LiquidMetrix analyses consolidated performance figures for equities and ETFs traded in Europe in the previous quarter.

LiquidMetrix’s unique benchmarking methodology provides accurate measurements of trends in market movements. We have seen many changes to market microstructure over the last year, and here we present statistics as a guide on the current trends as we come to grips with the pandemic.

The market trend over the year was a steady increase in the % LIS against the general increase in value traded to its peak in June 2019, then a slight decline to the end of the year. There was a slight, then dramatic decline in % LIS in the first Quarter of 2020 as the effects of the pandemic were felt on the markets, but dramatic increases in volumes traded during this period. In Q2 of 2020, volumes slightly reduced, and % LIS figures are slowly returning to those seen in Q4 2019.

One criterion to assess venue quality is the % of times the venue has a best price in the market. This is a measure of how competitive the lit markets are as it is based upon the major index constituents of each market, and includes both price ties and unique best price.

The trend continued from Q1 on lit markets in Q2 with the majority of venues and markets having reductions in the % best price. The only exceptions were Turquoise and Aquis on DAX, and Turquoise on FTSE. This further redution in % best price is likley due to increased competition between venues and their liquidity providers

The market liquidity picture shown below reflects some of the real effects of the pandemic with dramatic reductions in liquidity on all venues and markets apart from OMX-S where the different approach to lockdown by the Swedish government may be a factor. On all other markets the reduction in liquidity on primary venues was significant, with the reduction on DAX being the greatest in Q2 2020.

The tables below provide a method to assess performance of dark pools in Europe with the value traded, average trade value and measure the % of times there is a corresponding movement on the lit market.

Overall, there was a decrease in trade sizes and value traded across all dark markets in the period. Chi-X increased their ranking on FTSE and UBS increased ranging on both FTSE, DAX and OMX-S. Posit also increased rank on OMX-S.

For the periodic auction pools, values traded increased in the period. Rankings altered little, but Sigma increased rank on MIB, and Aquis and UBS increased on OMX-S.

As has been previously noted in 2019 we had seen an increase in trade sizes across the non-lit regulated markets, but we see some dramatic changes in volumes traded in SI.

The chart below shows the trend in daily value traded in dark pools, periodic auction venues and SI for major index constituents across Europe from Q4 2019 to Q2 2020.

We can see from the chart that the trend in dark value traded increased towards the end of Q4, but had the reductions expected towards the end of year. In Q1 dark volumes increased again, but periodic auction volumes remained flat. The effect of the pandemic appears to be in late Q1 and the beginning of Q2 volumes on all 3 types of venue decreased, but we can observe significant increases in SI volume from the beginning of June 2020.

ISS LiquidMetrix are pioneers in the measurement of European Fragmented markets, and provide research,TCA best execution and Surveillance for financial market participants and regulators – www.liquidmetrix.com

Gary Collier, CTO of Man Group Alpha Technology, and Hinesh Kalian, Director of Data Science, Man Group, discuss the state of data science on the buy side, spanning its evolution, current challenges, and the future outlook.

The podcast is moderated by Global Trading Editor Terry Flanagan.

In early July, I was fortunate to host a webinar on “Reg NMS II” for Eventus Systems featuring guest speaker Adam Inzirillo, Head of U.S. Equities at Cboe Global Markets. We had a lively discussion about equity market structure and the potential implications of this proposed regulatory update. We always look at regulations that potentially affect our clients’ trading activities and market risk requirements, and the conversation explored what firms should keep in mind as the proposal evolves.

Today’s Equity Markets: What’s Working and What’s Not

While the industry grappled with COVID-19, the markets remained resilient in the face of increased trading volume and volatility. Several regulatory safeguards demonstrated how markets and regulations have evolved:

Rules 201 and 204, focused on short selling and close-out requirements, respectively

Limit Up-Limit Down (LULD), implemented to limit volatility in National Market System (NMS) securities

Reg SCI, aimed at strengthening the technology infrastructure of the markets

Despite these safeguards, four circuit breakers triggered during March and April temporarily halted exchange trading. These events prompted the industry to question whether circuit breakers had to be revisited, especially when they trigger at the open.

Regulation National Market System (Reg NMS) and Transparency

Implemented by the SEC in 2007, Reg NMS encompassed initiatives designed to modernize the national market system for equity securities. At the time, market participants debated at length whether some components of Reg NMS were overly prescriptive and detrimental to competition and innovation.

As our discussion focused on transparency, we noted that the later enactment of both Reg ATS-N and the Rule 606 amendments – which increased the transparency of both alternative trading systems and handling of orders by broker-dealers, respectively – were examples of useful regulatory change.

Market Data Infrastructure Proposal Issues (aka “Reg NMS II”)

The SEC released proposed Reg NMS II in January seeking to create even more transparency. While Reg NMS II seeks to address the disparity in content and latency of market data provided by securities information processors (the “SIP”) and proprietary data products, this proposal has already earned vigorous commentary.

Adam and I focused on several elements of the proposal including:

Replacing the current “exclusive SIP” model with a decentralized model of “competing consolidators”

Elimination of a “unified” National Best Bid Offer (“NBBO”) necessary to accommodate multiple consolidators

Expanding the “Core Data” provided to the SIP, i.e., depth of book data

Adam identified a number of concerns and issues with the proposal that are likely to be raised by market participants including:

Undue burden on brokers with expansion of core data to five levels (i.e. routing protocols and data interpretation will be complex and expensive)

Inefficiency and complexity in distributing and ingesting a much-expanded set of data

Unnecessary regulatory burden created by a two-tiered market and an effective NBBO

Onerous procedures to stay compliant with Rule 611 and inter-market sweep orders (ISOs).

Suggestions and Predictions

Adam suggested the following ideas that would prove beneficial to all participants, with less complexity:

A distributed SIP model with equal access to all participants

Distribute relevant content without adding complexity

Eliminate the two-tiered markets proposal

Focus on innovation that benefits all market participants

Encourage targeted market structure enhancements for which there is general consensus – and do not harm what is already working well

While the SEC is right to address issues like transparency, market data and the modernization of markets, it remains to be seen how the Reg NMS II proposal will pan out. Based on early comments and discussion in the industry, we believe there’s a good chance Reg NMS II will be amended before final approval.

Cboe Global Markets is aiming to launch periodic auctions in the US, after success in Europe, as off-exchange trading volume has been increasing.

Adam Inzirillo, head of US equities at Cboe Global Markets, told Markets Media: “In the last couple of years, as off-exchange trading volumes have grown, periodic auctions give the public an on-exchange alternative for executing block trades and attracting natural interest.”

Cboe Global Markets plans to bring periodic auctions to U.S. equity markets, subject to regulatory approval. The first auction mechanism of its kind in the U.S. aims to enhance intraday liquidity in the public equity markets. Learn more: https://t.co/vKLjsrRHpT. #DefiningMarketspic.twitter.com/OD0vF7QOhZ

Periodic auctions last for very short periods of time during the trading day and are triggered by market participants, rather than the venue, helping them find liquidity quickly with low market impact, while prioritizing size and price.

Justin Schack, partner and managing director at Rosenblatt Securities, noted the increasing volumes of off-exchange trading:

43.16% of US equity volume traded off-exchange in July, a 4th straight record. The top 20 names by volume avg'd 49.18% off-board. 11 of these saw 50%+ OTC share and 7 of them traded 60%+ OTC. Clients can read more in our monthly volumes report here: https://t.co/YTDEEj9uY1

Greenwich Associates said in a report that the Covid-19 pandemic has triggered a major shift in US equity trading volumes away from exchanges.

The consultancy said off-exchange trading reported to the Trade Reporting Facility remained relatively stable last year between 35% and 40%.

“In all of 2019, there were 16 days with TRF volume above 40%,” added Greenwich. “In contrast, as of early June 2020, the reporting to the TRF had already exceeded 40% of market volume 58 times.”

Cboe launched periodic auctions in Europe in 2015 before the MiFID II regulations went live in 2018. MiFID II introduced double volume caps on equity trading in dark pools. However, trades in periodic auctions on lit venues were exempt from the volume caps.

Equities trading. Source: Cboe.

Inzirillo said Cboe is building on the success of periodic auctions in Europe but the US model will not be exactly the same.

“Some key differences include randomization of the auction message, no broker preference and displayed orders may become part of the auction,” he added.

In the European Union, exchange operators may own dark and lit books, but the current US regulatory regime precludes Cboe from owning and/or operating an ATS. Therefore Cboe intends to introduce periodic auctions on its Cboe BYX Equities Exchange.

Inzirillo said: “Periodic auctions also address some of the issues raised by the SEC regarding illiquid securities, which a high percentage occurs off exchange.”

The introduction of periodic auctions in the US requires approval from the US Securities and Exchange Commission.

Schack said in an email that Cboe’s regulatory filing for periodic auctions cites the SEC’s recent statement encouraging exchanges to propose innovative methods for improving outcomes in thinly traded securities.

“Some may prefer auctions to continuous trading for these less liquid shares, as a way to aggregate latent interest traders are reluctant to display,” Schack added. “Cboe’s European auction, though it has important differences from the US proposal, registers higher market share for smaller-cap issues than blue chips.”

Cboe said its European periodic auction accounted for more than 70% of all periodic auction activity, or approximately 2.4% of notional value traded on European equities exchanges.

Adam Inzirillo, Cboe

“In Europe, our periodic auction volume has been more than an average daily traded notional value of €1bn in the first half of this year, so we see an opportunity,” said Inzirillo.

Schack said the US market is so competitive that it is very difficult for any new venue or innovation on an existing venue to attract a lot of market share. For example, the biggest US dark pool, UBS ATS, is still less than 2% of total volume.

“Another complicating factor is that the recent surge in retail trading has hurt on-exchange market share considerably,” he added. “Considering all that, I’d be surprised to see exchange auctions get to the same level in the US that they’ve reached in Europe — at least not anytime soon.”

However, he noted that the US auction is different from the European version with integration with the rest of the Cboe BYX order book.

“That could help the US auctions — essentially new order types on an existing exchange, with the ability for other order-book interest to participate — build market share more easily than an entirely new venue might have,” said Schack.

Shane Swanson, senior analyst for Greenwich Associates market structure and technology, agreed that off-exchange volume could be rising due to the role of retail trading and their order flow bring directed to market makers such as Citadel Securities, Virtu and Two Sigma.

— Coalition Greenwich (a division of CRISIL) (@CoalitionGrnwch) July 21, 2020

“With proper systems, risk hedging and management, these firms appear to have been able to internalize more trades with the retail market, resulting in the increase in market share moving away from the exchanges,” said Swanson. “Moreover, as volatility skyrocketed, firms may have decided that dark trading was important to help prevent signaling to a market already in distress.”

Second quarter results

Edward Tilly, chairman, president and chief executive of Cboe Global Markets, said on the results call last week that the strategy over the last four years since the purchase of Bats Global Markets, the European exchange, in 2017 has been vindicated.

Edward Tilly, Cboe

“The Bats acquisition enabled us to strengthen our product set with new asset classes for Cboe, including U.S. and European equities and global foreign exchange, and to expand our market for multi-listed options,” added Tilly.

He continued that the exchange has methodically strengthened equities trading through the launch of new trading mechanisms and market enhancements and by cross-selling.

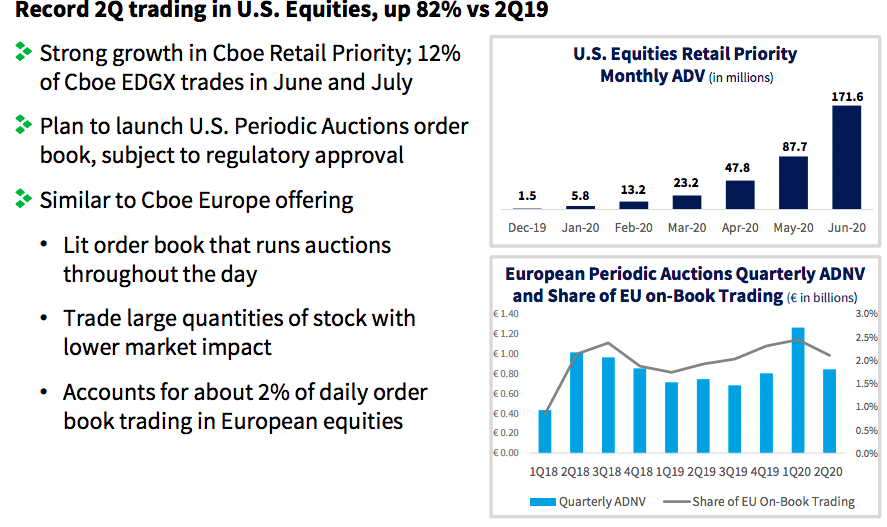

“We saw those efforts pay off in the second quarter when US equities trading at Cboe increased 82% over the previous year for an all-time quarterly average daily volume high of two billion shares traded,” said Tilly.

Volumes were also driven by the Retail Priority program, which was introduced to help improve execution quality and trading outcomes for individual investors and firms that facilitate their orders.

“Retail Priority orders have increased each month since their launch on Cboe EDGX in November 2019, and represented 12% of shares executed on Cboe EDGX in the last two months,” he added.

The exchange reported that Cboe US Equities had market share of 16.1% for the second quarter of this year, compared to 15.7% a year ago.

In contrast market share for Cboe European Equities fell 15.8% from 20.3% over the same timeframe which Cboe said was a result of market profile shifts and short sale bans, which impacted order flow.

Tilly cited the launch of US periodic auctions as another example of the exchange’s focus on equity product innovation. He said: “We believe the US market will also value executing trades in a venue designed to provide minimal market impact.”

On July 1 Cboe closed its acquisition of equities clearinghouse EuroCCP and announced its intention to expand equities derivatives trading in Europe by offering a market model similar to the US .

“We plan to launch that market with trading in equity futures and options based on six Cboe European stock indices in the first half of 2021, with plans to add more benchmarks later,” added Tilly.

In the second quarter Cboe also completed the acquisition of data provider Trade Alert and announced plans to acquire MATCHNow, the Canadian ATS, which completed this week.

Todd McDonald, co-founder of enterprise blockchain software firm R3, said the use of blockchain in capital markets is on the cusp of some really exciting developments.

Todd McDonald, R3

McDonald told Markets Media: “We need to ensure the technology is simple to use for institutional investors and that its why the collaboration with Nasdaq is important. They have experience running a regulated exchange and we are providing something additive to what is out there already.”

In April Nasdaq announced a long-term collaboration agreement with R3. The exchange’s Market Technology business will use Corda, R3’s enterprise blockchain software, to build full trade lifecycle solutions for digital assets marketplaces.

Johan Toll, head of digital assets, Market Technology at Nasdaq, said in a statement: “R3’s Corda platform will fit well into Nasdaq’s technology ecosystem and partnership strategy and allow us to harness the power of scalable design and a new level of interoperability.”

Nasdaq said the R3 collaboration will advance the exchange’s efforts in helping digital assets marketplaces strengthen transparency standards to align with their capital markets counterparts as they evolve their businesses.

Cathy Minter, chief revenue officer at R3, said in a statement: “Financial institutions are becoming increasingly aware of the huge potential for servicing the needs of digital assets. We can help them accommodate these assets with solutions that are designed for more secure, reliable and regulated environments.”

In June Nasdaq launched the Marketplace Services Platform which allows users to build new marketplaces across the trading lifecycle, from execution through to settlement, custody and payment, by using cloud-based plug and play components.

(Thread): Today, @NasdaqTech reveals the new Marketplace Services Platform, providing next-generation marketplace capabilities spanning the transaction lifecycle.

MarketPlace Services includes a Digital Assets Suite which is agnostic to the underlying digital ledger technology, is multi-cloud and will also be accessible for marketplaces in Microsoft’s Azure. Nasdaq is working with Digital Asset, R3 and Symbiont to deliver technology through the Marketplace Services Platform to meet the diverse needs and unique models of tokenized and digital assets marketplaces.

Magnus Haglind, Nasdaq

Magnus Haglind, senior vice president and head of product management, Market Technology at Nasdaq, told Markets Media in July: “We are working with firms such as R3 and the digital asset space has matured as vendors are moving into the next phase. We hope the number of partnerships will grow and create a broader ecosystem.”

McDonald also pointed to the Depository Trust & Clearing Corporation’s two projects to explore the benefits of digitalization in the public and private markets as being significant.

In May the DTCC unveiled two digital projects. Project Ion will explore accelerating settlement using distributed ledger technology and tokenized securities. Project Whitney is a prototype focused on exploring the potential for asset tokenization and digital infrastructure to support private market securities, from issuance through secondary markets.

Missed the #DTCCForum2020 last week? Watch recordings from our event, where DTCC executives and industry experts discuss the firm’s two projects—Ion and Whitney—to explore the road to T+0 settlement and asset tokenization: https://t.co/oQNRY22Z5lpic.twitter.com/oKcWojHrjK

McDonald continued that the two key metrics for measuring Corda’s progress are volume and value. He said: “The level of progress is ramping up and tokenization is an area of big growth.”

He said the need to work remotely as a result of the Covid-19 pandemic has accelerated progress.

“The pandemic has shone a light on digital transformation which is in name only and incumbents have accelerated plans,” added McDonald.

Darren Coote, chief executive at Cobalt, said the investment by Standard Chartered last month establishes the firm as a core utility in the foreign exchange market.

Cobalt provides infrastructure for the foreign exchange market based on shared ledger and high-performance technology. Standard Chartered joined the platform in February this year and also became an investor last month.

Standard Chartered Bank is the latest bank to announce it is to go live on Cobalt’s foreign exchange post-trade infrastructure.

Coote told Markets Media: “Standard Chartered’s investment further establishes Cobalt as a core utility in the FX market and is a great endorsement for other clients to join the network.”

He continued that half a dozen of the largest FX liquidity providers are on the platform and others will join this year. For example, Citi also joined the platform this year.

We are delighted to announce @Citi's support for Cobalt’s FX post-trade infrastructure for bilateral flow.

Gareth James, macro chief operating officer at Standard Chartered, said in a statement: “We see Cobalt as being a core part of our FX operating platform, enabling Standard Chartered to reduce risk and costs by automating manual processes across the bank and therefore improving services to our clients.”

Standard Chartered has a strong franchise in emerging markets.

Coote said: “Emerging markets are a focus as they are not covered by CLS and are quickly growing market share. Clients in this region benefit from Cobalt’s ability to make netting much more efficient.”

The majority of settlement in FX takes place through the CLS, the bank-owned infrastructure.

Cobalt was launched to reduce costs by approximately 80% through more efficient management of trades though their life cycle by developing a range of middle and back office processes that can plug into any distributed ledger technology. This allows the creation of a single shared record for every type of foreign exchange trade rather than each firm recording its own ledger on multiple systems.

Clients can choose how to integrate their own systems with Cobalt, which can then connect to CLS or another settlement system. Cobalt also allows banks to brand the technology to use for their own clients.

Darren Coote, Cobalt

“In the last six months we have upgraded the platform to a full microservices architecture,” added Coote. “The technology is more scalable and easier for clients to deploy, and they can also white label our services.”

Microservices breaks a problem into small components of functionality, while ensuring that the data they use is consistent in real-time. Firms can stop using monolithic architecture which is difficult and expensive to change without building a new version of the whole application.

Covid-19

Coote continued that the Cobalt team did an “exceptional” job in upgrading the system while continuing to seamlessly function remotely during the Covid-19 pandemic.

“Cobalt’s hosted platform has proven particularly resilient during the pandemic and ideal for clients to access and manage FX post-trade remotely,” added Coote.

In June the Global Foreign Exchange Committee discussed the operational challenges caused by the pandemic in a teleconference.

GFXC meets via teleconference to discuss FX market conditions and the impact of COVID-19 – https://t.co/11pR6YmBQi

— Global Foreign Exchange Committee (@GlobalFxc) June 23, 2020

“Overall, participants felt that the transition had been smooth, with no major operational issues arising,” said the committee in a report.

Participants said they were actively planning to ensure they can operate some elements of the remote working arrangements on a longer-term basis.

“Considerations noted included the need to continue making progress on workplace flexibility, the importance of ensuring that new staff, and particularly new junior staff, are effectively trained outside of the traditional trading floor environment, and the need to ensure continued focus on strategic planning and medium-term change initiatives,” added the report.

The GFXC also discussed the Bank for International Settlements’ 2019 Triennial Survey of FX markets which suggests that the proportion of trades being settled without payment-versus-payment protection may have increased.

“The amounts involved, and hence the risks posed, are potentially very significant, and require continued engagement from front and back offices in the FX market,” added the committee. “In light of that, the GFXC and local FX committees will consider ways to assist with gaining a better understanding of trends in settlement activity and with supporting the management and reduction of FX settlement risk, including reviewing the guidance in the Code.”

This article first appeared as FLASH FRIDAY on Traders Magazine.

FLASH FRIDAY is a weekly content series looking at the past, present and future of capital markets trading and technology. FLASH FRIDAY is sponsored by Instinet.

In business there’s a certain dynamic that plays out between profit-seeking industry participants and regulators: industry participants try to innovate and stay a step ahead; regulators try to catch up.

That ongoing dynamic is certainly the case in the capital markets business, where trading and investing firms seek to gain efficiencies and an edge on rivals, and the U.S. Securities and Exchange Commission, the Financial Industry Regulatory Authority and other regulators work to stay on top of the latest trends and determine what if any new rules or rule changes are needed.

Traders Magazine caught up with one financial regulatory expert, who started his career the same year man landed on the moon.

From a 1998 Traders Magazine article:

—–

John E. Pinto, a 29-year veteran and senior official of market regulation at the National Association of Securities Dealers, has left the organization to run the Washington branch of Dover International, an Atlanta-based consulting firm.

Pinto had most recently served as an executive vice president of member regulation at NASD Regulation, the NASD subsidiary headed by Mary Schapiro. NASD Regulation was created two years ago in the wake of two governmental investigations of Nasdaq.

“I saw a significant change happening in the organization,” Pinto said. “Mary Schapiro was bringing in her own people. I felt it was time for me to move on.”

Pinto joins Dover as an executive vice president and president of Dover’s Financial Services Exchange, a subsidiary that specializes in mergers and acquisitions. He is currently the sole employee at Dover’s Washington outpost. His compensation includes an equity stake in the firm.

Pinto had a high-profile NASD career. Pinto joined the organization in New York in 1969, gaining prominence as an examiner. He moved to the NASD’s main office in Washington in 1975, serving separately as a director of enforcement, vice president of surveillance and senior vice president of compliance.

In 1989, Pinto was named executive vice president of regulation at the NASD, responsible for all enforcement, examination and surveillance at the organization. As executive vice president, Pinto supervised all regional attorneys and oversaw all advertising, compliance, corporate financing, enforcement and market-surveillance departments of the 14 NASD district offices. He was named executive vice president at NASD Regulation in 1996.

—–

Fast forward to 2020, and Pinto is Managing Director at Renaissance Regulatory Services, a Washington, D.C.-based firm that provides compliance and operational consulting and support services to broker-dealers and investment advisers. According to its website, the firm is “founded on the premise that the financial services industry is constantly changing”, and Pinto has seen a lot of change.

John Pinto, Renaissance Regulatory Services

“If you look at the way the Nasdaq market operates, it’s all geared toward electronic trading and the type of activity that doesn’t involve the intervention of a human being,” Pinto told Traders Magazine on Aug. 5.

“From the regulatory side, monitoring of the market has changed with the technology,” Pinto continued. “Back in the day you’d have some information, but basically you’d be going out into the field, sitting at the firm and reviewing things at the firm. Today, a lot of it is done by mining the data that a firm submits before an exam. It’s dealt with remotely before an examiner has to go on site.”

The SEC’s Regulation Best Interest is among the rulesets that Renaissance clients are most interested in currently, in terms of the impact on their business. Reg BI lays out a new standard of conduct for brokers, as well as an interpretation of the fiduciary duty that applies to registered investment advisors.

Pinto said the SEC and Finra are on balance effective regulatory organizations, considering their resource constraints. Finra reported 3,517 dues-paying member firms in 2019, down from 5,106 in 2005; Pinto recalls there were about 6,600 Finra member firms at one point.

“Regulators are always working hard to try to keep up with changes made in the industry,” he said. “They are making much better use of technology, which makes their manpower more effective.”

“People are in the business to make money, so they’re going to be innovative in finding better ways to do things, and the regulators have to try to keep up,” Pinto concluded. “I think they’re doing a pretty good job, but they have their challenges.”

It may seem like Covid-19 has been with us for years, but it has only been months and the buyside is already priming for the next global market event such as the need to stress-test the resilience of a firm’s operating model beyond traditional scenarios, according to a new report from Simcorp, a provider of investment management solutions and consultancy Clear Path Analysis. This means not only looking at remote working capabilities but also digitalisation and cloud infrastructure as well as asset diversification

The report – The new operating environment: People, Processes, and Technology – is based on perspectives from senior European executives across asset management, pensions, insurance and banking.

Dean Chisholm, Invesco Asset Management

“This pandemic has shown everyone the need for a strong work from home technology environment, which probably had varied across the industry prior to it happening,” said Dean Chisholm, Regional Head of Operations, Asia Pacific at Invesco Asset Management. “This does have the implication of whether we need physical BCP (busines continuity plans) centres anymore, which has always been the traditional response. But now people are wondering just how useful they really are.”

He added that the pandemic reinforced the focus on clients and their requirements. “We realised that some things we had been doing weren’t really that important, so we asked why we were continuing to do them,” he said. “This type of questioning will continue quite heavily in the future, because we need to prioritise the client and what they want.”

The report also underscored the importance for buyside firms to review risk management models, to include new and emerging investment factors, such as rate of infections. In addition, they should should ensure that they have access to high quality, timely and granular, multi-asset data to navigate markets.

Molly Shannon, Wellington Management

As Molly Shannon, Member of the Executive Committee and Product Innovation Committee at Wellington Management (North America) pointed out, “Data scientists tell us that 95% of the world’s data has been created in the past five years. And so, we have essentially begun to restructure our workforce to harness all that data and help inform our investment decisions. Increased trade volumes and lack of liquidity in a market crisis mean that, without technology and the right tools, there is a heightened risk that errors will be made, and client objectives will not be met.”.

The report also noted buyside firms should be flexible in the way they deliver transparent and frequent client and regulatory reporting and to be holistic in the way they treat environmental, social and governance funds which have grown in popularity since the pandemic. Instead of having standalone strategies, ESG products and portfolios should be combined into a core data set.

Marc Schröter, Head of Global Product Management, SimCorp

In general, “the themes that emerged from the report point to the need for a simplified operating model, designed with the agility required to respond to any crisis,” said Marc Schröter, Head of Global Product Management at SimCorp.

He added, “Best of breed solutions that proliferate data silos, simply cannot support the speed and agility required for rapid asset diversification, liquidity management, timely exposure calculations, and other key investment functions across multiple asset classes. Additionally, digitalisation has to be high on the resilience agenda, not just for front-to-back processing, but also very importantly for proactive client communications.”

Andrew Edwards, CEO of Saxo Capital Markets explains why the industry needs to digitise and automate.

Andrew Edwards joined Saxo Bank in December 2017, and has since then served as the CEO of Saxo Bank’s UK entity. Andrew has overall responsibility for running an efficient, compliant, and prudent business, by constantly improving productivity, strengthening the Saxo brand as well as enhancing the quality of the firm’s employees within the UK organisation. Prior he spent 14 years at ETX Capital, the last position as CEO. He started his career at City Index as head of the US equity desk.

What do you think will be the long-term impact of Covid for the industry?

We are a digital trading and investment platform and there is no question that Covid-19 has created a significant amount of volatility and volume. This tested the scalability of the platform because although we built it to cope with increases in volume, it is one thing to test its resilience in artificial circumstances and another when it is real time. However, we were not significantly challenged and were able to continue support our clients. We also saw the time as a real opportunity to optimise the platform.

What lessons will be learnt?

In terms of lessons learnt, we did not have to change anything because we were already a global digital and automated platform so had the scale needed to handle the greater volumes and volatility. We also had data centres because of the provision of low latency we provide so were able to provide prices to customers whether it be in the US, Asia, UK or Copenhagen. We were also able to move to a remote operating model because our team in London, for example, was already used to talking to people via video tools in different locations. We have seen, in fact, an increase in productivity although there were some people who took longer to get used to the new norm but that was more due to the social aspects of working in an office.

What strategies did Saxo implement to keep the organisation working and to meet customer’s needs?

As a CEO of a subsidiary, there has not been any difference. Our job is to continually think about what can go wrong, to look at the risks, make sure the tech can hold up and build a good framework. We have regular internal audits that are highly valuable and will challenge us. A good governance structure can be timely and costly when you are building a business, but you realise its importance and how it helps you survive with these types of events.

I have read that you believe risk management should be a stronger focus for the industry. What do you think people should do going forward?

Risk management is more important than ever and it has always been a big part of our strategy. As a bank we have capital requirements to meet but I think companies outside the regulatory space also need to think more about balance sheet management because there will be further spikes over the long term due to the Covid-19 situation. We continually assess our cash reserves and I think this should be the case across the industry.

In general, the bank is often described more as a fintech player than a bank. What has been the strategy behind that?

The strategy that our founder, Kim Fournais, implemented over 10 years ago was to transform Saxo into a digital and automated company. I think he was quite visionary in that he saw how margin pressure and competition was changing the industry. He also realised that human behaviour was changing, and that people wanted to take greater control of their investment decisions and interact online as they were doing with every other aspect of their life. They expected to have a bank account and be able to transact instantaneously as well as having a lot of information at their fingertips across all asset classes.

We built a global digital investment platform that works for professional, retail and institutional clients and enables them to scale their business. However, we are also a bank and have built safeguards as well as a governance structure that meet the requisite capital and regulatory requirements.

I also see Saxo recently signed a deal with five Danish banks to white label. Are partnerships important?

We recently signed a white label partnership agreement with Sparekassen Vendsyssel, Sparekassen Thy, Middelfart Sparekasse, Frøs Sparekasse and Jutlander Bank to access our trading and investment solutions. Traditionally, banks have wanted to build and control their own value chain but the mindset is changing because of cost pressure and the time it takes for products to come to market. We have the full range of partnerships with robo-advisers to asset managers and brokers and all the way through to the traditional banks.

How is and will AI and machine learning change the industry and your organisation?

There are many firms that talk about it and invest capital but do not see the outputs. However, because of the nature of our business, AI has always been at the top of our agenda and we have quite a big initiative. Some of it is used to build new applications but more importantly, AI and data is being used to better understand customer behaviour and the tools and services they want. You need to attract new clients and retain existing ones but to do that you have to be able to improve their journey and experience.

Looking ahead, what objectives and opportunities are you pursuing and what do you see as challenges for the bank and industry?

The after-effects of Covid-19 will be challenging for firms who do not have scale, automation, digitalisation or the right governance structures in place. They will struggle to survive if they rely on manual processes. For us, we see an opportunity to grow organically by offering great services at a sensible price for new and existing customers. We will also be pursuing similar partnerships to the ones we struck with the five Danish banks.

As for acquisitions, we are currently integrating the Dutch stock brokerage company BinckBank which we bought last year. However, once that is finished, we will as ever be looking at other opportunities.

Covid-19 has triggered a “dramatic” shift in US Treasuries, the world’s largest bond market towards electronic execution from traditional voice trading, according to a report by JPMorgan Chase.

The figures from the Wall Street bank, one of the biggest Treasury dealers, reveal the corona virus accelerated a trend that was gradually occurring in the US government bond market. This is because many of the bank’s clients — who suddenly were forced to work from home in extremely volatile conditions — preferred to transact based on prices quoted on a screen rather than picking up the phone to negotiate with a human trader.

Over the past two years, roughly 50% of trading in the US Treasury market has been conducted electronically. However, the figure jumped to 70% in April, rising to 77% in June as traders became more comfortable with trading these products on screen.

Although the US Treasury market, which is the world’s most liquid bond market, has led the way in electronic trading, it still lags other asset classes such as equities and FX. For example, in the $6.6 trn a day currency market, estimates show that 90% of spot trading is executed digitally.

Anecdotal evidence shows that European fixed income volumes also went down electronic pipes, but it is further behind than the US despite the boost from MiFID II. Figures from a recent Greenwich Associates study – Uncharted Territory in European Fixed Income – show that electronic trading accounts for roughly 45% of the market.

Market participants cited the main benefits of electronic trading – greater liquidity and transparency – were particularly important at the height of the volatility spikes in the first quarter. Traders were able to quickly gauge market depth on their screens, freeing time for more complex trades plus the costs for investors were lower. Estimates were that trades were about 10%-30% cheaper than conventional voice trades.

However, this was not the case for all segments of the European market, and in some cases, such as investment-grade corporate bonds, the volatility and illiquidity sent traders back to their phones, according to a new study from the International Capital Markets Association (ICMA) assessing the impact of Covid on trading.

It said this was due to the difficulty dealers and liquidity providers had in offering prices across electronic platforms. Some banks closed their algo trading completely at the time, while others opted to continue auto-quoting prices.

As a result, while digitalisaton may be the future, industry experts believe that for the foreseeable time, both electronic and traditional trading models based on dealer-client relationships will continue to co-exist.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.

Shannon_Wellington")