Poor data quality poses a critical or significant challenge to transaction cost analysis (TCA) processes for more than three quarters (77%) of derivatives-focused executives at asset management firms, according to a recent report from Acuiti; but equities are broadly untouched by the issue.

This will not come as a surprise to many. “TCA is most mature and widely used in equities, where data availability and standardisation are the most advanced,” the study, The Growing Sophistication of Transaction Cost Analysis’, affirmed. Participant responses confirmed this, stating that equities are the easiest asset class to evaluate TCA in; the most difficult, they said, are OTC fixed income derivatives, spot fixed income and equity derivatives.

Changing regulatory requirements around best execution, technological developments and a widening range of use cases have prompted many asset managers to use the tool in asset classes beyond equities, Acuiti found – most commonly fixed income and equity derivatives, although participants also apply the strategy to commodities and listed and OTC fixed income derivatives.

The issue of poor data quality is most acute among those measuring TCA in OTC derivatives, the report noted, while those who only deployed TCA for equities were far more likely to rate it as providing no, or a slight, challenge.

“Fixed income analysis is more complex due to the diversity of instruments and the absence of a centralised marketplace,” the report explained. “In addition, measuring TCA in less liquid markets can be challenging.”

OTC markets pose difficulties due to their opacity, it continued, with less inputs to measure performance against. Additionally, the customisable nature of swaps contracts and the popularity of privately negotiated deals with limited competition make it difficult to compare execution quality and pricing.

Fragmented data analysis contributed to the problem of poor data quality, Acuiti said, observing that just half of the firms participating in the study used a single, golden source of data for processes including TCA and risk and portfolio modelling.

“As firms look to integrate TCA processes in other areas of the business, fragmented data across the organisation will set back drives for efficiency,” the company warned.

In addition to poor data quality, the study found that more than 70% of participants found sourcing accurate data to be a critical or significant challenge when conducting TCA. Measuring liquidity was the second most challenging issue cited, while allocating fixed internal costs was the most popular choice marked as ‘no challenge’ or ‘slight challenge’.

Bringing together different data sets was a significantly less challenging process than sourcing the data itself, with no participants labelling this as a significant challenge and the majority calling it a slight challenge. More than 20% stated that it was no challenge at all when conducting TCA.

Looking ahead, Acuiti predicted that firms will lean into outsourcing TCA processes. “As the sophistication of TCA increases, so too does the cost of development,” it said. “Firms that are deploying TCA pre-trade and looking for real-time TCA will ultimately be better served mutualising the costs of developing that software with a third-party vendor.”

Mark Randall, director of information services, JSE

The Johannesburg Stock Exchange (JSE) is the latest to unveil a new data service as it works to keep up with incumbent exchanges and industry trends, completing the first phase of its market data modernisation strategy and creating a centralised, cloud-based marketplace for its data products and services in partnership with DataBP.

Data continues to be a key profit generator for exchanges, with recent estimates from Morgan Stanley Research suggesting that data and analytics makes up two-thirds of LSEG’s overall revenue. In contrast, post trade and fixed income account for just 14% and 15%, respectively.

While not quite to the same degree, the value of data is also clear at Deutsche Borse and Euronext. Morgan Stanley Research estimates that the exchanges receive 23% and 22% of revenue from their data and analytics offerings.

“Exchanges the world over are looking to their data businesses to bolster their revenue as pressure on trading revenue continues,” Mark Randall, director of information services at the JSE, told Global Trading. “There are tier one exchanges that have data shops. This platform enables us to give JSE clients a world class client experience that they are accustomed to from other global exchanges, which is a big step for us on the tip of Africa.”

The JSE’s information services division contributed 15.5% to JSE group revenue, according to 2023 year-end financial statements.

Using DataBP’s financial data management platform, the JSE will be able to simplify client onboarding, streamline product development and automate data access entitlements and billing processes, it said. Clients will benefit from access to a wide range of products and the ability to enhance JSE data – both real-time and historical – through third-party content and analytics services.

Randall commented: “Migrating data offerings to the cloud is a key part of JSE’s ICT strategy. It not only reduces infrastructure costs but also increases flexibility.”

Mark Schaedel, CEO of DataBP, told Global Trading that exchanges’ interest in building out their data services should not come as a surprise. “I think exchanges are essentially price formation platforms, and that price is used not just by those who interact from that platform, but many others. So to me it seems like a natural evolution for exchanges to become data providers first, and for their businesses to become data-centric,” he said.

“Exchanges have recognised that their data is a valuable asset and product, that even those who don’t trade on their platform benefit from it, and that there will be demand for it to inform other types of events, valuation of assets, routing decisions, trading decisions, and to navigate capital markets.”

The JSE has previously partnered with big xyt to develop Trade Explorer, which allows trading venues to distribute data analytics solutions to clients in their ecosystems. This service, delivered by big xyt, has now been made available on the new platform along with digitised client contracting for index agreements.

Looking ahead, the exchange plans to release a virtual storefront where clients can purchase data online. “Ultimately, the JSE aims to leverage cloud services to provide clients with analytics and insights, rather than just raw data,” Randall said.

The six biggest Wall Street banks have accumulated vast equity cash and derivative portfolios. Using Federal Reserve filings, we reveal their portfolio size, hedging strategies and risk exposures – but now a proposed regulatory change might throw all this on its head. Nick Dunbar reports.

In cash equity trading they may have lost their lead as liquidity providers to the likes of Citadel Securities and Jane Street, but the Wall Street banks still play a central role on the sell-side. Regulated by the Fed, they can deploy leverage and act as principals, taking strategic equity exposure shunned by quant trading firms.

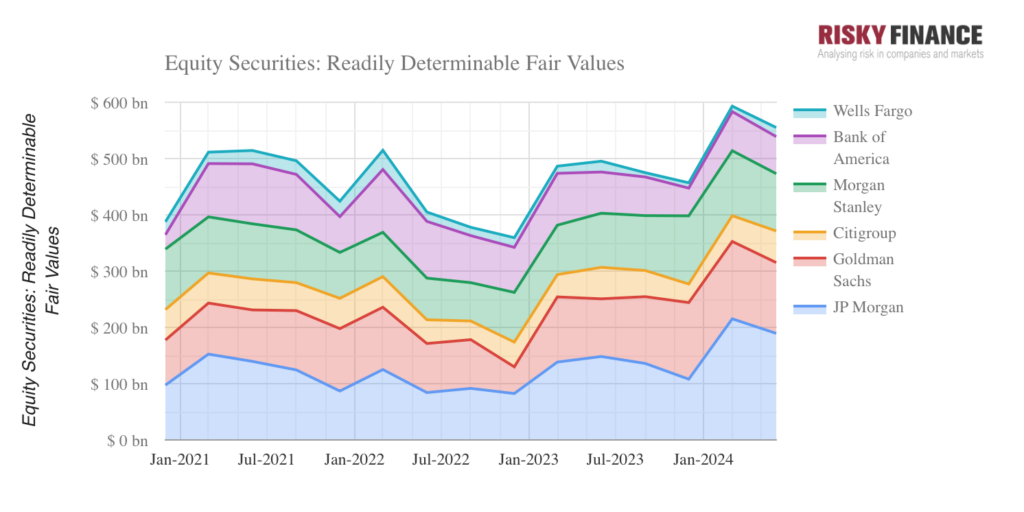

As markets have risen, so has the value of these equity exposures, reported quarterly in Fed filings. In the first quarter of 2024, equity holdings reached US$600 billion, led by JP Morgan with US$215bn and Goldman Sachs with US$137bn followed by Morgan Stanley, Bank of America, Citigroup and Wells Fargo.

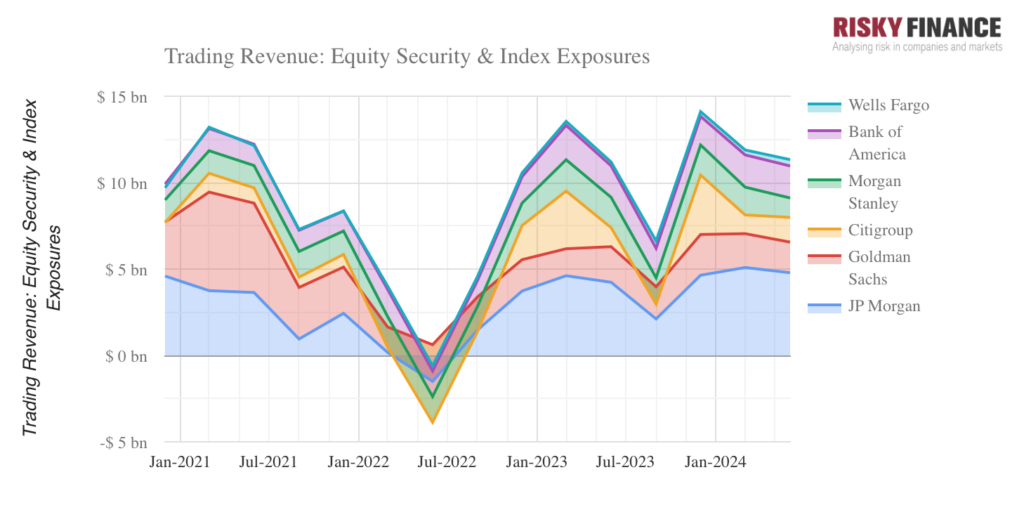

These equity holdings generate substantial trading revenue, totalling around US$11bn for the six banks in the second quarter of 2024, according to the filings. JP Morgan is in the lead here too, with US$4.8bn equity trading revenues in Q2, followed by Bank of America with US$1.8bn. Using the Federal Reserve data, we can see that these trading revenues are volatile, much more so than the banks’ published quarterly results.

For example, in Q2 2022, Citigroup suffered an equity trading loss of US$4.5bn according to the Fed’s data. But not in the bank’s quarterly earnings and 10-Q filings, in which Citi reported positive equity markets revenues of US$1.2bn in the same quarter. Clearly something is missing and the answer is derivatives.

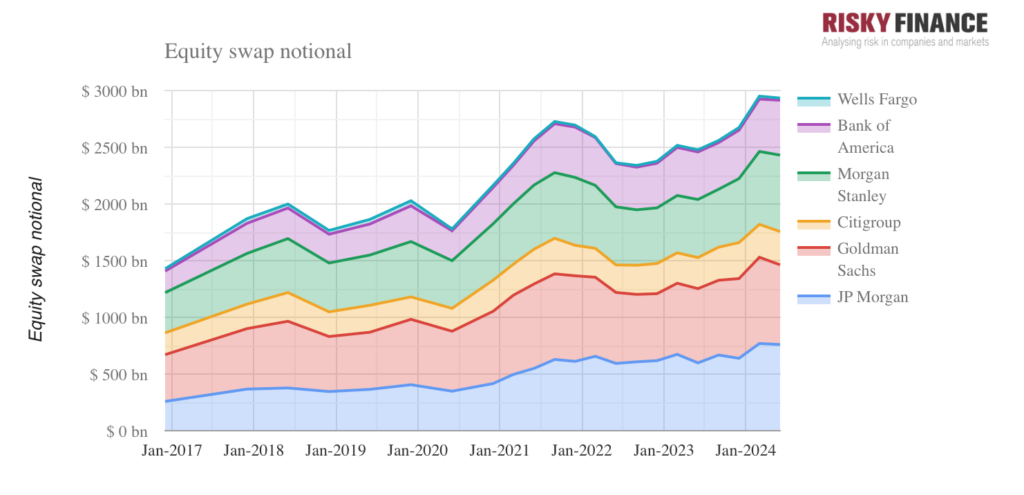

Equity derivative positions dwarf the cash equity positions of the banks in notional terms, although contracts such as index futures and options are not really comparable because notionals do not reflect their market value.

As opposed to options or futures, equity swaps are more comparable because they most closely replicate a physical stock holding, and hedge funds use them for this purpose. But there is a catch. The contracts are symmetrical – a counterparty on one side is effectively long the stock, but the on the other side the counterparty is short.

In the Fed filings, long and short equity swap positions are lumped together. JP Morgan reported US$759 bn of equity swaps in Q2, and Goldman had US$702bn. But we do not know how much of this was long exposure that can be added to the bank’s physical stock holdings.

We can try and unpick how much money the banks make on these derivatives by looking at two more lines in the Fed disclosures – ‘positive fair value of equity derivatives’ (where a bank is owed money on the contracts) and ‘negative fair value of equity derivatives’ (where the bank owes money) The change in these numbers from one quarter to the next would tell us something about a bank’s derivative profit and loss, if the contracts were fixed in place.

In reality, these contracts are changing all the time, as old ones expire and new derivatives are added, making a P&L estimate impossible. In the case of Goldman, both positive and negative-valued equity derivatives have increased over the past two years, but negative-valued derivatives have increased the most, suggesting that the bank has added short positions to hedge against rising equity markets.

Value-at-risk

To get a better idea of the actual risks the banks are taking with these trading portfolios, we need to look at a different area of Federal Reserve disclosures – the market risk filings. These follow an approach that started in the 1990s, looking at the statistical nature of trading books – an approach which is now widely used among both sell-side and buy-side firms.

Rather than take a snapshot of portfolio size or trading P&L on a particular date, banks assess the distribution of daily P&L during a specified time window (such as 100 days), sorting them from worst to best. The dividing line between the worst day and the other 99 less-bad days is called the value-at-risk or 99% VaR.

In the Fed’s market risk filings, the banks report VaR for individual asset categories such as equities or interest rates, and for the trading book as a whole. Rather than for a 1-day loss, these VaRs are for 10 days, so the numbers have to be divided by the square root of ten to convert them into a daily VaR. Then the regulators ask them to report backtesting results – the number of days that trading losses exceeded the VaR estimate. There are 63 trading days per quarter, so these 1-in-100 day events should happen once every two quarters or so.

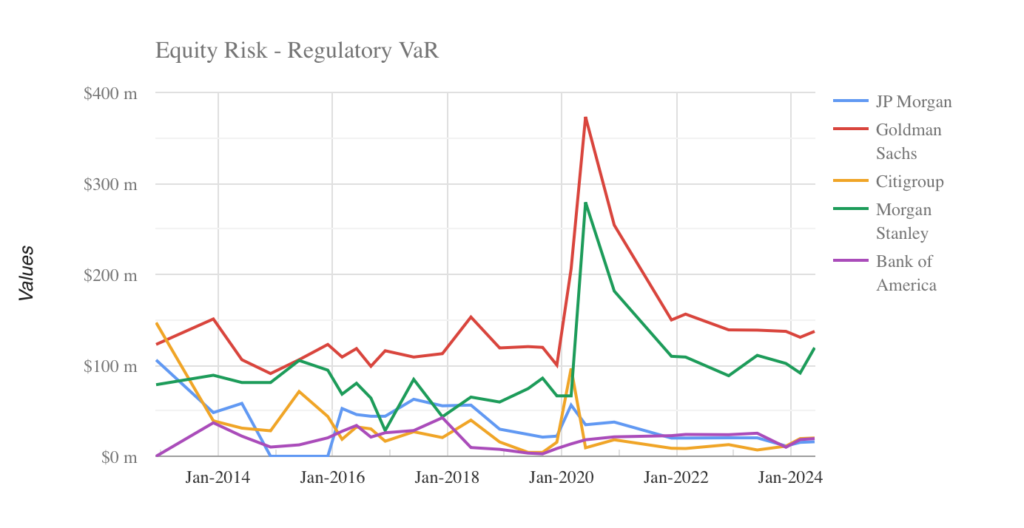

It is in the VaR and backtest numbers that the personalities of the banks reveal themselves. So, while JP Morgan may have the largest equity trading portfolio, Goldman has the largest equity VaR of US$137m in Q2 2024, followed by Morgan Stanley – reflecting both banks’ leading roles as market makers and capital markets specialists. That requires them to take outsized positions (such as for M&A deals or block trades) that expose them to greater risk.

This also reflects their ability to hedge. Index hedges are most liquid, but are the least effective at hedging the risk of a stock like Nvidia. An outright short would be the best hedge for a single stock, but is either impossible e.g. for an initial public offering (IPO), or would undermine the business model of the investment banks which requires them to hold a clients’ stock with minimal market impact. Citigroup, with an equity VaR of just US$20m, is clearly not trying to play this game.

The backtest data shows not just the number of days per quarter that the banks’ daily losses exceeded their VaR, but also how much greater than VaR these losses were. So the last time that Goldman reported a VaR exception, in Q1 2023, we learn that this loss was 215% of its VaR on that day (the Fed does not tell us whether this loss was in equity trading or another asset class). Using Goldman’s average VaR of US$484m for that quarter as a proxy, that suggests a loss of US$330m (dividing by the square root of ten to convert the 10-day VaR to daily VaR). Morgan Stanley lost US$217m on one day in the same quarter, using a similar analysis.

Although the banks may recoup these losses on other trading days, delivering profits for shareholders, VaR has a direct impact on them, via the Basel capital rules for market risk. Including a VaR-based capital requirement works as an incentive to reduce VaR, in order to reduce capital and increase dividends and share buybacks.

A year ago, the Fed threw all this into play with its Basel Endgame proposals – so-called because these were supposed to be the final US version of Basel III bank capital rules. The Fed wanted to abolish VaR for regulatory purposes, because of a well-known problem with VaR: It only measures the dividing line between the worst day and the less-bad days, not the amount you actually could lose on the worst day.

An example of this problem can be seen in Citigroup’s results for Q4 2023, when it reported a backtest exception. According to Fed filings, the actual loss on that day was eight times the bank’s VaR number, which averaged US$285m, implying a 1-day loss of US$720m. Such an extreme outcome would worry regulators. To plug this gap, the Basel Endgame would replace VaR with the expected loss on the worst day – which would force the banks to allocate a lot more shareholder capital to trading portfolios.

Over the past 12 months, banks and industry groups have lobbied hard against the endgame, even paying for advertising spots in the American Superbowl football tournament. The Fed promised to soften the proposals, and on 10 September, Fed vice-chairman Michael Barr confirmed that the credit and operational risk components of the Endgame would be dramatically scaled back – but not the market risk component. Traders and risk managers everywhere should take note.

Vincent Hall has joined Citi as an equity trader, after a two-year tenure at Citadel.

Hall has close to a decade’s industry experience, and began his career as an analyst at Citi’s markets and securities service. He later became an emerging markets equity trading analyst, before being appointed assistant vice president of the division.

He joined BlackRock as an associate in 2020, moving to Citadel in 2022.

In our latest regulatory round-up, we see firms urged to strengthen their ‘know your customer’ and anti-money laundering programmes in light of increased regulatory scrutiny, while pan-European regulator ESMA suggests markets remain ‘sensitive’ despite lower volatility earlier this year. In the Americas, US regulator the Commodity Futures Trading Commission has been busy, with fines for Nasdaq Futures and BNY Mellon.

Strengthen KYC, AML firms urged after H124 sees 31% surge in fines

ICMA publishes summary report following its 2024 repo and sustainability survey

Hong Kong exchange launches paperless listing reform consultation

Hong Kong makes temporary modifications to SPAC listing requirements

ESMA: markets remain ‘very sensitive’

CFTC fines Nasdaq Futures over “false and misleading statements”

CFTC hits BNYM with penalty over reporting and supervision failures

World

Strengthen KYC, AML firms urged after H124 sees 31% surge in fines

There was a 31% increase in the value of fines issued in H1 2024 compared to H1 2023, with the Asia-Pacific region (APAC) seeing the steepest rise in penalties, totalling more than US$46 million – a 266% increase compared to H1 2023.

The findings come from Fenergo, which said the rise in the value of fines reflects a global regulatory crackdown and technology advancements, which enhance the accuracy of detecting illicit activity.

Tracy Moore

Tracy Moore, director of regulatory affairs at Fenergo, said: “Looking towards the second half of the year, we expect this trend to continue, necessitating robust preparations for increased year-end enforcement actions.”

ICMA publishes summary report following its 2024 repo and sustainability survey

The International Capital Market Association’s (ICMA) repo and sustainability taskforce has published feedback received in response to its 2024 repo and sustainability market survey, launched in February 2024.

Building on the observations and categorisations from ICMA’s 2022 paper on sustainability in the repo market, the survey was designed to broaden the understanding of existing market practices and identify issues for further reflection and future guidance.

Feedback included calls for more guidance covering all types of sustainability-related repo; a confirmation that the majority of respondents active in this market primarily focus on repo transactions involving sustainable collateral and this category of sustainability-related repo remains their top priority; and a consensus that to avoid double-counting from an accounting perspective, any green claims should remain with the repo seller, who retains the economic exposure to the assets.

APAC

Hong Kong exchange launches paperless listing reform consultation

The Stock Exchange of Hong Kong Limited (the Exchange), a wholly-owned subsidiary of Hong Kong Exchanges and Clearing Limited (HKEX), has published a consultation paper seeking public feedback on proposals to further expand its paperless listing regime and other rule amendments.

The proposals aim to modernise market infrastructure and enhance operational and regulatory efficiency with market feedback sought over a two-month consultation period.

Katherine Ng

HKEX head of listing, Katherine Ng, said: “Sustainability sits at the core of HKEX’s strategic development and we are committed to adopting sustainable best practices as we continue to modernise. Our ongoing paperless listing reforms have been widely welcomed by the market, successfully resulting in a reduced use of paper and, recently, the first electronically registered prospectus in Hong Kong. We are pleased to be introducing more digital and web-based options to our listing framework, such as through electronic money transfer alternatives to cheque payments. Our proposals will not only align our practices with global standards, but will also provide greater convenience and enhanced efficiency for issuers, investors and other market participants.”

Hong Kong makes temporary modifications to SPAC listing requirements

The Securities and Futures Commission (the SFC) and The Stock Exchange of Hong Kong have made temporary modifications to the Listing Rules and amendments to the Exchange’s guidance materials effective from 1 September 2024, with respect to the minimum initial market capitalisation of Specialist Technology Companies; and independent third-party investment requirements for De-SPAC Transactions conducted by special purpose acquisition companies (SPACs).

The modifications, with the SFC’s support, are designed to address the change in market conditions since the introduction of both listing regimes.

Katherine Ng, HKEX’s head of listing, said: “At HKEX, we are committed to continuously reviewing and enhancing our listing framework so that it remains fit for purpose, supporting the attractiveness and competitiveness of Hong Kong’s capital market. Drawing on insights from listing applicants and related transactions, we have identified opportunities to boost the inclusivity and dynamism of our listing environment within the established framework. These modifications will provide greater flexibility and clarity for both issuers and investors, whilst upholding our robust regulatory standards.”

Michael Duignan, SFC’s executive director of corporate finance, said: “The SFC fully supports these modifications to maintain Hong Kong’s edge as a top listing destination for innovative and fast-growing technology companies. It is another example of how the listing authorities can be both agile and responsive to a challenging market environment, whilst continuing to maintain the quality of the market.”

EMEA

ESMA: markets remain ‘very sensitive’

The European Securities and Markets Authority (ESMA) has said markets remain “very sensitive”, despite lower volatility earlier this year.

Markets remain sensitive to interest rate changes, deteriorating credit risk and to political and electoral developments, the regulator said, with a “high risk” of corrections within the context of market liquidity in equities and other markets.

Verena Ross, chair, ESMA

ESMA chair, Verena Ross, said: “Markets are getting more nervous about the economic outlook and political events, as the dip in equity valuations in early August and market volatility around recent European and French elections shows.

“Close monitoring of the financial markets in our remit and strong coordination of supervisory efforts with national authorities remains our priority.

We continue to see risks in the fund area linked to liquidity mis-matches, particularly in the real estate sector, and deteriorating quality of assets linked to interest rate, credit risk and valuation issues.”

Americas

CFTC fines Nasdaq Futures over “false and misleading statements”

Nasdaq Futures has received a US$22 million penalty from the Commodity Futures Trading Commission (CFTC) for failing to sufficiently establish, monitor or enforce rules related to an incentive programme offered to certain debt capital market (DCM) traders.

From July 2015 to July 2018, the CFTC says, Nasdaq Futures offered a range of incentive programmes to certain traders in the contract market while operating as a DCM focused on energy commodity futures contracts.

One such incentive was the Designated Market Maker (DMM) programme, which paid a fixed monthly stipend to market makers and was disclosed both to the CFTC and the public. However, the commission found that certain programme participants were also given payments based on the total number of contracts that they traded, an element that was not disclosed. In rule submissions, Nasdaq Futures either omitted or explicitly denied the existence of these volume-based incentives within the programme, and interviews with staff on the topic garnered equal denials.

Recommendations from Nasdaq Futures’ regulatory service provider to contact three DMM programme participants about particular trading activities were not followed, nor was documentation made of why these actions were not taken.

CFTC hits BNYM with penalty over reporting and supervision failures

The Commodity Futures Trading Commission (CFTC) has issued a US$5 million civil monetary penalty to the Bank of New York Mellon (BNYM) following its failure to report millions of swap transactions to a registered swap data repository.

These actions were in violation in a previous CFTC order against the firm, the commission stated, and demonstrated a failure in the supervision of BNYM’s swap dealer business as required by the Commodity Exchange Act and CFTC regulations.

An order filing and settling charges with BNYM was issued on 26th August. Alongside the penalty, BNYM will retain an independent compliance consultant to review and advise on its compliance programme, it said.

Citi has named Achintya Mangla head of financing for investment banking.

In the newly created role, Mangla will report to head of banking Vis Raghavan and be responsible for global debt capital markets, equity capital markets, syndicate and private capital markets.

Achintya Mangla

Prior to Citi, Mangla spent more than two decades at JP Morgan where he most recently served as head of global equity capital markets. He also held roles across multiple asset classes and has worked in Asia, EMEA and the US.

Commenting on the appointment, Raghavan said: “[Mangla] is a proven leader with a track record of building and leading high-performing teams that deliver innovative, globally minded solutions to clients.”

The current head of global debt capital markets Rich Zogheb and co-heads of global equity capital markets, Douglas Adams and James Fleming, will continue in their respective roles and report to Mangla. Mangla will also work with other parts of Citi, including markets, wealth and risk.

Neurodiversity has been in the spotlight over recent years, with society becoming more aware, accepting and understanding of the needs of others. As a result, many firms now include neurodiversity within their DEI strategies, and even actively promote their neurodiversity initiatives. But when it comes to actually speaking about the topic outside the bounds of press releases and pre-approved statements, Global Trading has discovered an industry-wide reluctance to engage.

Neurodiversity is a sensitive subject. A 2024 study from The Diversity Project found that 57% of those polled, employees within the investment and savings industry, had disclosed their neurodiversity to their employer. It’s not necessarily a low figure, but as co-chair of The Diversity Project’s neurodiversity workstream Tim Edmans points out, “you have to consider the kind of people who are completing the survey. There’s a sample bias here”. In reality, the figure is likely far lower; stigma around neurodiversity remains prevalent.

Among those who disclosed, the majority (two thirds) reported a supportive response from their employer – demonstrative of the progress the industry, and society has made. An additional 10%, however, stated that they received an “unhelpful response” from their employers, and a quarter recalled a neutral response – arguably also unhelpful.

Among those who chose not to disclose their neurodiversity, reasons included concerns that it would limit their job prospects and fears that responses from colleagues would be less than desirable. It’s no surprise, given the fact that 55% of survey participants said that their neurodiversity had caused difficulties around finding work earlier in their careers.

What is neurodiversity?

Neurodiversity is a concept used to understand the different ways that people cognitively process, experience and interact with the world around them. It aims to take a positive approach to the neurological differences between individuals, rather than seeing divergence from the norm as a deficit.

Depending on which figures you follow, between 15 and 30% of the population are estimated to be neurodivergent. This isn’t a fringe issue, and it’s something that affects people, directly or indirectly, more than the majority may assume.

Although generally associated with autism, ADHD and learning difficulties like dyslexia, dyscalculia and dysgraphia, the term ‘neurodiverse’ covers a wide remit and has permeable borders; OCD and bipolar disorder also often fit under the umbrella. In addition to some mental health conditions also being categorised as neurodivergence, neurodiverse individuals are often more likely to deal with conditions such as anxiety and depression, issues likely worsened by a lack of understanding from those around them and the requirement to work in environments that are actively hostile to their needs.

Duncan Higgins

Duncan Higgins, CEO of Sustainable Trading, told Global Trading that early results from the firm’s Workplace Experience Survey have included feedback that employees’ neurodiversity has affected their experience in the trading industry. It’s not that nothing is being done to support neurodiverse individuals in trading, but clearly there’s a long way to go before people are fully comfortable to be their ‘true selves’ in the workplace. And while a majority of firms include neurodiversity in their DEI policies, Vic Mazonas, general manager of the Group for Autism, Insurance, Investment and Neurodiversity (GAIN), points out that, “an individual’s experience of a company comes not from the policies on paper, but how they’re applied”.

Vic Mazonas

Many firms are vocal about their work to be actively neuroinclusive in the workplace, promoting their provisions across websites, social media and conference panels. JP Morgan’s Office for Disability states its intention to “lead strategy and initiatives aimed at driving an inclusive workplace while helping the firm aspire to be a bank of choice for people with disabilities”, and runs the ‘Autism at Work’ programme to support autistic employees across nine countries – although the focus here is on technology-oriented roles rather than the trading floor.

Goldman Sachs made headlines when it launched its Neurodiversity Hiring Initiative in 2019. The programme offers a 10-week paid internship for neurodiverse individuals, developed in partnership with Specialisterne – a non-profit organisation working to integrate neurodiverse people into the workplace. The programme offers training and mentorship, with the goal of preparing participants for long-term careers.

But when contacted directly by Global Trading, these firms and others declined to participate in this article. Although awareness and vocal support is a crucial step in becoming more inclusive, a reluctance to engage in direct discussions about the topic suggests that there is still work to be done.

While firms may frame their neuroinclusivity efforts as successful, Manjinder Mann, a day trader and former proprietary trader, presents a different reality. “Put it this way,” he told Global Trading: “the situation is so bad that I ended up starting a company to end this mess of discrimination and exclusion.”

Mann explains that he typically struggled to get past the HireVue stage of big companies’ recruitment processes, despite personal trading success. In a new venture, Bren, he aims to create a consultancy and small investment bank with the goal of “kickstarting a neurodivergent economy”. The venture is backed by four co-founders and 11 autistic CEOs, he shared, and is advised by City of London Corporation’s start-up trust and an ex-McKinsey consultant.

Is setting up an entirely new ecosystem the best way to create a neurodivergent-friendly space within trading? Aside from lip service and inclusivity-washing, what do mainstream firms need to do to truly change the industry?

What’s out there?

Beyond firms’ internal efforts, a number of industry participants have taken the issue of neuroinclusivity into their own hands. One such group is Genius Within, a UK specialist firm that supports neurodiverse individuals in the workplace. Established in 2011, the company began with coaching programmes and now offers diagnosis services, consultancy, training for businesses and various other support mechanisms.

Royston Collins

“There’s a lot of support we provide within the financial sector already, and many [firms] were quite open to it,” says customer services director Royston Collins. “Initially there was a lot of reluctance; people thought neurodiversity was just a buzzword. But now a lot of firms have realised that they’ve got a lot of talented people who are neurodivergent on their teams – probably more than the national average.”

In the last few years, Collins has noted an uptick in the number of referrals for one-to-one coaching support from firms, who refer their employees to the organisation when they need support and recognise the value that it can bring. Coaching is a relatively cheap, low-intervention service that doesn’t require receivers to go through lengthy assessment and diagnostic processes. It doesn’t even count as a reasonable adjustment; people learn different ways to work or communicate, and are then able – in theory, at least – to implement the practices into their working life.

The champions and mentors in this programme are often higher-ranking employees in the industry, Collins explains, which not only has the benefit of sector-specific advice but also allows those looking for guidance to see that they are not alone in the industry.

Nalini Solanki

This is something that Nalini Solanki, Edmans’ co-chair at The Diversity Project, agrees is a crucial part of improving the experiences of neurodiverse traders. Change needs to come from the top, the pair say, with members of C-suites disclosing their diagnoses and building a culture that accepts and supports neurodiversity.

Over recent years, “the biggest change has been being able to talk about [neurodiversity],” Solanki says. But even though progress is being made, she reports that the financial industry “still [has] a sense that ‘it’s not us’”. Many advocacy groups see awareness as one of the first steps that businesses can take to become more neuroinclusive, and most businesses are at this first stage of change, explains GAIN committee member Liselle Appleby. Once the ball starts rolling, people are more likely to understand neurodiversity and the adjustments that can, and should, be made to allow everyone to work to the best of their ability. “When you start raising awareness, your perspective changes,” Solanki adds, with a significant realisation being that neuroinclusive initiatives tend to benefit neurotypical employees, too.

Benefits to the firm

Liselle Appleby

While it might be easy to disregard neuro inclusivity as a virtue signalling activity, evidence suggests that from a purely results-driven perspective it’s equally as beneficial for firms to take a more active approach to neurodiversity as it is to their employees.

“Tailored support helps create an inclusive environment where employees feel understood and supported and are more likely to be engaged and motivated while contributing to improved wellbeing,” Higgins explains. “It’s important for recruitment, retention, and advancement that the specific needs of individuals, such as those with neurodivergence, is discussed and communicated to create a truly inclusive and supportive workplace.”

The fact that there are differences between neurotypical and neurodiverse brains and thought patterns has often carries negative connotations – particularly in the recent past, when ideas of neurodiversity were based firmly in stereotype-ridden fiction rather than fact – but the advantages of hiring neurodiverse employees are now actively being championed. Whether it’s an ability to ‘think outside the box’ or identify patterns and make connections in ways that others miss, having people who think differently on a trading floor can be a huge advantage.

“Autistic people tend to be more process driven and oriented; ADHDers tend to react very quickly and can stay focused on something they love for a long time,” Mann explains. “This can lead to quick reactions, a strong theory of mind when it comes to understanding yourself and strong process following.” He brings up perhaps the most famous case of how neurodivergence can benefit traders: Michael Burry, the famously autistic founder of hedge fund Scion Capital who predicted (and profited from) the US sub-prime crisis, and was immortalised on film by Christian Bale in The Big Short (2015).

Although examples like these highlight the myriad benefits that neurodivergence can have for traders and trading firms, it’s important to avoid the stereotype of the ‘autistic savant’ –the assumption that neurodivergent individuals all hold special, almost mystical abilities. These kinds of preconceptions, although often framed as ‘positives’, can have a distinctly negative impact on mental health by ‘othering’ neurodivergent individuals and creating the sense that their worth is measured by extraordinary intelligence.

Reasonable adjustments

A lot of the measures that firms can take to be more neuroinclusive are relatively easy to implement; providing noise-cancelling headphones, creating ‘sensory maps’ that highlight areas of high sensory stimulation in offices or, perhaps the most widely recognised change over recent years, allowing employees to work more flexibly – whether in terms of schedule or location.

Of course, this final point is a challenge when it comes to trading. As an inherently time-bound business there’s a lot less scope for working at one’s own pace, and technology and security requirements mean that a home-working setup can be difficult to implement. Edmans recalls that traders were “practically the one group that was always in” during the pandemic. While many neurodiverse people realised that a hybrid approach was exactly what they needed during lockdowns, “that revelation couldn’t have happened for traders”, he adds.

Tim Edmans

Being neuroinclusive does not mean only catering to those who need workplace adjustments, but breaking away from rigid approaches to how a workplace operates. At The Diversity Project, Edmans and Solanki are championing cognitive diversity as one of their focus points in 2024. “It’s about recognising that everyone has a different way of approaching things, thinking and perspectives,” Solanki explains. “When our teams are more balanced in the way that they think and behave, you get far better results – because of that diversity of minds.”

This is something Mann agrees with, and aims to foster at Bren. However, rather than pushing for integration between different styles of thinking, he advocates for a radically different approach.

“I think honestly, neurodivergent people should lead their own teams separate from neurotypical people,” he states. “We think too differently to have effective collaboration if we work directly together.” Groups should work independently, he suggests, before those from each team who have good communication skills share and connect their work. “People will feel a lot more included when surrounded by like-minded people who listen to them,” he says, adding that this strategy extends to “tribes of neurotypicals” too – introverts and extroverts in their own groups, for example.

While it may seem discriminatory to deliberately push different thinking styles apart, “I’ve done a couple trials and done several studies of this model, and so far it’s been very successful,” Mann claims. He reports that the idea transfer is significantly improved in this structure, and that it allows for diverse thinking styles to more effectively coexist.

Exploiting the system

There will always be naysayers – those who believe society is becoming “too sensitive”, and people asking for adjustments are just trying to get special treatment.

But of course, the reality is far more nuanced than that. “You see reports that people are jumping on the bandwagon and there genuinely are some that are performative,” Collins says, noting that Genius Within does deal with, and support, people who sometimes blur the lines between what they want and what they need. That being said, it’s important to note that this does not represent the majority; and for some, this style of work can be genuinely overwhelming and does not play to their strengths.

“It isn’t that there’s overdiagnosis or that there are too many people saying “me too”. That’s simply not the case. We’ve just made it easier to talk about,” says Solanki. The problems that neurodiverse employees are facing are not new, but have for the most part been ignored or suffered in silence by the majority of those affected.

What needs to happen now?

Firms’ internal efforts, the work of advocacy and employee resource groups and changing social attitudes are all making a difference when it comes to neuro inclusivity in the workplace; but it’s clear that there’s still a lot of work to be done before the industry is truly supportive of neurodiverse employees.

Currently, even if firms are trying to offer support to their employees, it’s so poorly signposted that many of those who would benefit from assistance are unaware that it exists, or don’t know how to access it. “Especially in the financial sector, [firms are] quite disparate in what they do,” says Collins. “They have so many different divisions, and one part doesn’t know what the other part is doing. They don’t have somewhere central for people to go if they need help, so people don’t know how to ask or where to go.” Even companies that have been working with Genius Within since its inception have this issue, Collins reports “My advice would be that they consolidate and make it easier for employees to find the help they need internally, perhaps through their employee resource groups or occupational health services”.

One firm that has implemented this approach is Invesco, which runs a neurodiversity business resource group. The group both raises awareness, offers a forum for members to share resources, learnings and literature that have been helpful to them, and discusses how the workplace can be more inclusive for neurodivergent employees.

Devvya Sharma

Devvya Sharma, EMEA diversity and inclusion manager, sees the industry trending towards offering a ‘neurodiversity passport’. This document “captures all [an employee’s] requirements so that every time they change role, or change manager, the passport travels along with them”. Implementing this document “saves the individual from repeating the request again and again,” she explains, reducing stress and streamlining the adjustment process for the company.

Across the board, advocacy groups agree that raising awareness is one of the most important and effective ways to improve the lives of neurodiverse individuals and make society, and the industry, more inclusive. However, this requires real, proactive engagement at both a grassroots and board level. If neurodiversity is only ever spoken about on a theoretical level, can real change ever truly occur?

Allegra Berman will leave HSBC at the end of September, according to an internal memo seen by Global Trading.

Berman joined the firm in 2013, leading the global public sector business, before becoming head of FIG for EMEA and in 2015 and global co-head of securities services in 2018. She was appointed global head of institutional sales for markets and securities services (MSS) in 2020.

A replacement has not yet been found for Berman, the memo stated, noting that members of the institutional sales executive committee will report to regional MSS heads in the immediate term. Chris Georgs, chief operating officer for institutional sales, will manage global coordination in the interim.

Patrick George, global head of MSS, concluded the memo: “Allegra’s authenticity, support, and trusted counsel have been invaluable, and she will be greatly missed both professionally and personally.”

The number of companies choosing to go public in Europe and the UK is continuing to decline, with firms opting for US markets when launching their IPOs. As capital continues to flow out of Europe, the Federation of European Securities Exchanges (FESE), along with the European Startup Network (ESN), have published an open letter to EU finance ministers and the European Commission, calling for the fulfilment of the Capital Markets Union (CMU).

The CMU intends to create a single market for capital in Europe, increasing the flow of investments and savings to the benefit of consumers, investors and companies. After a decade of discussions, legislative proposals, rewritten packages and action plans, the union has not yet been realised – and European markets remain fragmented.

According to a McKinsey report published in June, since the first action plan for the CMU was introduced in 2015 Europe has missed out on US$439 billion in ‘lost’ IPOs – not counting companies that have jumped ship and relocated pre-IPO. In 2021 alone, the US hosted more tech IPOs than Europe did between 2015 and 2023.

FESE stated that tech companies’ decisions to go public in the US are logical, with the region offering “deeper and broader pools of capital, potentially higher valuations, and a better-integrated listing and trading ecosystem”. Led by Nasdaq and NYSE, the region represents half of global market capitalisation.

However, what appears too good to be true often is. An April study from Euronext has shown that, comparatively, “the presumed dominance of the US in equity liquidity is not as advantageous as it might seem”, FESE said. European firms may not see the same benefits as their American peers when going public in the region, it suggested, citing lower valuations, reduced liquidity and less comprehensive analyst coverage as potential downsides. As such, there is an opportunity for Europe to claw back more of the pie.

Europe needs to provide an environment in which companies can access sufficient investment opportunities, FESE argues, encouraging them to go public in their region of origin. This will allow for jobs, patents, talents, tax payments and economic returns that are created to remain in the EU, it said, while improving EU competitiveness, innovation, sustainable growth and job creation.

The European Commission is already taking action in this space following pressure to complete the CMU. Following a report from former Italian prime minister Enrico Letta earlier this year, commission president Ursula von der Leyen has voiced her intentions to also implement the European Savings and Investments Union. This will unlock private savings, Letta argued, which can then be channelled into the region’s markets rather than diverted to the US.

In their letter, FESE and ESN outlined four additional aspects of the CMU that could improve the European IPO market.

Growth-stage venture capital should be boosted in order to strengthen upstream investment in the stock market, the organisations argued, giving scale-ups sufficient funding to scale and, in the long run, fostering a tech and startup ecosystem in Europe.

Cross-border transaction costs for equity investment should be eliminated, they continued, stating that European investors are currently incentivised to buy national or American shares rather than European shares by complex withholding tax regimes. Streamlining these processes will help investors to diversify portfolios and support company growth in the region, the firms said, adding that the taxation of options products should be harmonised as much as possible in order to support scale up and participation for EU startups.

Mobilising retail investment is another priority, with the letter stating that the wealth of retail accounts needs to be unlocked to support both the primary and secondary tech markets. To do so, financial literacy among EU citizens must be improved. Currently the letter says, just 28% of European citizens are invested in financial products. In order to change this, European governments and local financial ecosystems need to create a narrative that encourages trust in capital markets, induces interest in financial products and increases investment in technology. Tax incentives for savings to stimulate long-term equity investments rather than short-term deposits and low-risk instruments are also needed, the organisations continued, arguing that risk-taking should not be overly discouraged. “These investments are not only crucial for advancing the EU’s twin digital and green transition, but also for creating prosperous European savings,” it affirmed.

Incentives also need to be offered for both retail and institutional investors to invest in European companies, the letter continues. In the first instance, it said, a tax and regulatory environment that removes barriers to existing investment flow should be implemented. Creating a pan-European label for trusted venture capitalists, or a European fund-of-funds, would give institutional investors an incentive to invest in tech and other industries at both pre- and post-IPO stages, it added.

Deutsche Borse, Euronext, France Digitale and Startup-Verband have also backed the letter.

Kepler Cheuvreux has expanded its offering in Europe through a connection to Euronext Dark, and extended its equity capital markets partnership with Crédit Agricole CIB into the MENA region, opening an office in the Dubai International Financial Centre (DIFC).

Some investors are convinced that lit trading is bad for their financial health – and trading firms are responding by channelling them towards dark venues. Speaking to Global Trading, execution sales team member Athina Trika stated that “dark trading continues to be a vital liquidity source for institutional investors.”

Connecting to Euronext Dark allows the firm to trade at midpoint across all seven Euronext exchanges. The service was launched in April this year, and allows users to source liquidity within Euronext’s central order book and make orders pegged to the real-time mid-point of the Euronext best bid offer.

Explaining the firm’s engagement with the strategy, Trika continued: “As an agency broker, our primary focus is to help clients access liquidity while minimising market impact. By joining Euronext Dark, we expand our reach to seven additional European dark venues, enhancing the range of matching opportunities and functionalities we offer to clients.”

According to the exchange, Euronext Dark has recorded a 47% increase in volumes between April and August and has seen average daily trading volumes of up to 22.8 million. Currently, 13 active trading members use the platform, while another 20 are in the testing phase.

The expansion into MENA follows interest from institutional investors in the region, said Laurent Quirin, chairman of the supervisory board, “where ECM activity is booming”.

Through the newly-established local presence, Kepler Cheuvreux will initially offer equity research and distribution in the UAE, which it was licensed for by the Dubai Financial Services Authority (DFSA) on 26 July, the Kingdom of Saudi Arabia and the Gulf region.

Claudio Villa, managing director and global head of equity primary markets, and Mathieu Labille, managing director and deputy head of equity brokerage, will be leading the MENA division, Kepler Cheuvreux revealed to Global Trading. Further details are expected to follow.

Crédit Agricole CIB will incorporate equity capital markets activities into its existing offerings in the region, it stated, developing its service portfolio and granting clients access to Kepler Cheuvreux’s international investor network and European research offerings.

“This new step in the history of Kepler Cheuvreux demonstrates the efficiency of our model and strengthens the group’s multi-local position,” Quirin commented.

Didier Gaffinel, deputy general manager and global head of coverage and investment banking at Crédit Agricole CIB, added: “Our partnership with Kepler Cheuvreux has proven to be highly successful in Europe with a number of flagship transactions. We are fully committed to the success of this new initiative and are strongly convinced of the value-add we bring to MENA equity capital markets issuers through our platform.”

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] Please review our updated Terms & Conditions and Privacy Policy carefully. By continuing to use our services after Aug 25, 2025, you agree to these