Gurbir Grewal, director of division of enforcement, SEC

The US Securities and Exchange Commission (SEC) is showing no sign of slowing down its crackdown on record-keeping failures, coming down on 12 firms over electronic communication recordkeeping failures.

The dozen firms, made up of broker-dealers, investment advisors, and one dually-registered broker-dealer and investment adviser, violated recordkeeping provisions under federal securities laws, and have agreed to pay a total of US$88,225,000. The firms were each charged with violating certain recordkeeping provisions of the Securities Exchange Act or the Investment Advisers Act or both. One firm was spared a penalty due to its own investigation and cooperation with the SEC.

The firms are: Stifel, Nicolaus & Company ($35m); Invesco Distributors, together with Invesco Advisers ($35m); CIBC World Markets, together with CIBC Private Wealth Advisors ($12m); Glazer Capital ($2m); Intesa Sanpaolo IMI Securities ($1.5m); Canaccord Genuity ($1.25m); Regions Securities ($750,000); Alpaca Securities ($400,000); Focused Wealth Management ($325,000); and Qatalyst Partners (no penalty). The SEC’s investigations into all the firms except for Qatalyst uncovered pervasive and longstanding use of unapproved communication methods, known as off-channel communications. The failures involved personnel at multiple levels of authority, including supervisors and senior managers.

In April, Senvest Management, a privately owned hedge fund sponsor which invests in US public equity markets, was hit with a US$6.5 million penalty for its use of off-channel communications. In August, more than two dozen firms were hit with fines by the SEC and the Commodity Futures Trading Commission (CFTC) over recordkeeping and communications violations.

Gurbir Grewal, director of division of enforcement, SEC

Gurbir Grewal, director of the SEC’s division of enforcement, said: “Widespread and longstanding failures, including where those failures potentially hinder the Commission’s investor protection function by compromising a firm’s response to SEC subpoenas, may result in robust civil penalties.

“On the other hand, firms that self-report and otherwise cooperate with the SEC’s investigations may receive significantly reduced penalties. Here, despite recordkeeping failures that involved communications by senior leadership and persisted after our first recordkeeping matters were announced in 2021, Qatalyst took substantial steps to comply, self-reported, and remediated and, therefore, received a no-penalty resolution.”

Qatalyst will not pay a penalty because it self-reported its recordkeeping violations, cooperated with the staff’s investigation, and demonstrated substantial efforts at compliance with the recordkeeping requirements. Two additional firms, Canaccord and Regions, also self-reported their violations and, as a result, will pay significantly lower civil penalties than they would have otherwise.

Separately, the Commodity Futures Trading Commission announced a settlement with Canadian Imperial Bank of Commerce for related conduct.

Nasdaq and Deutsche Börse are co-operating with an unannounced European Commission antitrust inspection into financial derivatives products.

The Commission is concerned the firms may have violated EU antitrust rules that prohibit restrictive business practices.

German stock exchange firm Deutsche Börse, of which derivatives exchange Eurex is a subsidiary, confirmed the European Commission’s investigation and told GT: “We do not comment on ongoing investigations.”

Nasdaq told GT: “We are aware of an investigation initiated by the European Commission involving the derivatives market. Nasdaq is committed to fully cooperate with the European Commission and support the relevant authorities with the investigation.”

The European Commission announced on Monday the inspections in two EU member states, with the relevant national competition authorities in attendance. The Commission told GT it would not confirm in which countries it was conducting the investigation nor the companies involved.

These probes are preliminary; if they uncover anti-competitive practices, further investigations and fines are a possibility.

When it comes to European derivatives exchanges, Eurex continues to dominate with a 71% market share in August 2024, and its equity derivatives volume standing at €80 billion, 31% higher than the same period last year (€61bn).

Eurex’s Equity Index Derivatives encompasses EURO STOXX 50, STOXX Europe 600, MSCI Indices, DAX, SMI, and FTSE 100, while Euronext covers regional exchange products.

Meaghan Dugan has left her role as head of options at NYSE, the company has confirmed.

Dugan has been head of options since August 2022, before which she was a senior director at ICE. With more than two decades of industry experience, she previously spent more than 10 years as a director at Merrill Lynch and as vice president of electronic trading at Morgan Stanley.

NYSE declined to comment on the change. Dugan could not be reached for comment.

Last week’s move by the Securities and Exchange Commission (SEC) to reduce the minimum tick size of many national market system (NMS) stocks to half a cent marks a significant milestone for the US equity market.

Alongside the tick price reduction, the SEC voted to reduce the access fee caps for protected quotations of trading centres, increase exchange fee and rebate transparency and accelerate the implementation of rules obliging exchange to provide timely information and certainty of fees and rebates at the time of execution.

As such, this week’s announcement has been something of a double-edged sword for exchanges. On the one hand, changes to minimum pricing increments could help to draw traders back to executing on exchange. On the other, reductions to access fee caps – 0.1% of the quotation price per share for stocks under US$1, down from the current 0.3% level – could put a dent in their earnings.

However, estimating such impacts is not straightforward. Nasdaq’s cash equities business saw US$703 million in trading revenue in the first half of 2024, which drops to just US$212 million after deducting expenses, rebates and fees. At ICE, which owns NYSE, cash equities trading revenue net of transaction-based expenses was US$151 million in H124. By comparing this to equity options revenues, Global Trading estimates that ICE made US$935 million gross revenue from cash equities over the first six months of the year.

While observers agree that exchange revenues will be negatively affected, people familiar with the exchanges caution against applying the two-thirds reduction in fee cap directly to their disclosed numbers. Only part of the cash equity revenues is covered by the fee cap, and this is not disclosed by the exchanges. Moreover, opacity in the way the exchanges allocate rebates to liquidity providers means that changes to the fee cap might not feed into revenue changes in a straightforward way.

While both ICE and Nasdaq declined to comment on the impact that the change would have on their profits, Nasdaq was scathing about the overall impact on the market: “The latest rules will impose serious harm to the long-term strength of the U.S. equity market, weaken the NBBO (National Best Bid and Offer), and ultimately increase costs for investors and listed companies”, a spokesperson told Global Trading.

Why now?

Commenting on the proposals, SEC Commissioner Caroline Crenshaw explained the rationale behind the change. “Currently, many exchanges charge the maximum fee and then pay out nearly all of it as a rebate to compensate liquidity providers. Though the

Caroline Crenshaw, commissioner, SEC

exchanges retain a small amount for themselves, this practice distorts the price that is actually available to investors. Therefore today’s amendment, which reduces the access fee, will allow exchanges to retain that same net capture for executions they were already keeping and continue to use rebates.”

That said, this is an experimental approach; “Reducing the distortions in the market associated with the fee/rebate models that have developed under the higher access fee cap should help improve market quality and preserve the integrity of displayed prices, which will reduce costs for investors,” Crenshaw said. However, she added, “It remains to be seen whether it will be helpful enough”.

The amendment to tick sizes has been long-awaited. Rule 612 of Regulation NMS, adopted by the SEC in 2005 “to modernise and strengthen the national market system for equity securities”, stated that the tick size NMS stock with a quotation, order or indication of interest priced at US$1 or above cannot go below US$0.01. Stock priced below this threshold were given a minimum pricing increment of US$0.0001.

A changing world

Since rule 612 was introduced, now almost two decades ago, “there has been a marked increase in trading volume related to NMS stocks that are constrained by the minimum pricing increment under the rule”, the SEC said on Wednesday. Tick-constrained stocks, with a time weighted average quoted spread of US$0.011 or less, make up the majority of the current trading volume, the commission reported in its proposal, and are unable to be priced by market forces. This causes the artificial constraint of their pricing, it continued, due to large quoted spreads.

Stocks become tick-constrained when their price is a low dollar amount (like Intel), in which case the tick size will end up being the spread of that stock as well. That increases trading costs for tick-constrained stocks, particularly for those who trade them frequently, and has led many traders to execute their trades off-exchange, on venues subject to less strict regulation. As much as two thirds of volume for large-cap stocks like Nvidia, for example, are executed on Finra’s Alternative Display Facility.

As commissioner Mark Uyeda explained, “if a tick size is too large, it can discourage price

Mark Uyeda, commissioner, SEC

competition on national securities exchanges and cause market participants to seek out other venues that might lower transaction costs.”

“The market structure and technology available today is vastly different from what was available when Regulation NMS was adopted”, the rule-change proposal said, drawing attention to the rise of electronic trading and the speed at which it can handle and process information. In light of this, “investors should have access to the best priced quotations available in the national market system and such prices generally should be determined by competitive market forces”.

Commissioner Crenshaw, in a statement on the amended rules, said: “Data analysis has shown that it would be easier and less costly for investors to transact in these stocks if they were allowed to quote at increments smaller than one penny.”

Through the revisions the SEC hopes to ensure that orders placed in the national market system reflect the best prices available, reducing transaction costs and improving overall market quality.

Thorsten Ackermann, head of APAC cash equities trading, JP Morgan

JP Morgan has appointed Thorsten Ackermann as head of APAC cash equities trading. He is based in Hong Kong.

Ackermann has more than 20 years of industry experience and joins JP Morgan from Jefferies, where was senior vice president and an equity trader in London. Prior to this, he was a director at Macquarie Group in and Citigroup Global Capital Markets.

His career has been split between London and Hong Kong, with a focus on European and

Thorsten Ackermann, head of APAC cash equities trading, JP Morgan

Asian equities markets.

Ackermann announced the move via a LinkedIn update. Jefferies declined to comment on Ackermann’s departure, or on who could be replacing him. JP Morgan could not be reached for comment.

Reeling from a money laundering scandal and record-keeping fines, TD Bank has named an internal candidate Raymond Chun as its new CEO as it battles to change its culture.

Many expected a change in TD management after numerous issues with regulators over recent months.

Earlier in the year, TD was the subject of a US Department of Justice probe investigating how Chinese criminal groups were using the bank to launder profits from fentanyl sales. It emerged that TD employees, along with those at other banks involved in the laundering, were bribed with US$57,000 in financial incentives over the course of five years.

In anticipation of regulatory fines, TD set US$2.6 billion aside – a figure partially offset by the sale of 40,500,000 shares of common stock from its stake in The Charles Schwab Corporation. In August, these preparations resulted in the bank’s first loss in more than 20 years.

At the time, CEO Bharat Masrani assured that ”We recognise the seriousness of our US AML

Bharat Masrani, group president and CEO, TD Bank Group

program deficiencies and the work required to meet our obligations and responsibilities is of paramount importance to me, our senior leaders, and our boards. Our remediation program is well underway.”

In August, TD was fined US$30 million by the SEC and US$75 million by the CFTC over recordkeeping violations. It was fined a further US$4 million by the CFTC over failures to effectively monitor communications. Along with 25 other firms caught up in the commissions’ penalties sweep, the bank agreed to pay the fines.

In a 21 August update, TD stated that it expected to see a global resolution, including monetary and non-monetary penalties, to be finalised before the end of the year. As part of its improvement efforts, and amid questions of its internal culture and excessive bureaucracy, Masrani stated that TD had “[added] globally recognised leaders and talent from across the industry, including experts from regulatory agencies, law enforcement and government” to its AML team. “The bank is also making important investments in data and technology, training, and process design,” he added.

Chun, currently group head of Canadian personal banking, will join the board of directors and become chief operating officer from 1 November. Reporting to Masrani, he will be responsible for all TD’s business lines. At the annual meeting of shareholders on 10 April, he will be appointed as CEO.

Masrani will step down on 10 April 2025, and remain at the bank in an advisory capacity until 31 October 2025.

On his departure from the firm, Masrani stated that “the anti-money laundering challenges we face took place on my watch as CEO and I take full responsibility” and stated that he would continue to direct remediation processes before stepping down, after almost 40 years with the bank, and following a decade’s tenure as CEO.

Raymond Chun, incoming CEO, TD Bank

Chun, who has spent more than three decades with TD, began his career in the management training programme and rising the ranks by way of president of TD direct investing, president and CEO of TD insurance and group head of wealth management and insurance.

Alan MacGibbon, chair of the board of directors, affirmed that “[Raymond’s] proven ability to drive change, deliver outcomes, and build strong, high-performing teams will serve him well as he guides TD into the future.”

Sona Meta, currently executive vice president for real estate secured lending and everyday banking, saving and investing, will take on Chun’s role as head of Canadian personal banking. Further reshuffling in the senior executive team has seen Paul Clark appointed senior executive vice president for wealth management, and Tim Wiggan named as group head of wholesale banking and president and CEO of TD Securities.

Large language models such as ChatGPT have become a global sensation since demonstrating an ability to conduct convincing conversations, pass exams and produce text. Meanwhile, the European Commission is consulting on new AI regulations. But how useful are these AI systems for traders?

Four researchers – Han Ding, Junhao Wang and Yinheng Li at Columbia University and Hang Chen of New York University – explore this question in a review paper published on the Arxiv Trading & Market Microstructure forum, where they examine 27 papers on LLM-based trading. In addition to their academic affiliations, Ding works as a data scientist for Amazon, Wang for Curemetrix LLC, Li is a scientist at Microsoft and Chen is an engineer at Snap Inc.

Yinheng Li, Microsoft

According to the authors, LLMs can be deployed as trading agents, directly generating and executing trading decisions, or as ‘alpha miners’, proposing and testing investment ideas which can be later implemented by humans. Backtesting shows average trading performance of 15-30% over benchmarks, although this is not the same as a real-world test.

The simplest type are ‘news-driven’ LLMs, which are fed corporate and macroeconomic news updates in order to directly predict stock price movements, similar to earlier-generation machine learning AIs. Then there are ‘reflection-driven’ LLMs, where news feeds and trading outcomes are summarised as memories than can be drawn upon when new information arrives, mimicking the human ability to reflect upon experience.

Debate-driven LLMs consist of multiple agents, each with a differing personality, that debate each other about investing strategies, which the research shows improves their trading performance. Reinforcement learning-driven LLMs are shown historical outcomes from financial markets to refine their predictions.

Hang Chen, Snap Inc.

The alpha-mining LLMs start with a ChatGPT-style conversation, where a trader prompts the LLM to generate a trading idea in the form of a script. Then another LLM is brought in as a judge providing feedback to refine the script, in the form of code which is tested in the real world, with the feedback used to improve both agents.

As regards the choice of LLM, OpenAI is the platform of choice in the studies surveyed by the authors. Data is a challenge, though, because LLMs are (as their name suggests) designed to handle text inputs rather than numerical stock price data. This works fine for financial reports such as 10-Q filings or analyst research. But for stock price histories, the only way forward is to convert numbers into text strings, which the LLMs process like a conversation.

The EU Commission’s July consultation paper has a section on securities markets that could cover a number of situations using LLM-based trading algorithms. Referring to generative AI as ‘general purpose AI’, the Commission asks industry respondents whether systems that act similarly could lead to herding effects, or whether trading algorithms could collude to manipulate markets and squeeze liquidity.

The fact that OpenAI’s platform dominates current LLM trading efforts, suggests that herding should be a concern, given that the trading agents ultimately derive their insights from the same corpus of OpenAI training data. And one can imagine debate-driven LLMs – if not properly supervised – privately agreeing to breach securities laws in order to boost profits.

In a question about ‘robo-advice’ the Commission frets about LLM hallucinations harming consumers. Having read Ding, Li, Wang and Chen’s review paper, it’s an amusing pastime to think about the market scenarios that could result if LLM trading agents become widely adopted.

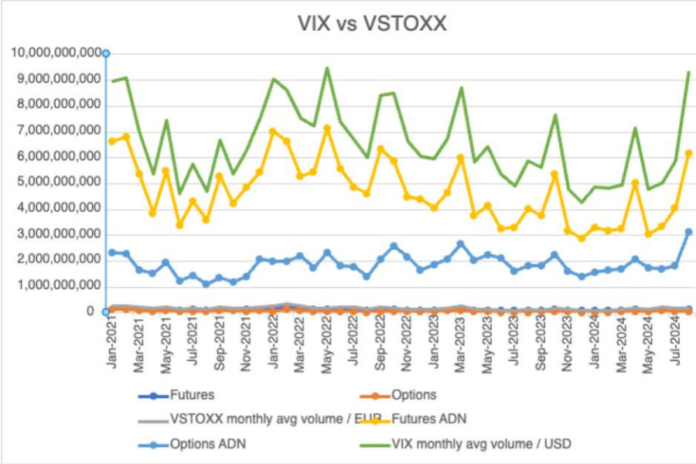

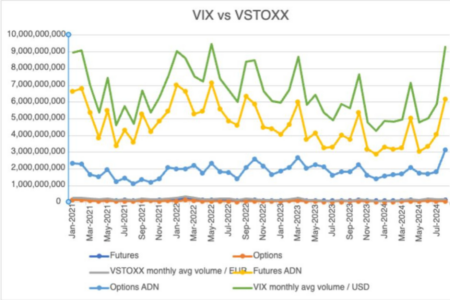

Cboe’s volatility products saw a strong month in August, analysis from Global Trading has found, with VIX options notional volume hitting record highs and dwarfing competitor Eurex’s VSTOXX offerings. The exchangeplans to launch S&P 500 Variance Futures next week, and options on VIX futures in October.

Analysis from Global Trading has revealed that VIX options average monthly notional volumes reached a more than three-year high of US$3.1 billion in August, up more than 70% from fairly static May, June and July figures (US$1.7-1.8 billion). VIX futures volumes, while not setting records, also spiked in August – to US$6.1 billion, building on slow growth since May.

Cboe has maintained a significant majority of market share in this space, dwarfing Eurex’s VSTOXX futures and options performances. Although the European exchange also recorded an increase in activity in August, the VSTOXX monthly average was up a more modest 18% over the month. Futures volumes reached €133 million, while options ADNV dropped – as it did the month before.

In light of increased client interest in volatility products, Cboe is set to launch S&P 500 Variance futures on Monday 23 September. Developed to compete with variance swaps, a long-established over-the-counter derivatives product offered by sell-side banks, the exchange-traded solution will give market participants another way to trade volatility in the US equities market, Cboe said.

S&P 500 Variance Futures allow users to trade the spread between implied and realised volatility in a more streamlined way and take advantage of the difference between market expectations and actual outcomes.

On the product expansion, Rob Hocking, head of product innovation at Cboe, said: “The launch of Cboe S&P 500 Variance Futures comes at a crucial time when risk management is top of mind for many market participants, amid the backdrop of the upcoming U.S. election, shifting monetary policy and ongoing geopolitical tensions.”

Catherine Clay, head of global derivatives at Cboe, commented: “As investor needs for hedging, trading, diversification and asset allocation continue to evolve, we are committed to expanding our offerings to meet their demands.”

Uncertain macro conditions have put volatility front and centre over recent months, most notably during the 5 August market tumble. At the time, the VIX hit 65 and set a four-year record when it closed at 38.57, with the spike in the so-called ‘fear index’ fueling panic about recession and a global crash. A rapid return to more normal levels reassured market participants, but the incident acted as a stark reminder of the current climate’s unpredictability and prompted greater interest in volatility products.

Hocking added: “As demand for hedging and income generation rises, our goal is to broaden access to the derivatives markets by simplifying complex, capital-intensive strategies and making them more easily tradable in an exchange-listed, centrally cleared environment. For those looking to hedge against or capitalise on volatility moves, we believe this new product will offer an accessible and capital-efficient way to replicate the exposures of OTC variance swaps.”

Contracts will settle based on a calculation of the S&P 500’s annualised realised variance. This will be calculated daily, based on a series of values in the S&P 500 Index from the closing index value on the day a VA futures contract is listed for trading to the special opening quotation on the contract’s final settlement date.

Barclays has made a number of appointments within its investment banking division. By shoring up its investment banking business, the firm may be looking to boost its revenues in this area after its relative position in the global rankings remained the same as last year.

The bank’s global investment banking revenues, year-to-date, stood at US$2 billion, placing it sixth, the same as last year’s Dealogic rankings.

The firm’s global equity capital market year to date revenues stood at US$278 million, placing it 7th in Dealogic rankings, up from 12th in the same period last year. Barclays did not make it into the top ten M&A rankings this year to date.

McNulty, Davidson, Itkowitz

The firm has appointed Derek McNulty as global co-head of chemicals, Derek Davidson as head of Americas commercial, residential and industrials services, Jared Itkowitz as head of Americas transportation and logistics, all within industrials investment banking. They will report to Spyros Svoronos, global head of industrials investment banking.

A fourth, Abhishek Singhal, has been named managing director within technology investment banking, focused on the payments sector. Singhal will report to Kristin Roth DeClark, global head of technology investment banking.

All four will be based out of New York.

Singhal

Singhal joins Barclays from Citigroup where he was a managing director in the fintech investment banking division. Prior to joining Citigroup in 2018, he worked at Deutsche Bank on the TMT investment banking team.

McNulty joins Barclays from Citigroup, where he was head of North America chemicals. He joined Citigroup in July 2022, having previously been a managing director at Jefferies in New York since the beginning of 2019. From 2006 to 2019, McNulty was with Barclays, covering strategic and financial sponsor backed chemical companies, and at the time of his departure was the head of Americas chemicals.

Throughout his career, he has executed more than US$75 billion in strategic advisory mandates as well as equity and debt transactions for blue chip clients.

McNulty will work in partnership with Gabriel Gruber, global co-head of chemicals investment banking.

Davidson will join Barclays from Morgan Stanley, where he was a managing director based in New York leading coverage of companies providing commercial, residential and professional services.

Davidson joined Morgan Stanley in 2010, spending his first 11 years with the firm in the global services group and the last three years as part of the global industrials group. During his time at Morgan Stanley, he executed transactions for clients including Rollins, Iron Mountain, Allied Universal, and BGIS.

Itkowitz has been with Barclays for more than 15 years, and began his career in equity linked and hybrid solutions working in both New York and Hong Kong.

In 2014, he relocated back to New York and joined the industrials group where he has spent the past decade covering transportation and automotive clients on a range of strategic and capital raising assignments.

Spyros Svoronos, global head of industrials investment banking, said: “These appointments demonstrate our continued investment in our platform as we work to most effectively serve our clients with best-in-class strategic advice and execution.”

The appointments are part of a hiring spree at the bank, hiring Rob Patterson to lead data and information platforms coverage earlier this week.

San Francisco-based David King was appointed global head of technology M&A earlier this month. He reports to Kristin Roth DeClark, global head of technology investment banking.

European exchanges are battling to snap up data and benchmark providers as they struggle for dominance amid the region’s fragmented equity markets. The latest example is Euronext’s acquisition of Substantive Research, a firm which provides research and market data benchmarking to more than 100 clients across Europe and North America.

Details of the transaction were not disclosed but the acquisition was fully financed with existing cash.

Euronext said the acquisition will complement Commcise, an acquisition made in 2018, which offers cloud-based, commission management, research valuation, consumption tracking and payment solutions.

Following the integration of Substantive Research, Commcise clients will be able to gain access to unique market benchmarks within the application. Euronext said Substantive Research customers will benefit from Euronext and Commcise’s scale, which will help Substantive Research to increase the number of benchmarked vendors, and also expand the variety of benchmarking products that it can offer to the buy- and sell-side.

The Substantive Research deal follows acquisitions of 75% of Global Rate Set Systems in June this year, and 100% of Allfunds Group in March this year.

Competitor Deutsche Börse made investments in HQLAx, Digital Vault Services and Caplight over the same period. HQLAx was an increase of its longstanding stake in the company (first investment was in 2018, the most recent in April). SimCorp was acquired outright in April 2023.

Camille Beudin

Camille Beudin, head of diversified services of Euronext, said: “The acquisition of Substantive Research will accelerate the growth of our Investor Services business with leading research and market data benchmarking capabilities and cross-selling potential with Commcise, our commission management and research valuation solutions.”

Mike Carrodus, founder and CEO of Substantive Research, said: “With the research market poised for yet more regulatory-driven changes, plus market data consumers grappling with increasing costs and pricing opacity, we are so excited to be able to accelerate our coverage and data depth with Commcise and Euronext’s insight and resources.”

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] Please review our updated Terms & Conditions and Privacy Policy carefully. By continuing to use our services after Aug 25, 2025, you agree to these