Hansjoerg Pack, European Equity Fund portfolio manager, Deutsche Asset Management

Hansjoerg Pack has been named portfolio manager for Deutsche Asset Management’s (DWS) European Equity Fund, effective 1 July. He replaces Juan Barriobero, who will become deputy portfolio manager.

Equity trading at DWS is led by Michael Abellera, based in New York.

Previously known as ‘The German Fund’, the European Equity Fund was established in 1986 and holds US$72 million in total net assets, making is a relative minnow in DWS’s total US$1,152.7 billion in assets under management.

Pack has more than 35 years of industry experience and has been a portfolio manager and senior fund manager for equities at DWSsince 2000. In this role, he specialised in funds with significant German small and mid-cap equities.

Prior to this, he was a portfolio manager and team head at Deutsche Bank’s funds management group.

Australian multi-asset prime broker 26 Degrees Global Markets has adopted QuantHouse’s Cboe One Feed to facilitate US equity market access for non-US participants.

The Cboe One Feed provides real-time markets data from Cboe’s four US equity trading venues, which represent 21.2% of on-exchange trading, including data from the 4-7am early hours trading session, where Cboe has a 40.5% market share.

Rob Kirby, head of EMEA and APAC sales and business development at QuantHouse, commented: “[The integration] supports contract for differences retail flow and meeting growing investor appetite, particularly in Asia, to trade around the clock”

Various exchanges have been extending trading hours, and the US has been establishing plans to move to a 24-hour trading structure, in part due to increased international demand for access to the US market.

Anton Gorshkov, head of engineering, Genesis Computing

Anton Gorshkov has left Goldman Sachs after more than 24 years with the company.

Commenting on his departure via LinkedIn, Gorshkov said: “With time I matured, grew, evolved as did Goldman and it seems we’ve reached a point where our trajectories are on different planes.”

He will now serve as head of engineering at Genesis Computing, which developed purpose-built AI data agents for engineering, operations and analysis.

Explaining the business, he said: “We’re building intelligent data agents for enterprise systems that think, adapt, remember and assist, not just execute.”

Gorshkov joined Goldman Sachs in 2001 as a compliance technology analyst, later taking on senior roles including vice president of equities core trading, asset management core strategies, and quantitative investment strategies. Since February 2021, he has been a managing director for asset management strategic initiatives.

Ross Finlayson, head of markets and product strategy for ETFs and indexing, Amundi

Amundi has appointed Ross Finlayson as head of markets and product strategy for the ETF and indexing business. He is based in London.

According to Morningstar data Amundi sat in third place when it comes to European ETF market share in 2024, taking 12.4%. BlackRock’s iShares led the way with 42.2%.

Finlayson has spent 12 of his more than 15-year career at BlackRock, where he was most recently a managing director and head of iShares EMEA equity product strategy and markets coverage.

Prior to this, Finlayson was a trader at Avalon Capital markets and a pan-European equity trader at Nomura International. He began his career as an equity trader at Lehman Brothers in 2008.

Wenjie Zhang, country officer and banking head for China and president and executive director of Citibank China

Citi has named Wenjie Zhang as country officer and banking head for China and president and executive director of the Citibank China business, effective July 2025.

Based in Shanghai, he reports to Marc Luet, head of Japan, Asia North, Australia and banking.

Citi reported US$81.1 billion in revenues globally in 2024, US$19.8 billion of which came from the markets division. Within this, Japan, Asia North and Australia (JANA) contributed US$2.5 billion.

As a representative of Citi in the Mainland China region, Zhang is responsible for developing regulatory relationships and ensuring risk control.

Luet commented: “China is one of the largest markets for Citi globally. Wenjie’s depth and breadth of experience and on-ground expertise and knowledge will enhance our growth in this important market as we continue to support our clients’ cross-border banking needs.”

Zhang has 30 years of industry experience and rejoins Citi from Bank of America, where he has been China president and managing director of global corporate and investment banking since late 2020. Earlier in his career, he was co-head of global banking and an executive vice president at HSBC China, and held senior roles at JP Morgan, Citi and Credit Agricole.

Citi has been building out its emerging markets business this year, with Natalia Maksimova joining as an equity sales trader last month.

BNP Paribas has hired program-trading specialist Jack Tierney as in its program trading desk in London.

Tierney most recently consulted for Hobart Capital Markets and. Before that, he spent five years at Credit Suisse covering multi-product equity trading for institutional clients. Earlier in his 17-year career he held electronic trading positions at Goldman Sachs, Instinet and J.P. Morgan.

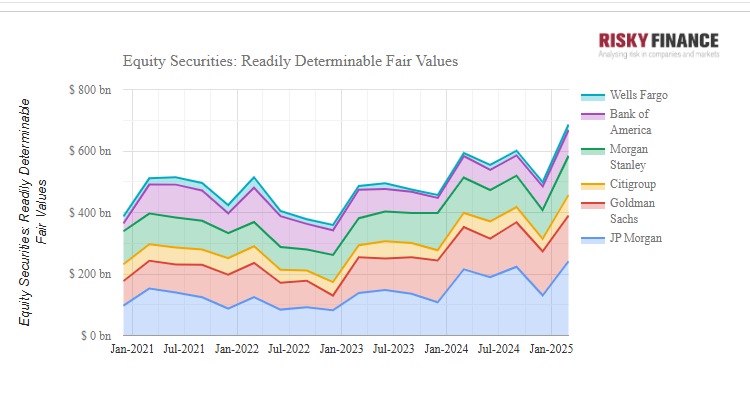

JP Morgan twice breached its VaR limit and lost US$203 million on two trading days, as the bank’s markets revenues, trading assets and derivative exposures reached record highs during the first quarter.

“Our folks did a fabulous job trading this quarter”, declared JP Morgan CEO Jamie Dimon on an 11 April earnings call, as the banking giant reported record markets revenues of $9.7 billion. But there were two trading days for which JP Morgan’s results were less than stellar.

According to Federal Reserve filings published in May, the banking giant twice exceeded its value-at-risk limit during the three months ending on 31 March, suffering losses of $116 million and $87 million on two trading days. The figures are disclosed because the Fed requires large banks to report their worst trading results as a percentage of regulatory VaR.

This is the second consecutive quarter for which JP Morgan has reported VaR breaches, with $231 million of losses on two days in the fourth quarter of 2024. Like the latest results, this pair of losses occurred amid a backdrop of strong overall trading results for the bank.

Regulatory VaR is measured at the 99th percentile, meaning that breaches of VaR limits are predicted to happen on one in 100 trading days on average. Multiple breaches can indicate unusual market conditions, as well as a problem with a bank’s risk model.

The trading volatility comes as the top six US banks reported record levels of trading assets and derivatives exposures in the first quarter. In particular, JP Morgan reported its largest ever holdings of cash equity securities at $241 billion, and largest ever equity swap notional exposures of $926 billion. These over-the-counter derivatives are increasingly used alongside cash equity positions and traditional short selling using prime brokerage.

Responding to Global Trading, a JP Morgan spokesman said, “As a reliable market-maker, we were well-prepared for those temporary – and manageable – losses while supporting clients during volatile markets. We fully recovered those losses, and our Markets business recorded a best-ever first quarter.”

Gary Paulin, chief investment officer, Northern Trust Asset Management (NTAM)

Northern Trust Asset Management (NTAM) has appointed two chief investment strategists. Gary Paulin takes on international responsibilities, while Joseph Tanious will head the North America region.

The pair report to incoming global co-chief investment officers Michael Hunstad and Chris Roth, who will lead the division from 1 June.

In their roles Paulin and Tanious will work with investment teams across asset classes to develop the firm’s economic and market views, and produce research and analysis on new instruments and market developments.

Roth commented: “Their expertise will be invaluable as we support our clients through changing market environments and evolving risk profiles.”

As of 31 March, NTAM held US$1.3 trillion in assets under management.

The appointments follow the continued expansion of NTAM’s quant investment strategies team, which saw 13 new hires in the Amsterdam office earlier this year.

Paulin has been with Northern Trust since 2016, leading integrated trading solutions in the capital markets business before becoming head of global strategic solutions in 2021 and head of international enterprise client solutions in 2024. Prior to this, he was a founding partner at boutique investment bank Aviate Global and part of the equity sales team at Merrill Lynch.

With more than 25 years of experience, Tanious joins NTAM after 11 years at Bessemer Trust. Most recently, he was a managing director and head of portfolio strategy at the firm. Earlier in his career, Tanious was an executive director and market strategist at JP Morgan Asset Management.

Natalia Maksimova, emerging markets equity sales trader, Citi

Natalia Maksimova has joined Citi as an emerging markets equity sales trader as the group continues to expand the division. She is based in London.

Citi’s total markets revenue in 2024 was US$19.8 billion. Equities made up US$5.1 billion of this, up 26% year-on-year.

With 25 years of experience, Maksimova was most recently an emerging markets equity sales trader and director at Credit Suisse, a role she held for more than 15 years. Prior to this, she had the same title at UBS.

Market makers are paying more than $4.9 bn a year for US equity and options order flow as retail participation cushions markets from tariff turmoil, according to regulatory filings compiled by S3.

As Douglas C. Cifu, chief executive officer, said it during Virtu’s latest earnings’ call on 23 April, “Market Making had its best quarter since the first quarter of 2021”.

So did related payment for order flows. A detailed aggregation of every broker’s Rule 606 filing indicates that market-making firms paid a combined US $1.19 billion for US retail flow in the first quarter, the largest three-month total since public reporting began. The sum was twelve per cent higher than the previous record set in the final quarter of 2024 and fifty-four per cent above the year-earlier quarter. Almost two-thirds of that cash went to option contracts, a tilt that has intensified each year since 2021, while the remainder was directed to equities.

Data source: S3

Notes for visualisation tool use: Readers can toggle between market makers who pay for flow and see aggregate payments per security type and order types, the mirroring visualisation is available to look at payment recipients.

Citadel Securities again dominated, laying out US $388 million in the quarter. That figure was 45% above the same period a year earlier and 4% above its spend in the closing quarter of 2024. IMC’s Dash venture followed with US $227 million, up 84% year on year; Wolverine Execution Services, Susquehanna and Virtu Americas rounded out the top five on US $109 million, US $101 million and US $75 million respectively. Together those five market makers accounted for 87% of total payments within our reporting universe. The skew towards derivatives was stark: IMC and Wolverine channelled one hundred per cent of their outlay to options, Susquehanna 75% and Citadel 71%, whereas Virtu paid solely for equities.

A source close to Citadel Securities told Global Trading that the firm’s leading position results from its large wholesale market presence and price improvement capability.

Across our entire sample, the distribution by order-type shows why limit instructions are so valuable to wholesalers. Pure market orders attracted US $212 million of payments, equivalent to an average 0.19 cent per share. Marketable-limit orders drew US $370 million at 0.67 cent per share, and fully passive, non-marketable limit orders commanded US $448 million at 1.70 cent per share. “Other” orders, not held and conditional instructions, made up the remaining US $155 million and were paid at roughly 0.38 cent per share. Citadel’s own pattern closely mirrored the industry’s ladder, whereas IMC’s equivalents converted to more than thirty-eight cent per share for marketable flow and just over 0.50 cents for passive orders.

On the receiving side, retail brokers logged commensurate gains. Robinhood’s two broker-dealer entities together booked US $560 million, 65% than in the first quarter of 2024 and 4% up quarter on quarter. Charles Schwab, now reporting on a fully integrated Ameritrade platform, received US $355 million, lifting its tally by twenty-four per cent year on year. Morgan Stanley’s E*Trade franchise, Fidelity and Webull collected US $93 million, US $72 million and US $57 million respectively; Webull’s total almost doubled against a year earlier.

Robinhood remains the most derivatives-heavy recipient: 80% of its payment receipts came from options and its weighted (weighted on a factored across market makers sample) average PFOF came to 0.65 cent per share, the highest in the top tier.

During the company’s quarterly call chief financial officer Jason Warnick told analysts, “We saw record options volume in the quarter, driven by strong customer engagement.”

The monthly rhythm of payments underlines how quickly retail participation has strengthened since the new administration arrived in office.

January’s aggregate reached US $410 million, February posted US $395 million and March US $380 million – each comfortably above the strongest month of 2024. From a comparative base in the first quarter of 2022, option-linked payments have trebled, whereas cash linked to equities has grown by less than half, reinforcing the view that retail trading is concentrating in short-dated, high-gamma contracts.

All listed market makers declined to comment. Fidelity and Robinhood confirmed our figures.

Methodology: All amounts are taken directly from S3 database which amongst other offerings compile 606 and 605 public disclosures.

Order-type averages are calculated by dividing each firm’s disclosure of dollars paid by its disclosure of equivalent shares or contracts for the same order category.

Rule 606 filings include rebates from exchanges in addition to payment for order flow from market makers. For example, for Interactive brokers 30% of their equities’ receipts in Q1 2025 came from the exchanges rebates and 100% of their options receipts (US$ 12.6million) came from exchange rebates.

")