This is the fourth installment of a content series sponsored by CODA Markets

When I left the world of high-speed market-making back in 2014, friends were flummoxed. Auctions? Really? Nice for openings, nice for closings, but all-day long? What are you thinking?

Don Ross, PDQ EnterprisesTo be sure, I still have great regard for speed. As a trader, it served me well for ten years. But I could also see that the economics of speed were changing, rapidly, for the worse. The cost of shaving another microsecond was growing, year on year. It became clear there was more money to be made leveraging technology to fix market structure than there was trying to stay on top of a flawed one. Thus my conversion to on–demand auctions.

Auctions are not new, obviously. The New York Stock Exchange ran them from 1812 to 1870, only conceding the future to continuous trading when the existing floor technology could no longer keep pace with the growth in public listings and trading demand. Today, of course, we can do auctions electronically. More than a third of NYSE volume in NYSE-listed shares is done in their opening and closing auctions.

But why stop there? Why not do them all day long—on-demand, whenever traders want them? Well, here are the reasons I still hear:

You can’t trade more than 150 shares of anything without tipping your hand. This is true—in a continuous market with bilateral transactions. But in an auction, you can trade tens of thousands of shares without moving the market. Why? Because you don’t have to identify yourself or how many shares you want to trade—or even whether you want to buy or sell.

In a CODA auction, all you have to tell the world is that you (anonymously) want to trade a given stock. Then you sit back—between 5 milliseconds and 30 seconds, depending on your preference—and watch the counterparties come to you. If you don’t trade, no one’s the wiser. If you do trade, whether against one counterparty or ten, 500 shares or 50,000, the multilateral transaction that prints tells the world nothing about where the market is headed. Did a buyer initiate? A seller? No one knows—so future prices don’t budge.

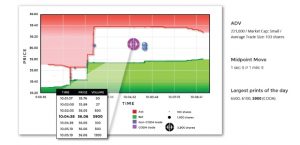

Consider this trade in Pfizer stock, in which a $3M+ transaction had just printed one tick outside of a thin NBBO. CODA’s multilateral auction facility allowed a liquidity seeker to offer down an extra penny on the $40 stock, and to capture 50 times the lit bid size—all with virtually no impact.

Pfizer, Inc. “PFE” – October 23, 2018

Ok, but liquidity is good enough in the continuous markets. Good enough? If you can trade 50,000 shares in one go, simultaneously against multiple counterparties, without revealing who you are or whether you are buying or selling, the market impact should still be less than trading 150 shares bilaterally, sequentially, 333 times, particularly when the market can infer whether a buyer or a seller is moving it. And when the stock is thinly traded, auctions really show their worth in aggregating liquidity and minimizing signaling.

Consider this trade in Assembly Biosciences. In the five minutes before the CODA auction, a total of 6,000 shares changed hands, pushing the thinly traded stock up from $35.35 to 36.05. The CODA Block 30-second auction aggregated diverse liquidity, resulting in a single print of 5,900 shares—without moving the price. Again, CODA’s symbol-only alerts minimized market impact.

Assembly Biosciences, Inc. “ASMB” – October 3, 2018

Ok, but the NBBO on thinly traded stocks bounces all over the place, and auctions can’t do anything to help with that. Not so. If you know the price at which you’d happily trade your block, inside or outside the NBBO, initiate an auction! You have nothing to lose but your fear of leakage. You may get some or all of your order done, at that price or better. And if you don’t—try, try again (or let your algo do it). No one will know what you’re up to.

Consider this trade in Beazer Homes, where two earlier auction attempts shot blanks. Just one minute after the second auction finished, a separate natural initiated an auction of their own, and the alert brought the original order back in for a complete fill. The lesson is clear: your first try may not bring joy, but so what? CODA Block has a daily unique symbol hit rate of 33%—so give it another shot a bit later. Or try a more aggressive price. Victory goes to the persistent and the bold.

Beazer Homes USA “BZH” – October 2, 2018

Ok, but you cherry-picked your great trades. Not so. Consider this recent study by ViableMkts, their “CODA Block Execution Quality Report”: http://www.pdqenterprises.com/wp-content/uploads/2019/01/ViableMkts-CODABlockAnalysis-12-Month-final.pdf. ViableMkts independently examined twelve months of CODA Block trades, and their numbers back me up. The study concluded that initiating CODA auctions offered “a valuable tool for trading institutional size with little downside and potentially large benefits.”

Ok, so on-demand auctions are great, but I can’t afford to ignore good prices when I see them. Not to worry. Algorithmic solutions are available from your broker, or from CODA directly, that seamlessly integrate on-demand auctions with access to the continuous markets. You don’t have to give up the old to partake in the benefits of the new.

Businessman sitting frustratedly on decreasing graphic chart, business failure, crisis concept.

There’s no way to sugar coat it – trader bonuses were down in 2018.

Yet as an industry, Wall Street did well for itself last year, according to the latest report and estimates from New York State Comptroller Thomas P. DiNapoli. His office reported securities industry profits in 2018 were 11 percent higher than the previous year, but the average bonus paid to industry employees in New York City declined by almost 17 percent to $153,700.

DiNapoli’s office releases an annual estimate of bonuses paid to securities industry employees who work in New York City during the traditional bonus season. Bonuses paid by firms to their employees located outside of New York City (whether in domestic or international locations) are not included. The Comptroller’s estimate is based on personal income tax trends and includes cash bonuses for the current year and bonuses deferred from prior years that have been cashed in. The estimate does not include stock options or other forms of deferred compensation for which taxes have not been withheld.

“Despite a sharp decline in the financial markets in the fourth quarter of 2018, the securities industry still had a good year with increased profits and employment,” DiNapoli said. “Profits grew in 2018 and have nearly doubled since 2015. Bonuses declined in 2018, but the average bonus was still double the average annual salary in the rest of the City’s workforce. It’s too soon to say how the industry will fare in 2019, but trade tensions, a slowing global economy and greater economic uncertainty are all factors that could affect results.”

Despite increased market volatility, and the worst December for the Dow Jones Industrial Average since 1931, the industry had an 11 percent growth in pretax profits for the broker/dealer operations of New York Stock Exchange member firms (the traditional measure of securities industry profits). Profits totaled $27.3 billion in 2018 — up from $24.5 billion in 2017 — the highest level since 2010 and 81 percent higher than in 2015 after adjusting for inflation.

Employment in New York City’s securities industry increased by 4,700 in 2018 to 181,300 jobs, the highest level in a decade. With solid gains in four of the past five years, employment in the securities industry in the city is still 4 percent smaller than before the financial crisis in 2007. In contrast, the rest of the private sector in the city has grown by 25 percent since 2007.

The Office also reported:

* The 2018 bonus pool for securities industry employees who work in New York City declined by 14 percent during the traditional December-March bonus season to an estimated $27.5 billion. The bonus pool in 2017 was $32.1 billion, the largest since the 2007 financial crisis.

* The average bonus per employee in 2018 declined by almost 17 percent to $153,700 in 2018 because the pool was shared among a larger number of employees. In 2017, the average bonus grew by an estimated 18 percent to $184,400, driven in part by changes in the federal tax code that encouraged firms to move up payments to December 2017. The acceleration of payments into 2017 could have contributed to the decline in 2018.

* Industry profitability was driven in 2018 by higher net revenue, which increased by 6 percent to reach $163 billion. This was the fastest rate of growth since 2012.

* Trading revenue was up 22 percent during the first three quarters of 2018, but was down 6 percent in the fourth quarter. For the year, trading revenue was up 17 percent and accounted for 6 percent of total revenue in 2018.

* The average salary (including bonuses) in the city’s securities industry ($422,500 in 2017, the latest annual data available) was more than five times higher than the average in the rest of the private sector ($77,100). Nearly one-quarter (24 percent) of the industry’s employees in the city earned more than $250,000, compared with less than 3 percent in the rest of the city’s workforce.

* The industry accounted for less than 5 percent of the private sector jobs in the city in 2017, but it generated more than one-fifth of all private sector wages paid in the city. DiNapoli estimates that nearly 1 in 11 jobs in the city are either directly or indirectly associated with the securities industry.

Securities-related activities are a major source of revenue for both the state and the city. DiNapoli estimates that the securities industry accounted for 18 percent ($14 billion) of state tax collections in state fiscal year (SFY) 2017-18 and 7 percent ($4.2 billion) of city tax collections in city fiscal year (CFY) 2018.

Institutional investors are increasingly looking to their most trusted asset managers for market research, and are now more than ever finding that content via social media.

According to new data from Greenwich Associates, 22% of institutional investors from North America, Europe and Asia named trust in the brand as the most important factor in selecting an asset manager, compared to 21% citing the ability to achieve high returns.

Daniel J. Connell, Greenwich Associates“Our data shows that, increasingly, the best way create a trusted brand is by delivering insightful and relevant content through digital media,” says Dan Connell, Greenwich Associates Managing Director and co-author of the new report Investing in the Digital Age: Media’s Role in the Institutional Investor Engagement Journey.

In the report, Greenwich Associates data highlights how institutional investors are consuming and using content via digital and social media:

68% of investors used social media to research asset management firms in 2018, up from 36% in 2015.

63% of institutional investors now consume social media while less than half regularly consume finance-specific trade publications.

86% of investors say they take action on content they receive, with 41% doing so at least weekly.

Dan Connell, Greenwich Associates“While the ability of asset managers to achieve specific investment goals is paramount, they need to fully embrace and take advantage of the evolving media landscape,” says Brad Tingley Market Structure and Technology Analyst at Greenwich Associates and the report’s co-author.

Investing in the Digital Age: Media’s Role in the Institutional Investor Engagement Journey examines the investor’s journey throughout the manager selection process and analyzes the importance of digital media channels, the use of content types and formats, social vs. traditional news media, the trust factor, and keys to continuous engagement.

Mizuho Bank selects smartTrade as its core technology provider for their next generation FX platform.

Tokyo, Japan – 28th March 2019.

David Vincent, CEO, smartTrade Technologies

smartTrade Technologies, a global leader in multi-asset, end-to-end trading solutions for the sell and buysides, has been selected by Mizuho Bank Japan to deliver their next generation e-FX platform.

Mizuho required a proven end-to-end FX trading solution to strengthen their leading position via the addition of innovative functionality delivered with a quick time to market. Mizuho’s core requirements included an advanced and open out-of-the-box solution allowing them an easy injection of their own intellectual property, advanced algos and AI, whilst supporting them in constantly assessing new technologies to obtain further improvements.

smartTrade’s LiquidityFX platform has seen tremendous global growth and adoption in the past few years by providing low latency connectivity combined with sophisticated aggregation, execution, smart order routing, order management, distribution, analytics and risk management. By selecting the LiquidityFX solution, Mizuho Bank will centralise the aggregation process as well as optimising and internalising the management of their very significant FX flows. Not only will this generate considerable cost savings for Mizuho it will also create new opportunities for their clients.

Hiroaki Aoyama, Global Head of FX at Mizuho, commented: “We are pleased to announce that we have selected smartTrade’s solution for developing our core e-FX distribution system. The e-FX sphere, today, undeniably plays more than a central role within Mizuho Bank, both internally and through client facing channels. We would like to strengthen our FX business by partnering up with smartTrade and utilizing their LiquidityFX platform.”.

“After a thorough review process, we are very pleased that Mizuho has selected our LiquidityFX platform to support their e-FX growth. The combination of our low latency connectivity and execution stack combined with sophisticated pricing and distribution functionality will allow them to enhance their execution and risk management efficiency.” said David Vincent, CEO of smartTrade Technologies.

By Kathryn Zhao, Global Head of Electronic Trading, Cantor Fitzgerald

The electronic trading business is highly competitive. In my view, to build a competitive low-touch offering, one needs to, at least, tackle the following five key areas.

TECHNOLOGY

Over the last 20 years, the electronic trading technology landscape has experienced dramatic changes. Innovations in hardware, networking, and software have had an immense impact on the current state of the art. To truly stand out from the rest of the competition, an electronic trading product must perform from a latency and throughput point of view and be resilient to failure without compromising capabilities and quality of execution.

There is a prevalence of cutting-edge open-source libraries for almost everything that needs to be built. A tremendous amount of attention should be paid to reliability and failover. A comprehensive suite of automated testing and a sophisticated simulation environment is essential to validate and guarantee the quality of a product.

Buy-side firms clearly demand better performance and predictability of execution results, without sacrificing the ability to source liquidity, transparency and control of their executions. Connecting to a wide range of liquidity sources, selecting venues to route algorithmic child orders based on advanced analytics, regularly reviewing venue selection, and providing transparency of order routing logic are all integral parts of best execution and drivers of quality execution performance.

QUANTITATIVE RESEARCH

Advanced quantitative models are the cornerstone of a competitive electronic trading offering. It is the “brain” that drives the algorithmic behavior. Taking into account both historical and real-time market data, a limit order placement model determines when, where and how much quantity to place at any point in time throughout the order lifecycle, a venue-ranking model makes informed stock-specific routing decisions, and a volume profile model dynamically tilts towards either a front-loaded or back-loaded distribution of volume.

One should choose the most suitable models for every situation. We treat our order placement problem as a Markov Decision Process solved by dynamic programming technique. This provides a mathematical framework that can naturally integrate various sub-models to address different aspects of security trading, in particular, market microstructure models, such as spread dynamics, fill probability and adverse selection, all modeled with thorough statistical analysis. Short-term signals can also be easily incorporated into the framework.

At every state, an optimal decision among crossing the spread, improving the best quote, joining the best quote, placing deeper in the order book, and staying away from the market will be selected in order to minimize trading cost.

The use of market microstructure models and dynamic programming technique makes a number of well-known optimal decision concepts become the natural outcome of an order placement model in a quantitative manner:

1. Opportunistically cross the spread when the spread is tight or the market is moving in the same direction as

the algo trading activity.

2. Remove the order from the market if there is significant adverse selection or the market is moving in the opposite direction as the algo trading activity.

3. Step into the spread to improve fill probability while still capturing the spread.

ONBOARDING

FIX connectivity/Vendor certification/Client onboarding is one of the most crucial elements to get right in the electronic trading business. Seamless certification reduces the number of issues down the road, and proper set up of FIX connectivity and tag translations creates a positive client experience, with a reduced number of rejects and erroneous algorithmic behavior. In addition, expedited response to FIX inquiries enables electronic sales and coverage to respond to clients’ demands in a timely manner.

Kathryn Zhao, Cantor FitzgeraldCUSTOMIZATION

No two buy-sides’ needs are exactly the same. Modern, competitive electronic trading offerings are required to deliver customized solutions tailored to each client’s specific trading preferences.

With growing sophistication of quantitative models and ever-increasing electronic solution varieties, buy-side firms face a unique challenge: how to choose a product that is straightforward to use and yet easy to customize.

The first question one should ask when evaluating a provider’s electronic offering is whether it has the capability to quickly customize its product to meet all the requirements and what level of customization can be achieved. There are roughly three types of customizations:

1. Customize within a particular algorithm and adjust parameters and behaviors based on price, time, or other market conditions;

2. Customize across algorithms, i.e., switching between different algorithms based on certain signals or

market conditions; and

3. Bespoke algorithmic offering based on specifications from buy-side firms.

Customization needs to be done expediently to enable the buy-side to take advantage of market dynamics as they occur.

On top of that, it is necessary to build a flexible experimentation framework that allows conducting A/B (randomized test running two versions side-by-side) test and an advanced analytics framework that enables generation of performance statistics easily. Only doing so will ensure having a complete circle of capabilities for a modern customization framework.

SERVICE

Electronic trading is a “low-touch” business with “high-touch” service. The most competitive service model would be a combined approach of low-touch speed to market and high-touch level of consultancy. As the number of providers, algorithms, and venues grow, it is increasingly important for sell-side firms to provide a high level of customer service to their electronic trading clients. In order to deliver “high-touch” service, one needs to have proper sales trading tools, capable FIX support personnel, and dedicated algorithmic support staff to answer buy-sides’ inquiries on the fly.

What is “high-touch” service?

• Stay on top of trade blotter and watch orders closely: orders that are not executing, orders that are falling behind the schedule, performance metrics (slippage against Arrival Price, Interval VWAP, etc.), orders that are causing impact, orders that are getting poor fill rates, stocks that are on the move, etc.

• Provide prompt responses to Instant Bloomberg messages and client inquiries.

• Most importantly, catch things that clients care about (even if it is not good news) and bring issues to their attention.

• Provide actionable suggestions.

An algorithmic product is only as good as the people behind it. “High-touch” service means the algorithmic coverage is clients’ eyes and ears, and provides them with value-added information in a frequency acceptable to them.

Enabling/papering the client is step one, getting the client to trade is step two, retaining and increasing the clients’ business is step three. Simply getting the client to send an order on auto pilot mode is not something that will retain clients, and more importantly, increase the clients’ flow.

The FIX Trading Community EMEA conference opened with Verena Ross, Executive Director, ESMA, as the keynote who set the stage for the event by bringing clarity on how the industry can move forward in the event of a no-deal Brexit.

Verena’s message touched on the main areas of how ESMA is preparing for a no-deal Brexit scenario in an effort to limit the risk to financial markets ahead of 29th March. She also shared examples surrounding the framework of MiFID II/MiFIR implementation under the transparency regime provisions, including the unbundling of research and the costs absorbed directly by asset managers.

Verena then touched on the importance of LEIs and their essential role in market surveillance and transparency. She stressed the importance of data quality and data standards, and how there is still a need for a Consolidated Tape Provider (CTP). Verena’s speech ended with the connection between Brexit and MiFID II and the impact Brexit will have on the transparency regime to suit the EU27 requirement.

l to r: Matthew Coupe, Philippe Guillot, Fabio Braga, and Rebecca Healey

Speakers: Matthew Coupe, Co-Chair EMEA Regional Committee & EMEA Regulatory Subcommittee, FIX Trading Community, Director, Barclays Investment Bank Philippe Guillot, Managing Director, Markets Directorate, Autorité des marchés financiers (AMF) Fabio Braga, Manager, Trading and Post Trade Policy Team, FCA Rebecca Healey, Co-Chair EMEA Regulatory Subcommittee, FIX Trading Community, Head of EMEA Market Structure and Strategy, Liquidnet

The morning followed with the session – ‘Brexit – What next for the Industry’, to address the practical implications of what firms now need to do, and how they will trade after liquidity settles. The panel discussed the challenges of Traded on a Trading Venue (TOTV), Financial Instrument Reference Database Systems (FIRDS), market data, Share Trading Obligation (STO) and liquidity. It was acknowledged that there are systemic challenges ahead, and the unpredictable political climate continues to provide uncertainty. When it comes to complying with any future requirements, regulators are aware that it can be harder for small firms to comply with what is coming but have higher expectations for larger firms. When it came to TOTV and the possible fragmentation between the UK and the EU with regard to transaction reporting, there were no quick solutions; all agreed that a no-deal Brexit would create challenges for trade reporting.

With ESMA phasing out UK data over time, the issue of cleaning up market data was seen as critical as the risk of divergence increases, depending on market structure post-Brexit and the ability of firms to trade cross-border in a different way. The FCA has issued a Post Trade Transparency Policy and encourages firms to engage on roundtables with the FIX Trading Community shortly after Brexit in order to pick their way through the implications. The message loud and clear was to keep talking to regulators and to carry on interacting with the FIX Trading Community and trade associations over the coming months.

l to r: Philippe Guillot, Tim Kreutzmann and April Day

Moderator: Robert Barnes, Chief Executive, Turquoise

Speakers: Ross Barrett, The Investment Association Fabio Braga, Manager, Trading & Post Trade Policy, FCA April Day, Managing Director, Head of Equities, AFME Philippe Guillot – Directeur des marches, AMF Tim Kreutzmann, VP of Legal, BVI

During this morning session on the evolving equity landscape, a panel of experts discussed a range of topics including how liquidity in dark pools has diminished whilst there has been an increase in activity in frequent periodic auctions; although there is still notable activity on non-lit markets. Post MiFID II, market participants have access to more data across a broader set of asset classes; we can see exchange traded funds, for example, in a way we couldn’t under MiFID I. It was noted, however, that we still have issues with the quality of market data, but from the data that we do have access to, it has been a story of evolution rather than revolution.

Concerns continue to persist about liquidity fragmentation and post trade transparency post Brexit, with many market participants frustrated with what they see as a lack of regulatory guidance around what to do in the absence of equivalence between the EU27 and the UK. Panellists also warned that some politicians seem to be using the share trading obligation rules to drive liquidity from the UK to Europe, which could see an increase in costs for end investors.

l to r: Christoph Hock, Nick Philpott, David Lawlor, Gareth Coltman and Richard Wire

Speakers: Christoph Hock, Head of Multi-Asset Trading, Union Investment Privatfonds GmbH Nick Philpott, Head of Market Structure, Standard Chartered David Lawlor, Head of Regulatory Products, TP ICAP Gareth Coltman, Head of European Product Management, MarketAxess

This session addressed the use of Market Data and the perspective, from both the sell side and buy side, on the benefit of the data transparency regime. Whether data is being used to input into pricing, trade surveillance or valuation of control, there is still a big need to understand and be educated on where the data is coming from and how best to use the data. The consensus from the session was that firms are having to become more data savvy and understand where they get the data from i.e. Trading Venues and the number of venues and further sources.

A further challenge is how to integrate the data into the trade lifecycle. Additionally, the consensus was that the cost of data is still relatively high (in particular in Fixed Income) and the industry challenge remains on how to collate and aggregate the data and turn that data into something meaningful. The three main concerns from the panellists regarding data transparency were the underlying quality of the data, the source from where it comes and consistency on how the data gets reported.

l to r: Christoph Hock, Matt Cousens, Severine Vandelanoite, Jon Finney, Mark Hemsley and Huw Gronow

Moderator:

Huw Gronow, Head of Dealing, Newton Investment Management (Chairperson of the EMEA Investment Management Subcommittee, FIX Trading Community)

Speakers:

Christoph Hock, Head of Multi-Asset Trading, Union Investment Matthew Cousens, Head of EMEA Execution Sales, Barclays Severine Vandelanoite, Senior Vice President, Products and Regulation, Deutsche Borse Jon Finney, Director of European Business Development, Citadel Securities Mark Hemsley, President, CBOE Europe

In a panel session on the practitioner outcomes for the evolving equity landscape, there were similar points made from the earlier equity stream, making it clear that these are the issues that are at the front of everyone’s minds. Panellists discussed how a lack of clarification on the Share Trading Obligation (STO) was causing serious concerns for the market. One panellist stated that a further assessment was needed with specific regard to the ‘trading on a trading venue’ (TOTV) rules, and how badly both liquidity and post trade fragmentation across Europe could become. The cost to the buy side (and the end investor) was underscored once more. The appropriate use of frequent periodic auctions and systematic internalisers was again discussed in this session, where panellists felt the regulator should simply look at execution quality, as it is the job of a buy-side trader to deliver ‘best in class execution’ to both portfolio managers and investors.

MiFID II has given a complex, but widely-understood, set of rules to follow for buy-side traders and concerns were raised about any subsequent plans to change this yet again. The buy side stated that it is essential for the regulator to appreciate the complexity of price formation, specifically, concerns relating to information leakage, of secondary markets and the reason that traders use systematic internalisers. Regulators were encouraged to look at the trading ecosystem as a whole, as opposed to focusing purely on one or two trading methods.

Moderator:

Carl James, Global Head of Fixed Income Trading, Pictet Asset Management

Speakers: Sassan Danesh, Managing Partner, Etrading Software Ltd Ian Morgan, Managing Director Head of Sales EMEA, Fenics UST Mario Muth, Head of Electronic Trading, Deutsche Bank Paul O’Brien, Senior Product Manager, MTS Markets

This fixed income session reflected on the eco structure which isn’t new but is ever evolving. It addressed the recent trend in the market of having to be more innovative in using technology in order to aggregate the data and for the liquidity takers to look at new ways to better connect with liquidity providers to access their liquidity. The panellists highlighted how more asset managers are investing in technology to automate their trade flows, in particular on fixed income government bonds.

Asset managers are now looking at alternative trading methodologies such as streaming prices, firm pricing, high frequency trading (HFT) and alternative liquidity providers in addition to the trading Request for Quote (RFQ) protocol. The methodology chosen continues to depend on the liquidity chain of the product. The traditional RFQ continues to be used widely, but the direction of travel is leaning towards modernising and looking at new ways to facilitate alternative pricing and sources of liquidity.

l to r: Carl James, Ivan Mihov and Jonathan Gray

Moderator: Matthew Coupe, Co-Chair EMEA Regional Committee & EMEA Regulatory Subcommittee, FIX Trading Community, Director, Barclays Investment Bank

Speakers: Carl James, Global Head of Fixed Income Trading, Pictet Asset Management Ivan Mihov, Head of Buy-Side Fixed Income EMS, Axe Trading Jonathan Gray, Head of Fixed Income (EMEA), Liquidnet

In a panel session on finding the alpha in execution, delegates heard how MiFID II has pushed more trading electronically, but traders still want options – including voice trading for larger trades. The regulation has incentivised buy-side traders to ‘show their workings’ which has been good for the end investor. The panellists discussed how there has been a blurring of the Portfolio Manager and dealer role within fixed income; while dealers still aren’t taking the end decision, they are increasingly being asked to put forward ideas about the best way to gain exposure to a wide selection of asset classes.

When discussing technological advancements, attendees heard how buy-side trading desks can increasingly become a source of alpha thanks to new technology and understanding of complex data sets. However, the industry needs to do more work on API development and integration. There have been many platform launches, but concerns remain about connectivity and levels of sophistication. Panellists said that technology is also enabling liquidity to come to the trader for the first time, which allows traders to be further up the curve. It means that dealing desks are able to discuss a much broader range of options with portfolio managers prior to execution.

Rebecca Healey, head of market structure & strategy, EMEA at Liquidnet, has warned that European asset managers have real concerns on retaining access to liquidity following guidance on how investment firms in region should implement the share trading obligation under MiFID II in a no-deal Brexit.

The MiFID II regulations, which went live in the European Union at the start of last year, require shares listed on venues in the region to be traded on regulated markets or on third-country venues deemed equivalent by the EU Commission. If the UK leaves the EU without a deal there will be no equivalence and EU asset managers providing MiFID II services will not be able to access UK venues, including systematic internalisers.

Rebecca Healey, Liquidnet

“For European asset managers in particular, this represents real concerns on retaining access to liquidity,” wrote Healy. “Many European firms are in the process of repapering with their counterparties in the UK and Europe to ensure that they have continued access to liquidity in the relevant jurisdiction, an exercise which is both time consuming and costly.”

Yesterday the European Securities and Markets Authority published long-awaited guidance on the share trading obligation and said it will extend to UK-listed shares deemed to be “liquid” in the EU. Esma listed the 14 stocks affected which include BP, Royal Dutch Shell and Vodafone Group.

🆕 ESMA publishes statement on the application of the share trading obligation #MiFIDII in a no-deal #Brexit without an equivalence decision for the UK

ℹ️ Provides additional clarity & certainty to market participants on application of TO for shares pic.twitter.com/OvRsyX4p9a

— ESMA – EU Securities Markets Regulator 🇪🇺 (@ESMAComms) March 19, 2019

Nick Burchett, UK equities manager at Cavendish Asset Management, said in an email to Markets Media: “In the event of a hard Brexit and Esma getting its wish for UK stocks to be traded inside the EU, all this will do is further fragment equity trading across Europe. This is slightly ironic given that fact that the whole point of Esma’s creation of MiFID II was to increase transparency across markets. But how on earth does having numerous stocks listed across multiple different locations help with transparency ?”

Chris Cummings, chief executive of the Investment Association, said in a statement that the guidance falls short of the broad equivalence the market needs in order to avoid fragmentation and a reduction in market liquidity.

“This does not represent a good outcome for our industry, or for savers and investors whose money we manage,” he added. “In the event of a no-deal exit, the solution outlined today may leave firms unable to efficiently trade in the market and at the very least will lead to significant operational issues for firms executing orders.’

Analysis

Anish Puarr, European market structure analyst at Rosenblatt Securities, tweeted that the broker had analysed the 14 stocks with GB ISINs that will be subject to the MiFID II share-trading obligation in the event of a no-deal Brexit or lack of equivalence.

Only three of these issues had >50% market share on EU venues in 2018. Hard to believe that some of the EU versions of these stocks are deemed "liquid" enough to prevent EU firms trading them in the UK.

Esma said in a statement that it recognises that its approach may lead to an overlap of trading obligations for a number of shares and potentially a greater level of fragmentation of trading should the UK apply an identical approach.

“However, the absence of any clarification by Esma would by default lead to the application of the MiFIR trading obligation to every share traded in the EU27,” added Esma. “Esma’s approach seeks to limit potential market disruption while also ensuring Article 23 MiFIR is adequately and consistently applied across the EU.”

Esma stressed that the guidance should only be applied in case of a no-deal Brexit occurring next week on 29 March.

FCA

The UK Financial Conduct Authority said in a statement that the onshoring of EU legislation in preparation for Brexit means that the UK will have a share trading obligation that, based on current trading data, would mean there would be a large degree of overlap between the UK and EU obligations.

FCA response on ESMA guidance on impact on TO in case of no deal brexit , https://t.co/qXw2ekH5gg

“This has the potential to cause disruption to market participants and issuers of shares based in both the UK and the EU, in terms of access to liquidity and could result in detriment for client best execution,”added the UK regulator. “We therefore urge further dialogue on this issue in order to minimise risks of disruption in the interests of orderly markets. The FCA stands ready to engage constructively with Esma and other European authorities to achieve this.”

Healy continued that the guidance opens the possibility to a new ISIN, a type of securities identifier.

“The latest political response to Brexit negotiations may yet deliver what policy makers least expect, regrettably it looks as if end investors may bear the brunt of how future liquidity formation plays out in practice,” she added. “One to watch as Brexit negotiations continue.”

Christian Voigt, senior regulatory adviser at Fidessa, said in a blog that market participants had hoped for a more practical approach and are disappointed in a new regime that prevents EU27 investment firms from trading stocks such as Vodafone in London after a no-deal Brexit.

“While arguing what the regulator could have done, we shouldn’t forget that it is all caused by a political decision not to grant equivalence,” he added. “Esma’s new regime is poorly suited for a smooth day-to day-operation of markets. For example, what will happen after the EU revokes the equivalence decision with Switzerland in a couple of months? This is not what principle-based regulation looks like.”

The FICC Markets Standards Board is continuing to review structural and conduct risks in electronic trading, government bond auctions, the sharing of allocation information in primary bond markets and the management of large trades as it has taken action on more than half the issues identified in the initial strategy.

The FMSB was set up in 2015 after the UK authorities’ Fair and Effective Markets Review of poor market practice in many fixed income, currency and commodities markets following scandals in foreign exchange and the setting of Libor interest rates. The market-wide body was formed under the sponsorship of the UK Treasury, the Bank of England and the Financial Conduct Authority and includes corporate issuers, asset managers, exchanges and investment banks.

Mark Carney, Bank of England

Mark Carney, governor of the Bank of England, said in a statement: “UK authorities have used their convening powers to encourage market participants to establish standards of market practice that are well understood, widely followed and, crucially, that keep pace with market developments… But the authorities cannot future-proof alone. In particular, the FMSB is undertaking horizon scanning for future misconduct risks through its innovative Behaviour Cluster Analysis.”

This week the FMSB issued its latest annual report covering the period from August 2017 to December last year.

“One of its key conclusions was that there was insufficient, practical and clear guidance available to market practitioners as to how they should operate in the best interests of their clients,” said the report. “Some critics at the time even talked about a crisis of confidence amid concerns that bad behaviour was more widespread than had been generally appreciated.”

Initially the FMSB identified 72 potential topics and issues to examine in wholesale FICC markets and has taken action on 53%, or 38. The body has also published 13 standards and statements of good practice.

Mark Yallop, FMSB

Mark Yallop, chair of FMSB, said in the report: “FMSB has made significant progress during this period due in large part to the commitment of the board and FMSB members.”

Yallop is an external member of the Prudential Regulation Committee and the Financial Market Infrastructure Board at the Bank of England. He was UK group CEO for UBS from 2013 to 14; group COO for ICAP from 2005-11 and previously spent 20 years at Deutsche Bank.

The report continued that in the next three years FMSB will move beyond the pure market conduct agenda to address broader market structure questions; develop metrics to demonstrate the effectiveness of its standards in supporting fair and effective markets; and review its international engagement.

FMSB Annual Report 2018 has been published today and sets out progress made to enhance standards of behaviour in the wholesale Fixed Income, Currencies and Commodities (FICC) markets. Follow the link: https://t.co/Ikcrx9TxWy

For example the electronic trading and technology committee is considering 12 topics including change management and control, integration with risk data infrastructure, conduct issues in algorithmic trading, systemic risks to market liquidity and the design of market mechanisms.

A working group is considering the the management of large trades including pre-hedging, disclosure and relevant procedures and market making obligations.

“Alongside the published materials, FMSB has a significant amount of work in progress, such as reviews of structural and conduct risks in electronic trading, government bond auctions, the sharing of allocation information in primary bond markets, the management of large trades and the conduct of precious metals fixes,” added the report.

This report explores the global fixed income e-trading trading venue landscape. Building on the findings of previous bonds e-trading venue reviews, this report significantly expands the scope of its research for this report – generating over 12,000 data points from over 125 venues – as the basis for its quantification of the ongoing shift in fixed income markets. Reviewing the venue data through a multitude of analytic lenses, the continued advancement of all-to-all (A2A) trading at the expense of the historic broker-dealer-centric trading model is evident across both single- and multi-tiered matching methodologies.

Market intelligence provider Greenwich Associates found that between 2014 and 2018, there was a 50% increase in the median size of clients’ broker-dealer volume reallocations in US equities. Its paper entitled ‘Customer Retention in the Age of Electronic Trading’ is based on 15 interviews with asset managers in the US and Canada.

Ken Monahan, Greenwich Associates

“The buyside has been weaponising their transaction cost analysis infrastructure, turning it from a compliance tool into a trading tool,” said Ken Monahan, senior analyst at Greenwich Associates. “This has significantly raised the bar for the sellside by enabling the buyside to measure outcomes precisely and to evaluate relationships accordingly.”

Greenwich Associates argued that the stability of dealer-client relationships is eroding over time and that bulge-bracket firms are losing their relative stability advantage. Although Greenwich Associates identified stability at the top of the Greenwich Share Leaders, it found considerable instability at the individual broker-client relationships level. It claimed that at the median, buy-side firms regularly change a given broker-dealer’s share by a third year over year.

The report attributed these developments to increased scrutiny of executions by the buyside, which is using tools that were originally developed to prove best execution to optimise trading. Greenwich Associates stated that buyside firms are able to observe broker-dealer performance and specify what execution factors influence their profitability with growing sophistication.

Greenwich Associates concluded that a number of lessons for the sellside exist. While the breadth of the client base is more important than the depth of client relationships to top firms, all firms want to reduce their customer market share volatility. The market intelligence provider predicted that broker-dealers will invert their clients’ methods, making use of their larger volumes to fashion client behaviour so that they can address issues before clients detect them.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.

Speakers:

Speakers: