Michael Horan, EMEA GIDS head of trading, SS&C Technologies

The increasingly crowded market for outsourced trading services has gained a new entrant as SS&C Technologies appointed trading veteran Michael Horan as head of its EMEA outsourced trading business.

The global investor and distribution solutions (GIDS) business provides operational insights and real-time transparent oversight to investors, advisors and asset managers, with global transfer agency and investor servicing available through a single platform. It was established in 2020.

Based in London, Horan will lead the outsourced trading division.

Horan has 30 years of industry experience, most recently as head of electronic equity trading at BNY. He held the role for more than a decade, leaving earlier this year amid department restructuring.

Prior to this, he was head of outsourced trading at Pershing EMEA. Earlier in his career, Horan was head of the European broker desk at Instinet and a UK equities inter-dealer broker at Tullett Prebon.

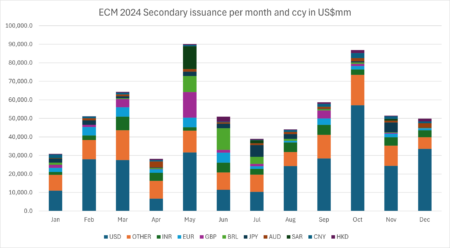

2024 was a boom year for equity capital raising, with $640bn of secondary offerings worldwide, according to Bloomberg data.

Secondary offerings were up 26% in 2024 over 2023 according to LSEG data, correlating with an overall strong market for stocks and the need for issuers to raise further equity.

Top US issuers included Boeing, which raised $18 billion in a rights issue in October, and Micro Strategy, which issued $15 billion in equity the same month “to buy more bitcoin”, according to a filing by the company. Saudi Arabia’s Aramco raised $11.2 billion in a secondary offering in May. Two Brazilian companies, Viver Incorporadora e Construtora and Cia de Saneamento Basico do Estado de Sao Paulo, raised a total of $19.4 billion during the year, according to Bloomberg.

ECM 2024 Secondary issuance per month and ccy in US$m, Source: Bloomberg

NASDAQ and NYSE accounted for 46% of secondary issuance volume of US$288.2 billion. The London Stock Exchange saw a high value of secondary issuance compared to its small IPO volumes, led by National Grid’s secondary offerings valued at around US$10 billion and a series of deals by Haleon totalling $8.4 billion. Similarly to its strong showing in the primary space, Indian secondary offerings were 7% of the total or $US 47.9 billion.

League tables were stable with the top 5 lead managers (Goldman Sachs & Co, JP Morgan, Morgan Stanley, BofA Securities Inc, Citi) keeping their rankings and helping issue US$197.2 billion worth of stocks, amid small movements lower down in the table with Indian banks gaining while European investment banks and Chinese banks lost some ground.

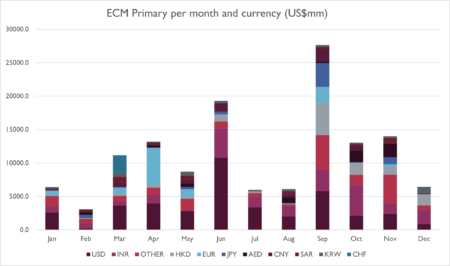

Dollar and Indian rupee-denominated initial public offerings in 2024 accounting for 56 per cent of primary issuance, underscoring the growing importance of India’s capital markets alongside traditional US venues.

The IPO landscape reflects broader shifts in global capital markets, with European financial centres increasingly sharing the spotlight with emerging market venues, particularly India and the Middle East this year.

Nasdaq was the year’s leading venue across its various platforms, in front of India’s National Stock Exchange, with the New York Stock Exchange and Hong Kong Exchange following behind. European exchanges saw notably subdued activity, compared with a surge of issuance on Middle Eastern bourses in Dubai, Abu Dhabi, and Saudi Arabia which collectively raised $12bn — surpassing the total euro-denominated issuance across all European exchanges, according to data compiled by Bloomberg.

Carmaker Hyundai Motor India’s $3.3bn capital raise which completed in October was the largest deal of the year in India, where total issuance of $22.7bn mostly consisted of smaller companies. In Europe, SIX Group accounted for $5.5bn of issuance with two deals, Galderma in Switzerland and Puig Brands in Spain. Home Furnishings group Midea raised $4.6bn in Hong Kong, part of $11.5bn of total issuance in the territory.

The market showed seasonal strength during the September to November period, though no single industry dominated issuance. Diversified holdings and REITs emerged as the most active sectors, albeit representing only a modest portion of total activity.

ECM IPOs by month Source: Bloomberg

In league tables compiled by LSEG, Morgan Stanley climbed from the 15th position in 2023 to claim the top spot among underwriters last year, bolstered by its lead roles in the high-profile Reddit and Astera Labs offerings which amounted to US$748 million and US$774 million respectively. JPMorgan Chase and Goldman Sachs both improved their standings, securing second and third positions respectively in the league tables. A notable entrant epitomising the good issuance year in India was Kotak Mahindra Bank Ltd in tenth place, while Chinese banks suffered from the poor performance of their home market last year – China Securities moved from second place in 2023 to twenty-fifth.

Rising market capitalisation prevented reduced transaction volumes from denting most European exchanges’ equity turnovers in 2024, according to end of year results.

Euronext continued its reign of dominance in European equities in 2024, reporting €2.7 trillion in transaction values over the year. At the other end of the scale, Deutsche Börse and LSE were almost tied with €1.05 trillion and €1.06 trillion reported respectively.

End-of-year 2024 results show LSE pushing ahead of Deutsche Börse in terms of equity turnover, reversing their 2023 standings. This shift occurred in the second half of the year, with Global Trading’s European Exchanges Handbook showing the 2023 rankings in place at mid-year.

Although it reported the greatest transaction value of European exchanges, Euronext’s results were up just 4% YoY, to €2.7 trillion. Similarly modest increases were seen between December 2023 and 2024, up 9% to €204.9 billion. As noted across the board, values dropped from the previous month – here by 14%.

Rising market capitalisation over the year superseded a decline in transactions, which dropped by 4% YoY in 2024 to 603.7 million at Euronext.

SIX Group (SIX Swiss Exchange and BME) was the only exception, noting a slight (1%) dip in order book turnover over the year to €1.1 trillion in whole-year results. Although there was a small bump in December results compared to 2023 (up 3% to €86.5 billion), there was a more drastic 17% decline on November’s turnover of €101.9 billion.

Transaction volumes were up 2.5% over the year to 44.6 million but dropped by 15.2% between November and December to 3.3 million. For the most part, it was the opposite story at European exchanges – with transaction volumes falling but turnover rising.

At Deutsche Börse, turnover rose by 2% YoY to €1.06 trillion on a year-to-date basis but declined somewhat compared to both December 2023 (€79.2 billion) and November 2024 (€91.3 billion).

Units traded were down 12% to 36 million (results adjusted for comparability) for the full year, and down 44% from December 2023 to 4.23 million in December 2024. This also marked a 44% rise on November’s figures.

LSE recorded a more drastic 12% YoY rise to €1.06 trillion in total volume traded for EOY 2024, and a 9% increase in December volumes YoY to €75.8 billion. From November, this figure dropped by almost a quarter (23%).

A marked decline in international equity trading (down 23% YoY) in 2024 was somewhat offset by a 7% increase in UK equity trades at the exchange. This was more pronounced between December 2023 and 2024 trading volumes, which were up just 1% and down 29% for UK and international equity respectively.

Global Trading examines six of the most influential trading and market microstructure papers published online in 2024.

Competition and Learning in Dealer Markets

Rama Cont.

A world in which AI-powered robots dominate trading may seem dystopian to some, but in their paper Hanna Assayag, Alexander Barzykin, Rama Cont, and Wei Xiong embrace this future. They analyse dealer behaviour in a hypothetical market consisting of autonomous market making agents with the ability to learn from experience. In a tour-de-force of theoretical exposition, the paper combines Nash equilibria (where players in a game can only win from others’ mistakes), mean-field theory (the physics of magnets), and reinforcement learning, the AI technique used by Google DeepMind to defeat the world’s best Go players. Their findings reveal that diversity among dealers helps prevent systematic over-bidding and under-offering (supra-competitive quoting strategies), suggesting that heterogeneity in dealer strategies contributes to more efficient market pricing for the market makers themselves.

Lit markets are often criticised for providing the illusion of liquidity, because fear of information leakage means most available liquidity remains concealed from view. Robert Bartlett and Maureen O’Hara seek to quantify this effect in U.S. equity markets, with a comprehensive multi-venue database of $467 billion of trades in which 40% of activity is hidden. Their research demonstrates how a simple machine learning model can assist broker-dealers in identifying hidden liquidity pools, and with better recall than conventional statistical models. With the help of a vendor dataset, they provide evidence of the bigger prevalence of hidden liquidity in high priced stocks (over $US100) as opposed to lower priced stocks (sub US$ 5)

There is a natural dichotomy in trading between liquidity-taking market orders and liquidity-providing limit orders. Executing entirely via limit orders is known as passive trading, and here Youssef Ouazzani Chahdi, Mathieu Rosenbaum, and Grégoire Szymanski introduce innovative models for understanding the market impact of such strategies. Previous work focused on the impact of metaorders when they are executed as market orders. Using a model known as the Hawkes propagator, here the authors provide theoretical predictions of the impact of meta orders executed passively – that is executed through providing liquidity on the bid or offer side of the market.

Efficient market theory states that securities prices reflect fundamental information but this view is under increasing attack from the market microstructure community. The latest assault comes from Philippe van der Beck, Jean-Philippe Bouchaud, and Dario Villamaina who argue that investors are unable to disentangle fundamentals from fund flows that inflate returns. Through anonymised thematic ETF flow data, they statistically examine the self inflated return and price impact of said ETF, as well as model price reversal events. They identify daily wealth reallocations of approximately 500 million dollars from ETF alone and propose a new regulatory metric called “fund illiquidity” to measure bubble risk.

Beyond the Bid–Ask: Strategic Insights into Spread Prediction and the Global Mid-Price Phenomenon

Svetlozar Rachev.

A hot topic in microstructure analysis is how the depth of limit order books (LOBs) affects quantitative finance questions such as option pricing and risk measurement. Yifan He, Abootaleb Shirvani, Barret Shao, Svetlozar Rachev, and Frank Fabozzi propose new LOB-based mid-price and spread metrics, incorporating the deeper liquidity in the total order book. Their findings, analysing these metrics for the stocks of Apple, Amazon, and Google, reveal heavy-tailed return distributions and innovative approaches to hedging liquidity risks with option pricing models. These insights refine trading strategies and risk management frameworks to take into account all available information within lit orderbooks.

Neil Chriss was a junior equity trader at Morgan Stanley in 1998 when he co-wrote the seminal paper ‘Optimal Liquidation’ which first explored the trade-off between market impact and volatility in execution strategies. After a distinguished career as an entrepreneur and hedge fund manager, Chriss has released a series of new papers. This one examines Nash equilibria (the best choice for each individual trader considering all information available) in multi-trader competition, providing closed-form solutions for equilibrium strategies and implementation costs. He highlights the benefits and drawbacks of different centralised trading strategies, optimised order flows, and the persistence of aggregate costs despite increased competition. These insights offer strategies for reducing trading costs in competitive markets. He demonstrates that naïve centralisation can result in increased cost through front running by other traders and an optimum centralised trading strategy can be found through splitting orders.

MetLife Investment Management (MIM) has agreed to acquire the small-cap equity team of financial services firm Mesirow, expanding its leveraged finance platform.

The transaction also includes Mesirow’s high yield, bank loan and strategic fixed income teams, with a total of US$6 billion in assets under management being transferred to MIM. As of September 2024, MIM held US$609.3 billion in assets under management.

Jude Driscoll, MIM president, commented: “As fundamental, bottom-up investors, these investment teams are excellent strategic fits and bring seasoned talent to MIM. By leveraging the power of the MIM platform, we believe we can accelerate growth in these strategies through investment performance and the breadth of our distribution capabilities.”

Natalie Brown, Mesirow CEO, added: “[We] will continue to focus on growing our alternatives capabilities and core wealth management, fiduciary solutions, and capital markets/investment banking offerings.”

In December, MIM acquired global asset manager PineBridge Investments in a total US$1.2 billion deal as part of MetLife’s ‘New Frontier’ expansion strategy. The initiative aims to deliver double-digit adjusted earnings per share, a 15-17% adjusted return on equity, a 100-basis-point reduction in direct expense ratio target and free cash flow of US$25 billion.

A Cboe Europe representative told Global Trading: “We have worked closely with Aquis to explore, via the SimpliCT joint venture, participation in the public tender process to operate the EU equities consolidated tape. However, after careful consideration we have together decided against proceeding any further.

“We remain strong advocates for the tape and, its potential to strengthen the EU market ecosystem, by helping to drive a more competitive, integrated and attractive EU market and offering choice and flexibility to market data consumers. We remain committed to supporting regulators and the industry to help deliver a tape that meets users’ needs.”

In November, SIX Group announced that it was acquiring Aquis, which led to concerns of a conflict of interest; SIX is a member of bank-led consortium EuroCTP. The group stated that it would withdraw from consortium EuroCTP if the exchange continued its bid for the tape.

Following ESMA’s publication of final regulatory technical standards (RTSs) for CTPs in December, the group’s CEO Eglantine Desautel shared a positive outlook with Global Trading. “When you build a platform, the devil is in the detail. But at this stage, we don’t see any major roadblocks that will require us to break things that we have been working on developing.”

Stewart Liduci, European head of investment banking, William Blair

Boutique investment banking, investment management and private wealth management firm William Blair has promoted Stewart Licudi to European head of investment banking.

As of September 2024, the company held US$74 billion in assets under management

In the London-based role, Licudi is responsible for the company’s European advisory activity.

He has close to three decades of industry experience, the past 18 years of which have been spent with William Blair. Most recently, he was head of investment banking for London.

Prior to this, Licudi was an investment director and a senior investment manager at private equity firms LDC and 3i Group, respectively.

AFME has named April Day as head of capital markets.

Based in London, she replaces Rick Watson, who announced his retirement in July 2024.

Day has more than 25 years of industry experience, and has been with AFME since 2012. She joined the firm as managing director of equities trading, later becoming head of the capital market’s equities division.

Prior to this, Day was director of equity sales at Panmure Gordon & Co and Dresdner Kleinwort.

Adam Farkas, CEO, commented: “April’s leadership and vision will undoubtedly strengthen our efforts to advance Europe’s capital markets and support our members in navigating the challenges and opportunities ahead.”

The Federal Reserve’s chief banking regulator Michael Barr has announced his resignation as vice-chair for supervision, creating fresh speculation over US financial regulation as Donald Trump prepares to return to the White House.

Barr, who will step down on February 28 while retaining his position on the Fed’s Board of Governors, cited concerns that potential conflicts could impede the central bank’s regulatory mission. His early departure comes amid an ambitious drive to strengthen capital requirements for the largest US banks.

Since his appointment in 2022, Barr has championed stricter banking rules, most notably through the contentious Basel III endgame proposal, which would require major US lenders to maintain larger capital buffers against potential losses. While he had recently signalled openness to scaling back these requirements following industry pushback, his departure might altogether end prospects for even a moderated version of the reforms.

Large US banks faced capital requirements increases under Basel III Endgame reforms, with systemically important banks (assets over US$100 billion) originally requiring 21% more capital. The trading book review could have raised risk assets’ weights in their balance sheet by 75%, potentially squeezing market liquidity and raising client costs.

“If there was any doubt, the 2023 Basel III Endgame proposal is dead,” said Brian Gardner, chief Washington policy strategist at Stifel. He characterised Barr’s exit as “positive for banks,” suggesting the move could free up capital for stock buybacks, dividends and lending activity.

The banking industry had criticised the Basel III proposals as overly stringent and lacking real-world modelling to assess their impact. The timing of Barr’s exit, more than a year before his term was due to expire, effectively puts major regulatory initiatives on hold. The Fed has indicated it will pause significant rulemaking until a new vice-chair for supervision is confirmed.

The resignation marks another potential shift in the regulatory landscape as the US prepares for its second Trump administration, with implications for both traditional banking and emerging financial technologies.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] Please review our updated Terms & Conditions and Privacy Policy carefully. By continuing to use our services after Aug 25, 2025, you agree to these