The Financial Conduct Authority (FCA) has approved JP Jenkins as a PISCES operator.

JP Jenkins provides a platform for private and unlisted company securities to be issued and traded. It reported capital and reserves of £247,275 at year-end 2022, its most recently available results. This marked a 25% increase year-on-year.

It was acquired by fintech InfinitX last year, making it a fully electronic trading platform. InfinitX reported capital and reserves of £143,891 for financial year 2024, recovering from 2023’s -£1,064.

A number of companies active on JP Jenkins delisted from the London Stock Exchange over recent years to join the platform, including Superdry, Prax Hurricane and iEnergizer.

Existing JP Jenkins member companies will be able to transition to the PISCES market if eligible. Currently the firm offers a match-bargain facility, which connects buyers and sellers using expressions of interest.

“JP Jenkins played a leading role in the design of PISCES,” the company stated.

Mike McCudden, CEO, added, “We have worked at pace to get this project over the line.”

LSEG was the first company to be approved as a PISCES provider, and also had an active role in the development of the service. In October, it announced that it would use ION’s Fidessa platform to support its PISCES auction events.

The regulatory framework for PISCES platforms is being tested in a sandbox, and will be reviewed by HM Treasury by June 2030. It will then be decided whether the framework is transferred into permanent legislation.

Yarkova-Valente has close to 25 years of industry experience and joins the firm from MTS Markets, where she has been a sales executive and senior sales manager since 2013.

Earlier in her career, she was a sales executive and business analyst at the London Stock Exchange Group.

Daniel Dempsey, head of UK market making, GTS Securities Europe

Daniel Dempsey has joined GTS Securities Europe as head of UK market making.

Based in London, Dempsey is responsible for building out the firm’s UK market making desk.

Parent company GTS Securities is a NYSE designated market maker. It also market makes in ETFs and wholesale and covers fixed income and FX.

Subsidiary GTS Securities Europe reported a US$496,761 loss for the financial year 2024.

Dempsey has 25 years of industry experience and joins the firm from Iress, where he has been a senior account manager since 2023. Prior to this, he was a UK market maker at Stifel.

Earlier in his career, Dempsey was director of equity trading at KBW and UK head of trading at Pictet Global Markets.

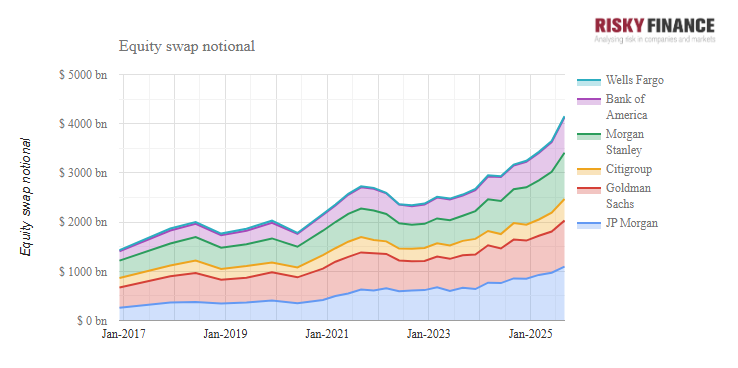

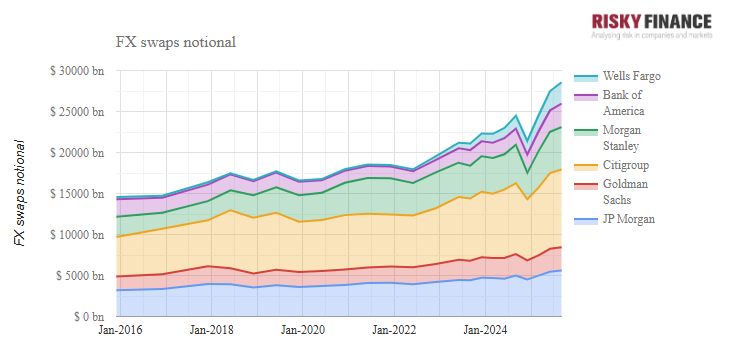

Notional amounts of equity swaps at the largest six US banks reached $4 trillion in September, while FX swaps hit $25 trillion as dealers sidestepped cash trading for bilateral over-the-counter derivatives.

Their use is controversial among the buyside, and the Bank for International Settlements thinks they are a source of systemic risk. But OTC equity and FX swaps keep growing on bank balance sheets, while a summer lull in trading losses appeared to vindicate the banks’ growth strategy.

According to Risky Finance analysis of Federal Reserve filings, the equity swap exposures of JP Morgan, Bank of America, Citigroup, Wells Fargo, Goldman Sachs and Morgan Stanley reached $4 trillion at the end of September, led by JP Morgan with $1.1 trillion notional of equity swaps and Goldman with $934 billion.

This compares to $800 billion of equity securities held by the same six banks at the end of the third quarter, meaning that each dollar of cash equity exposure was matched by five dollars of derivatives, including long and short positions. This comparison does not include equity futures or option positions.

With non-bank market makers such as Citadel Securities or Jane Street now dominating cash equity trading, bank-owned dealers have an advantage when it comes to derivatives, with their leveraged balance sheets allowing them to post collateral supporting their trillions of notional exposures. This gives them flexibility to noiselessly take on single stock or basket exposures on behalf of clients. However, there is concern among buyside firms that pre-hedging of orders by banks amounts to a form of front-running.

Having conceded much of cash trading to newer competitors, the banks drive to keep up using equity swaps forces them to increase exposures as market valuations reach eye-watering levels on the back of the AI boom. In the past year that has caused some firms like JP Morgan to repeatedly breach value-at-risk limits, attracting the attention of Fed regulators. However, that was not an issue during the third quarter, with none of the top six US banks reporting a VaR breach.

Meanwhile, FX swaps also grew to a record, led by Citigroup which had $9.5 trillion of the contracts. The contracts involve an exchange of currencies at the outset along with a forward agreement to swap them back again in the future. They are the most heavily traded FX derivatives in the market, with $4 trillion daily turnover in April 2025, according to the Bank for International Settlements.

FX swaps can be used to hedge the currency risk in equity exposures, but their main use is in yield enhancement for cash portfolios. The BIS has warned about the systemic risk of FX swaps based on their similarity to cross-border repo, although this has been disputed by academics.

Market as a Service: A New Model to Transform Exchange Performance

David Mellor, MEMX.

Long term partnerships and world class reliability require forward thinking engagement models, writes David Mellor of MEMX.

In the past 25 years, the exchange landscape has become more competitive than at any point in the previous century. An industry that began 400 years ago is being transformed by technology that has moved from a supporting function, to a strategic differentiator. As exchanges strive to deliver liquidity, information and confidence, their underlying infrastructure becomes a critical factor in determining their appeal to members.

Reliability may not be the flashiest topic in financial technology, but it is unequivocally the most important. For exchange operators, reliability is not just about uptime it is about trust. Clients rely on exchanges not only to execute trades but to provide credible, uninterrupted access to market data. Predictability builds client confidence and reduces operational risk.

At the heart of this reliability is the engineering of the matching engine. In an environment where exchanges are expected to be up 100% of the time, even minor outages can erode market share and damage reputations. Uptime applies not only in trade execution but also to data dissemination. Clients need to know the information they receive is accurate, timely, and consistent.

Strength through elasticity

The right architecture for an exchange supports long-term growth by ensuring that performance remains stable even under stress. This is particularly critical in today’s fragmented market environment, where exchanges must compete on more complex pricing and latency sensitive services to different market participants.

The wider the base of users, the more diverse the set of instruments that are selected to trade. Multi-instrument and multi-asset capabilities allowing exchanges and venues to offer cash products for equities and fixed income alongside derivatives, on a unified platform. This flexibility is crucial for operators looking to expand their product offerings or enter new markets.

Understanding clients’ strategic goals over the longer term is key, and the ability to follow the growth of exchange traded products (ETPs) and their cross over with the underlying instruments can make or break a trading venue’s future potential. Customisation and strategic alignment of an exchange’s offering with those of its clients is emerging as a valuable attribute.

The art of the possible

If the technology underpinning an exchange allows it to tailor its trading environment to specific use cases, whether supporting dark pools, auction mechanisms, or bespoke order types, the platform needs accommodate an exchange’s diverse requirements without compromising performance.

Speed-to-market is increasingly vital, especially as new exchanges seek to differentiate themselves with niche offerings, or a focus on a specific asset class or region. Using technology with a modular design supports rapid deployment, enabling operators to go live in weeks rather than months seizing opportunities as they present themselves.

Legacy technology can be a barrier to developing a dynamic new exchange. Being more rigid, expensive to maintain, and ill-suited for exponential growth, legacy systems require periodic ‘big bang’ upgrades that disrupt operations and introduce new risks.

The most limiting element here is software ‘mortality’; the need to refresh systems in their entirety to create a generational difference and evolve the exchange’s services.

Building With an Eye Toward the Future

Getting past this barrier requires a new deployment model that supports more dynamic deployment of capabilities, without a reliance on disruptive, monolithic changes to the core systems.

The ‘market-as-a-service’ model eliminates this pain by offering elasticity, scaling resources up or down as needed, and delivering incremental improvements without increasing downtime. It moves beyond traditional software licensing to offer exchanges a fully managed, continuously upgraded platform, providing operational support while lowering costs and reducing risk.

Breaking free of ‘software mortality’ moves an enterprise into the realm of ‘software immortality’. Unlike traditional software, which suffers from a fixed lifespan and eventual obsolescence, market-as-a-service ensures that a platform evolves continuously and removes clunky generational changes. This not only enhances performance but future-proofs the exchange against technological shifts.

Aligning technology with client strategy

The best technology is about deployment as much as it is about systems. It offers more than tools, it offers enablement. By understanding the strategic goals of its clients, whether they are launching a new exchange, expanding into new asset classes, or optimising existing operations, they need a provider that delivers solutions that support those ambitions.

Technology should be a facilitator, not a constraint, with an architecture that allows clients to innovate without being held back by legacy limitations. This is particularly important in a market where differentiation increasingly comes from strategic positioning rather than technical specifications alone, with direction, speed and strength of build all fundamental factors in the delivery of an effective strategy.

As exchanges face increasing pressure to innovate, reduce costs, and maintain trust, platform providers can offer a blueprint for success, in partnership with the vision of the exchange leadership. By aligning technology with strategic goals and embracing continuous improvement, exchange operators can not only survive but thrive in a rapidly evolving capital markers landscape.

Almost 20 years after MiFID decentralised UK equity markets, the Financial Conduct Authority (FCA) has opened its consultation on the UK equity consolidated tape. The regulator proposes a tape integrating post-trade data with attributed best bid and offer quotes from all UK venues, and acceptable latency to dissemination of 150 milliseconds.

The FCA proposes a single consolidated tape provider, appointed through a competitive procurement process. Its favoured design is a tape combining real-time post-trade data with pre-trade best bid and offer (BBO) data attributed to each venue. According to the regulator, this structure would provide a clearer and more comprehensive view of UK equity market liquidity. The consultation notes that UK liquidity is frequently underestimated when assessed only through central limit order books (CLOBs).

Alternative solutions are considered, including a post-trade-only tape, delayed-data models, and a multi-provider architecture. The consultation weighs trade-offs around deeper pre-trade transparency and seeks views on the proportionality of new latency obligations. Proposed latency standards for data contributors are 50ms for both pre- and post-trade submissions at a 95% confidence interval. The regulator’s view is that this would enable dissemination of the tape within 150ms.

The consultation follows CP23/15, published in 2023, but provides far more granularity, drawing on analytical work already completed during the bond tape process. Since 7 May, the FCA has been engaging with the market under a preliminary engagement notice indicating a total project value of between £50 million and £60 million.

Stakeholders are asked to comment on whether additional pre-trade depth should be incorporated over time; how regulatory data fields should align with EU standards; how historical data should be structured; and what obligations the consolidated tape provider (CTP) should have regarding data quality, error detection and corrections. The FCA also seeks views on how best to ensure the tape reflects “addressable liquidity”.

In addressing market sentiment, the FCA acknowledges pressure for greater cross-border alignment. The consultation states: “Another wider issue to consider is the consistent theme in conversations with market participants that they would ideally like a CT that covered the UK, EU and Switzerland… some market participants are also keen that the UK equity CT should be based on the same requirements as those that apply to the CT and CTP in the EU.”

Arianne Collette, head of US equities, Depository Trust & Clearing Corporation (DTCC).

The Depository Trust & Clearing Corporation (DTCC) has appointed Arianne Collette as a managing director and head of US equities as it continues to build its presence in the asset class.

In the newly-created role, Colette is responsible for strategic planning and execution, market expansion and growth of the business’ clearing and settlement infrastructure. Based in Jersey City, she reports to managing director and global head of equities solutions Val Wotton.

Earlier this year, DTCC announced that 24/5 clearing of US equities would be available through the National Securities Clearing Corporation (NSCC) from Q2 2026 as the journey to 24-hour trading accelerates.

Collette joins DTCC after 24 years with major liquidity provider Morgan Stanley, where she has held senior roles including chief operating officer and head of strategy for reinvestment in the business’ wealth management division, global head of sales strategy, and Americas head of firm-secured funding. Earlier in her career, Colette was a sec lending and collateral finance sales trader, and a fixed income repo trader.

Wotton commented, “[Collette’s] deep industry expertise, strategic vision, and commitment to innovation will be invaluable as we continue to deliver solutions that enhance market resiliency and efficiency for our clients.”

ESMA’s move from the double to single volume cap was promoted as an easing in regulation. But systematic internalisers say the move will result in dark volume moving to periodic auctions, harder to tailor liquidity provision in bilateral relationships, and an equally opaque post-trade liquidity picture.

ESMA’s latest equity-market transparency package is now in its implementation phase. It brings two interconnected changes to European equities trading: the double volume cap has been retired for a single EU-wide volume cap on dark trading and increases pre-trade quoting obligations for the new “opt-in” systematic internalisers (SIs) have been upgraded.

Under previous versions of MiFID II, investment firms could be pushed into SI status once their dealing activity passed ESMA’s quantitative thresholds. Under the revised framework, firms can now choose to declare themselves an SI for a given instrument or class. Optiver did so in March 2025.

When it proposed the new pre- and post-trade transparency regime, ESMA said: “[The package] aims to contribute to a more informative pre-trade and post-trade transparency regime.”

While the move to a single volume cap reduces reporting burden and makes it easier for dark trading caps to be put in place directly by venues, in the UK, the FCA has removed the volume cap altogether. The FCA has not moved like ESMA in upgrading the standard market size requirements in pre trade transparency.

The new single-volume cap pushes dark volume to periodic auctions

The main change for venues and brokers is the replacement of the double volume cap with a single cap for trading under the price waiver, allowing stocks to trade in dark. Instead of checking both a per-venue 4% limit and an EU-wide 8% limit on trading under the reference-price waiver, ESMA now aggregates all European trading volume from every venue to determine if more than 7% of stocks have traded in dark. Once an instrument breaches that level, use of the waiver is suspended across the Union for 3 months.

Several electronic liquidity providers have pointed out to us that this dark volume moves straight into periodic auctions. One SI active in streaming to the buyside put it bluntly: “You’re not shrinking dark demand; you’re just relocating it to something ESMA hasn’t capped.”

This can already be seen in the data since the new single-volume cap list got posted on 10 October. Since the new cap was introduced, the proportion of addressable liquidity traded in periodic auctions, according to BMLL Vantage, has risen by a third from 6.3% to 8.1%. Mirroring this change, dark volumes have fallen from roughly 8% to 6%

Adressable liquidity pre and post new SVC

New pre-trade transparency requirements impact ELPs’ ability to tailor the size of their streamed quotes

The most operationally burdensome piece is the new pre-trade transparency requirement for SIs.

ESMA’s stated goal was to enhance pre-trade transparency for systematic internalisers because it said that:” allowing SIs to quote at 10% of SMS “has led to very low levels of pre-trade transparency.”

ESMA has changed the standard market sizes (SMS) that define how much an SI must be prepared to show on both sides of the market while streaming quotes. In the past, SIs had to bid and offer everyone at least 10% of the SMS and be prepared to fill all orders up to 100% of the SMS at that quote.

They now are forced to stream quotes at the full SMS, on a more granular scale, especially for smaller stocks with SMS sub-€10k. SIs must fill orders at that quote up to 2 times the SMS.

The Sis / ELPs we talked to said it would not be an issue to fulfil these new liquidity conditions, but it might make it harder to tailor the risk-adjusted liquidity profile they want to offer for individual clients.

New transparency requirements don’t bring a clearer liquidity picture

The ELPs we talked to, who wished to remain anonymous, said that while all these changes were costly in terms of constant compliance changes, they were ultimately not a threat to their bilateral liquidity provision ability.

They pointed out that, for a transparency package, they did not address the difficulty to understand the actual accessibility picture of European stocks liquidity: A large proportion of what is reported under the SI category is still broker internalisation of agency and swap flows that will continue to be reported off-book on exchange. Coupled with inconsistent flagging as coherent FIX flags are still not mandated by the regulator, prints that do not represent a genuine economic interest will likely continue to be accounted alongside genuine accessible liquidity and will not become more transparent because an SI somewhere else has lifted its SMS.

For liquidity providers that do run genuine bilateral risk, the new rules “make it harder to provide genuine risk” because they lock in a bigger public commitment without distinguishing between principal SIs and banks internalising for clients.

Matthew Evans has left his role as an equity fund manager and senior portfolio manager at Ninety One, after more than eight years with the firm.

He is now a member of the Global Growth Market advisory board, a project aiming to develop an international stock market for growth companies.

Based in London, Global Growth Market intends to give smaller, sub-US$5 billion companies access to public capital and a simplified IPO process. It intends to begin trading next year.

Commenting on his move via LinkedIn, Evans said, “I’ve stepped away from my role at Ninety One to pursue opportunities that allow me to support businesses more directly as they scale and evolve — and to help investors access the next generation of growth.”

He described the Global Growth Market as “designed to make public markets work better for entrepreneurs”.

Evans’ more than 25-year career has included fund manager roles at Threadneedle Investments and Legal & General Investment Management.

Wajih Ahmed has swapped Goldman Sachs for Balyasny Asset Management, joining the firm as a macro portfolio manager after more than a decade with the bank. He is based in London.

Balyasny Asset Management holds US$29 billion in assets under management. Earlier this year, the company appointed Stephen Peyser as global head of trading and capital markets.

Ahmed has almost a decade of industry experience, all of which has been spent at Goldman Sachs. He joined the bank as an inflation trading analyst in 2016, before becoming an associate and then vice president of inflation trading in 2020.