Shifting EU-US credit valuations, navigating data gaps, and the rise of portfolio trading

Sarah Harrison, senior portfolio manager at Allspring Global Investments, discusses the firm’s evolving view on valuations across European and US credit markets this year. As the US government shutdown continues, she unpacks how her firm adapts its forecasting models amid disruption to economic data releases and shares how the firm’s portfolio managers are collaborating closely with traders to execute cost-effective strategies, highlighting the firm’s growing use of portfolio trading in 2025.

In this episode:

• Shifting views on Europe Vs US credit valuations

• Navigating data disruption and adapting the forecasting model

• PM and trader collaboration on the desk

• Portfolio trading vs. line-by-line strategies

• Why is discipline crucial going into the year-end

This show is supported by Cabrera Capital Markets.

As electronic liquidity providers become more ubiquitous in cash equity trading, they increasingly compete with traditional market makers, namely the trading arms of large global banks. According to a document obtained by Global Trading, Citadel Securities had $18 billion of trading capital in March 2025. Compare that with Goldman Sachs, which had $100 billion of common equity tier 1 capital and a $2 trillion balance sheet.

This difference gives the banks a crucial advantage – they can use their balance sheets to support outsized over-the-counter derivatives positions alongside their cash securities trading. This allows them to compete for lucrative mandates such as share buyback VWAP trades, that elude the newer ELPs.

Now, one such ELP, Susquehanna has teamed up with consultant Acuiti to release a report complaining about an aspect of banks’ derivative activity: so-called pre-hedging. Susquehanna is tapping into buyside disquiet about RFQs and IOIs that move the market – a sign, some say, that banks are pre-hedging more than they should. It’s a “very tricky subject”, one buyside trader told Global Trading.

And don’t forget that ELPs have a vested interest of their own in making such arguments.

SIX has appointed its subsidiary Aquis Technologies as technology provider for its trading platforms, following a multi-stage selection process.

SIX completed its acquisition of Aquis in July, with a £224.6 million deal.

In its interim report, SIX stated, “The primary reason for the business combination is to create a pan-European exchange innovator across the primary exchange and multilateral trading facility businesses, with access to 16 capital markets across Europe.”

On the new commercial agreement, an Aquis spokesperson told Global Trading, “The selection process was conducted wholly independently to the acquisition on a competitive basis and was initiated well in advance of SIX’s approach to Aquis.”

Aquis’ Equinox matching engine will now be used across all SIX Group exchanges, which it says will allow users to access more liquidity. A new platform for equity and equity-like products is expected to go live in 2027. Other asset classes will follow.

“As exchange innovators, SIX and Aquis will continue to build on this successful basis by further expanding its technology business in the coming years,” SIX said.

SIX does not break down its IT costs, but according to its interim report the group spent £23.2 million on property, plant and equipment additions, including IT hardware and technology installations, in the first six months of 2025. This marked a 15% increase year-on-year.

A further £29.4 was spent on transformative costs, a portion of which included IT infrastructure.

CNSX Global Markets, parent company of the Canadian Securities Exchange (CSE), has acquired National Stock Exchange of Australia (NSXA) parent company NSX.

The all-cash deal, approved by 94.78% of NSX shareholders, would see ordinary shares purchased at AUD 0.04 each.

NSX chairman Tim Hart commented, “[We] look forward to giving the Australian market what it needs: greater choice for investors to build wealth and a lower cost of capital for companies to fund their growth, especially in the early-stage and venture space.”

NSXA is currently the second largest primary listing venue in Australia, with 51 listed securities. According to Macquarie Equity Research, close to 550 further companies would be eligible to list on the platform.

Competitor Australian Stock Exchange (ASX) has more than 2,000 listed entities.

Australian equity markets have struggled with liquidity issues in recent years, in part due to a small investible universe, market participants have said.

Earlier this year, Cboe received Australian Securities and Investments Commission (ASIC) approval to launch a listing market in Australia, putting it in direct competition with the incumbent ASX.

Max Cunningham, NSXA CEO and managing director, will continue to lead the exchange, with CNSX Group providing financial, technical and strategic support. CSE CEO Richard Carleton is expected to join the NSXA board of directors.

“The CNSX Group and NSXA are taking immediate steps to strengthen the NSXA’s competitive position in Australia and build a dynamic exchange alternative tailored to the needs of early-stage companies in Australia and beyond,” CNSX stated.

Planned actions include upgrades to the NSXA tech stack and a hiring spree to build out all business lines.

Cunningham noted, “Another exciting aspect of our partnership is the potential for inter or dual-listing opportunities across our exchanges for Australian, Canadian and global companies, which multiple entities in the mining and early-stage tech space are exploring already.”

The Financial Conduct Authority (FCA) is seeking feedback on its proposed short selling regime, which will anonymise reporting and, it says, encourage growth.

The FCA has overseen short selling regulation in the UK since 2023, when it was given rulemaking, supervisory and enforcement powers by the UK Treasury.

The UK short selling regulation (SSR) was initially based on the EU framework, but now differs in a number of ways.

An initial call for evidence, completed in 2022, concluded that fundamental changes to the short selling regime were not required. However, a number of tweaks have been proposed to reduce the reporting burden on firms and remove potential barriers to short selling, while ensuring that the strategy is not overused.

In the updated regime, all individual net short positions reported above the 0.2% threshold would be combined, anonymised and disclosed. By contrast, the EU requires all short positions over 0.5% to be publicly reported, along with details of the transactions.

This aggregated reporting is in line with the 2025 Short Settling Regulations, a legislative framework published by the UK Government in January. Further guidance on how these aggregate net short positions are calculated, published and updated will be provided in due course.

Patrick Sarch, partner and head of UK public M&A at White & Case, commented, “There is no substantive change to what investors can do – it will simply mean there is less transparency regarding who is short of what.

“In fact, many investors don’t mind being named or actively prefer to be. The real impact will be on the issuers who will have less visibility on who is holding short positions in their stock and whether those positions are concentrated or spread across multiple investors.”

“Ultimately, these changes won’t make a material difference to the efficiency or attractiveness of the UK market. There will be slightly less compliance friction for short sellers and their intermediaries, but at the expense of transparency for issuers and other investors.”

Partners at AO Shearman disagree. In a January report, the law firm said of the anonymous reporting, “This is a welcome change, particularly for asset managers who for years have been concerned about copycat behavior, short squeezes and potentially revealing trading strategies. The changes are intended to encourage more trading activity and greater liquidity in U.K. markets.”

While public disclosures of short positions will no longer be mandated by regulation, voluntary disclosure may continue – as is seen in the US.

Tom Matthews, partners and head of EMEA activism at White & Case, noted, “We will therefore continue to see short selling “bear attacks” by specialist short selling hedge funds, who publish negative reports on a company in parallel with placing short bets on its stock.”

The SEC’s regulation SHO, which governs short selling, is currently under consideration after legal challenges.

Firms would also be given more time to submit their position reports under the FCA’s new rules, with a deadline of 23:59 T+1. The processing time for the regulator, and the time it takes to provide guidance on how firms should determine the issued share capital of companies in order to calculate their positions, will be reduced.

The list of shares bound by the rules will be updated, with the criteria for inclusion expanded.

The FCA additionally intends to automate and simplify its systems for the receipt of position reporting and market maker exemption notifications.

“Aggregated net short positions and simplified processes for reporting will enhance and streamline the short selling regime in the UK, reducing burdens for capital market participants while ensuring the market still gets the transparency it needs,” said Simon Walls, executive director of markets at the FCA.

“These proposed changes are another important milestone in our drive to become a smarter regulator and to support growth.”

Comments on the consultation paper will be accepted until 16 December.

Trian Fund Management and General Catalyst Group have submitted a joint proposal to acquire Janus Henderson Group, taking the UK asset manager private.

Known for being an activist investor, hedge fund Trian holds approximately US$6.3 billion in assets under management. Venture capital firm General Catalyst has previously invested in companies including AIM, Anthropic and Mosaic.

Trian has been invested in Janus Henderson since October 2020, and holds 16.7% of the firm’s outstanding common stock. If accepted, the remaining ordinary shares not currently held or controlled by Trian will be acquired for US$46 per share in a cash deal.

This represents a more than 56% premium on the shares’ price as of April 2025. The overall offer of US$7.2 billion values Janus Henderson at more than 9.5 times its trailing 12-month earnings, as of June 2025.

In Q2 2025, Janus Henderson reported US$457 billion in assets under management.

The firms’ letter to the SEC stated, “Trian Management and General Catalyst stated they believed the Issuer has an opportunity to enhance client’s experience and further its strategy by significantly increasing long-term investment in the Issuer’s product offerings, client service capabilities, technology and talent.

“Trian Management and General Catalyst further indicated that they believe these investments can more effectively be done free from the constraints of operating as a public company.”

3D rendering robot humanoid walk up stair to success and goals achievement. Concept of AI thinking brain and machine learning process for the 4th fourth industrial revolution .

Automation, a buzzword of the moment, is drastically changing how trading desks are run. But the way that firms are approaching the technology differs greatly. As traders seek out increasingly marginal gains, the automation game is a competitive one – with numerous approaches.

The primary use case for automation in trading is around small orders. “It saves a lot of time,” says Evan Canwell, equity trader at T Rowe Price. “Automation can take some of those lower value-add jobs that are more repetitive and free up time so we can concentrate more on the higher value-add things, look at market colour.”

At T Rowe, smaller orders have become increasingly handled by machines over the past

Evan Canwell, T.Rowe Price.

eight years. No longer do traders have to take responsibility for tiny trades, selecting which algo to send them off to. “An order comes in, the parameters and characteristics are captured, and it’s sent off to our performance database,” Canwell relays. “We do some statistical analysis, a suggested broker algo is stamped on it, and if it’s a small enough order it will go straight out the door.” Humans still oversee the process, but with a much lighter touch.

It’s a similar story at UBS Asset Management (UBS AM), one that head of European equities trading Stuart Lawrence says aligns with the general approach on the street. “The [small] orders hit our trading desk, automate out to our EMS, execute in the market, come back, and mark themselves,” he recounts. “ The traders use pre-programmed execution

Lawrence Stuart, UBS

strategies that are driven by the technical factors of an order, which allows us to then automate the entire workflows.”

Lawrence shares that UBS AM has been automating much of its ETF flow over the last year.

“We’re constantly trying to see what else we can automate, freeing our traders to do more thinking and less processing.”

“Without going into specifics, our automation is set up to deal with a host of order types and sizes. We initially set up automation to assist with the trades where traders can add limited value (low ADV, low notional) but we are now expanding our methodology to add new approaches and opportunities to make our workflows more efficient.”

Complex orders

That said, “we don’t just throw everything into automated systems,” Lawrence assures. “We have very strict rules around which orders can be sent through – based on notional, ADV, the market, etc. and we always ensure we have someone on the desk with oversight of the automation at all times.”

For UBS AM, orders requiring more attention include those with a high notional value, super liquid stocks or those that are part of a contingent basket, “That’s where traders can really add value, based on their experience and knowledge of how best to achieve an outcome,” Lawrence adds.

For larger orders, those that traders are expected to focus on once the scraps have been hoovered up, there’s still a place for automation – but as a copilot rather than a controller. “In these cases, an algo suggestion is just that – a suggestion,” Canwell says. “The trader can choose whether to take it or overrule it.”

“There’s a point when the order stops being something that can be automated and needs a trader’s eyes on it,” Lawrence says. “The desk needs to be nimble when it comes to finding that sweet spot. We’ve coded our parameters for automation to allow traders to focus on where they can add the most value.”

Canwell agrees. “Our non-automated flows are those which require some form of human intervention, so they’re typically larger or block-sized, or have specific execution instructions from a portfolio manager.”

Totally random

Broker allocation and algo choice are one of the key uses of automation in trading, but the degree to which these practices should be randomised is up for debate.

At UBS AM, Lawrence explains,“We have full randomisation within our algo wheels, which promotes fairness for measuring performance, so no one broker benefits more from the orders they receive than others. It’s a kind of league, relegation-promotion system; if one broker is consistently underperforming, we either reduce their weighting in the wheel or remove them entirely.”

The wheels are assessed twice a year – Lawrence expects the timeline to be condensed to once a quarter in the near future.

“We need to be constantly asking who’s best for this particular market, this particular strategy,” he says. “It’s important that we’re constantly evolving. We don’t just keep brokers because they’re the incumbents.”

UBS AM uses a mixture of in-house and vendor applications for its automation projects, Lawrence notes. Its algo wheels are built and operated within the firm’s EMS, while OMS to EMS automation is developed internally.

At T Rowe Price, the set-up is very different. There’s a degree of randomness to the allocations – between a 10-20% chance of any broker being selected – to ensure that the top algos are performing consistently well. But for the most part, the order goes to the best performing broker.

“We’ve never really been a fan of randomised algo wheels,” Canwell shares. “We want to replicate the way that a trader would think about an order, rather than replace the trader. If they’re thinking about an order manually, and don’t have an initial feeling for where to send it, they might look at TCA data and see which brokers have performed best in past similar cases. That’s what our service replicates.”

For Canwell, the key is mimicking human behaviour and offering suggestions to traders.

2.0

Lawrence wants to start using ‘waterfall wheels’ at UBS AM, a second generation of algo wheel that goes beyond just routing orders based on set parameters.

“As a simple example, think of it as a trickle-down,” he explains. “First we see if we can get a mid-price fill. If that doesn’t work, we bring it down to the next level and try to get 100% fill on the touch. If that doesn’t work, we might try and rest in dark for a couple of minutes. If that doesn’t work, we finally might say, ‘well, there’s no other liquidity out there that we can use right now’, and route to the algo wheels as we previously did.”

With the liquidity landscape changing, and electronic providers increasingly prominent, there are a lot more flows to tap into. Desks want to take advantage of that.

“It treats smaller orders in a similar way to bigger ones, so we always see if there’s an opportunity to trade in the spread through liquidity providers who offer mid-spread liquidity,” Lawrence continues. “We can eke out small gains from that. If you’re constantly getting an extra 30% of your fills at the mid rather than on the touch, you’ll see a meaningful difference to performance.”

This kind of tool is already used at rival asset managers including Groupama, former head of trading Eric Heleine told Global Trading last year.

Some market players have suggested that while this kind of waterfall logic is nothing new, it has been automated in recent years thanks to increased bilateral trading and the democratisation of more advanced execution management system technology.

Pre-trade

Beyond allocation, automation also has a significant role to play in pre- and post-trade analysis to enhance execution.

T Rowe’s Canwell detailed one way that the firm is thinking of bringing automation into its data processing.

“We put together a daily trading note manually, bringing together Bloomberg messages, broker emails, things like that. In the future, we could compile all those into a nice format – probably using an AI tool like an LLM – and then have a trader decide whether that output is good enough or needs changing.”

It’s something that’s front-of-mind for investors across the board. “Automate the noise, focus on execution,” is a focus of many.

There is some question, however, as to how much data will be accessible for such systems – big data providers may be less keen for their outputs to be scraped. Equally, trading firms may not be ready to hand over their data. One trader observed that although there is a lot of talk about the use of AI on the desk, the reality is that few are actually implementing it in meaningful ways.

T Rowe’s automated trading services have all been developed in-house, with just one external vendor used. “That’s purely for supplying data points, such as pre-trade cost estimates, to help choose an execution algorithm,” Canwell affirms.

Already, according to Global Trading’s recent buy-side survey, just 14% of traders are using in-house tools for pre-trade automation and complex execution. The majority outsource these tasks to a vendor tool (59%) or use a broker tool via website access (27%). Automation can be both a helpful tool for firms with limited resources and another budgeting headache – especially for smaller companies.

Earlier this year, Mathias Eriksson, senior trader equities and credits at Swedish pension fund AP2, shared how the firm uses vendor AI technology to wrangle data and lead its broker allocation decisions.

From a vendor perspective, Ovidiu Campean, product director for LSEG Execution

Ovidiu Campean, LSEG Execution Solutions

Solutions, sees the benefit in giving clients the opportunity to customise their solutions. “The more flexibility we can provide to clients to incorporate their own logic and criteria into the wheel and into the automation, the more we see clients implementing our own automation and wheels,” he affirms.

“We’ve seen shifts towards Alternative Trading Systems (ATS) and conditional block cross platforms, which are meant to help clients find bigger blocks of liquidity while minimising slippage and market impact, and reducing adverse selection. There are also many that employ diverse AI models to improve execution quality.

Giving insight into LSEG’s offerings, he added, “Our order and execution management systems operate as normaliser layers across both lit and dark type venues, so we can provide venue agnostic access to liquidity, improving clients’ chance for best execution. We’re continually adding venues to our platform, so we’re riding on this trend, giving clients optionality and flexibility across global asset classes.”

How low can you go?

It’s easy to get swept away by the thought of algorithms and automation taking over the trading floor – but even enthusiastic market participants are clear that this is some way off.

One trader explained that automation could, for equities, have reached its ceiling. Aside from small tweaks here and there, and advancements made possible through enhanced data visibility (which the consolidated tapes intend to bring), there is not that much room to grow in the asset class.

Others disagree, believing that automation can go further – with caveats.

From a governance perspective, regulation of automation needs to include internal policy frameworks for fiduciary duty and trading ethics, ensuring that brokers or routes are not favoured in a way that harms clients, Campean notes.

“Another thing to monitor is data quality and input controls, where you see how much data quality contributes to the decision an automated system is making. You have to have high-integrity, latency-aligned, real-time data, or the model will perform on stale sources.”

On a practical level, he adds, “For a while you’ll need human oversight and controls, especially kill switch and escalation path capabilities. If the model goes haywire due to high volatility or the system connectivity to markets breaks, you need to have controls in place, otherwise the model could flood the system or the exchanges.”

“Reasoning artificial intelligence may still be a decade away, and until such robust systems and models emerge, the idea of eliminating human oversight remains highly improbable.”

That said, Campean does expect to see AI being increasingly used in trading automation, acting as a co-pilot to traders and providing increasingly complex insights into growing reams of data.

Canwell sits between the two perspectives.

“There’s already some level of machine learning in algos, used to fine-tune parameters over time,” he says. “I can see that increasing, with more brokers pulling in more data to improve their offerings. The world is only getting more quantitative, and I think traders want to be able to benefit from that.”

But, he concludes, “the near-term future won’t be too dissimilar from where we are now.”

Ako Nishi, Executive Director, Central Dealing, J.P. Morgan Asset Management (Asia Pacific).

After years of stagnation, Japan’s equity market is booming and alternative trading system providers are flocking in. Buyside traders now hope that the stranglehold of HFT firms will be broken.

With its first female prime minister and the stock market at a record high, Japan is attracting a new influx of domestic retail and foreign investment. But first, the country’s buyside giants want aspects of Japan’s creaking markets infrastructure to be fixed.

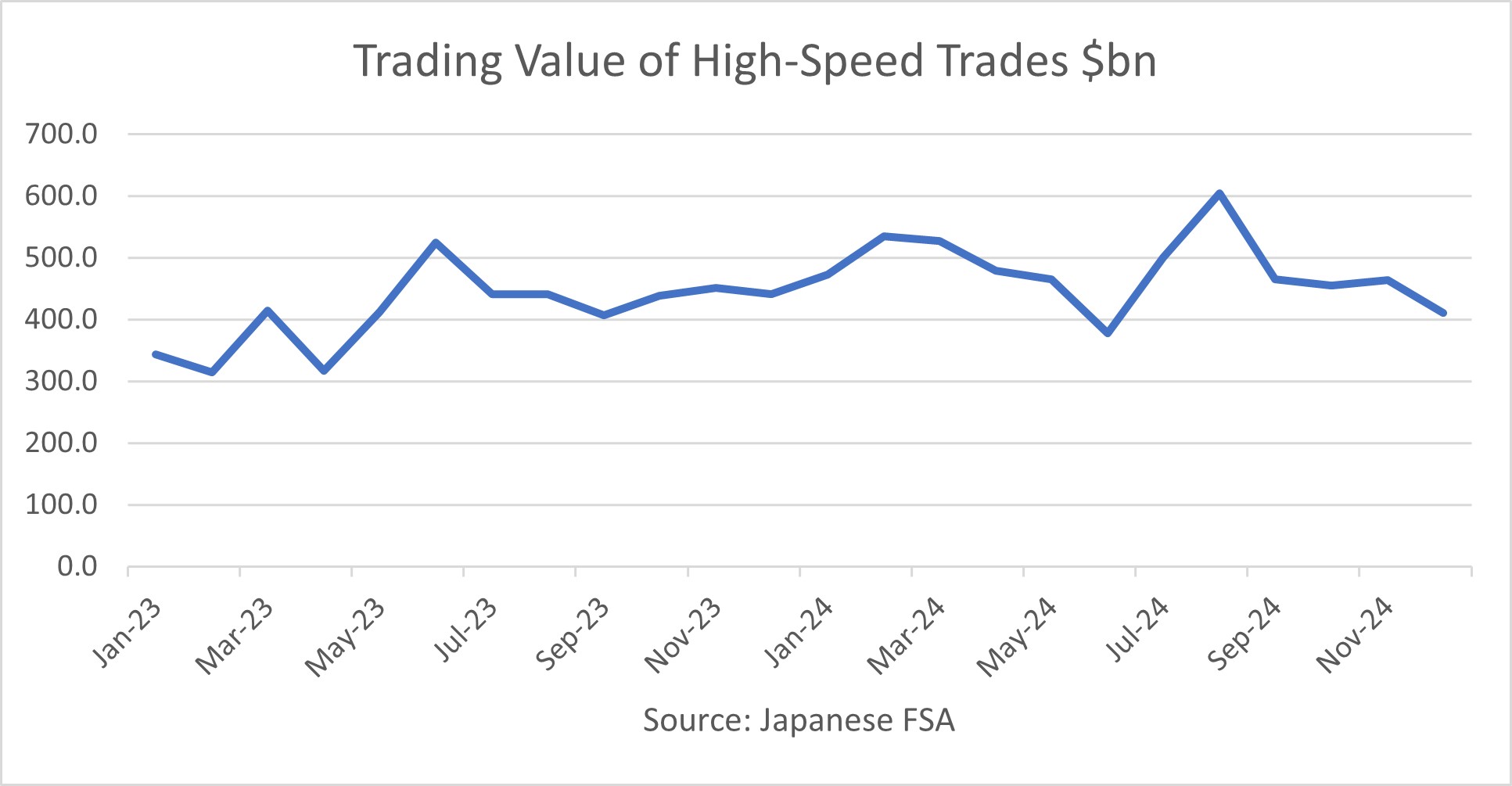

Chief bone of contention is the dominance of high-frequency traders in Japan’s lit equity markets, a development encouraged by the Tokyo Stock Exchange, whose Arrowhead system allows low-latency access to its matching engine. According to the Japan Financial Services Authority (FSA), which regulates HFT firms and compiles data on their activity, HFTs accounted for 35% of TSE volume at the end of 2024. That compares to 17% on HFT-friendly Eurex, based on Global Trading analysis.

For buyside traders who submit orders via brokers, the result is a chronic information leakage problem. “We place great importance on brokers with abundant liquidity” Kenji Takeda, head of equity trading at Nomura Asset Management told the audience at the FIX Japan Electronic Trading conference in Tokyo on 8 October.

“However, I think that the key factor behind this is how to prevent prices from fluctuating, so I think that a clean flow is an absolute requirement. However, when it comes to Japanese stocks, there is a lot of HFT and it is a market that is prone to gaming, so I feel that this is an important point”.

This perception about HFT is shared by non-domestic buyside firms that trade Japanese stocks. “When I execute this alongside other Asian stocks, I feel that it is very difficult to ensure liquidity in the Japanese market” said Ako Nishi, a trader at JP Morgan Asset Management based in Hong Kong. “One factor is the high market share of HFT. In terms of ensuring liquidity, I think it is very difficult to interact with.”

Ako Nishi, Executive Director, Central Dealing, J.P. Morgan Asset Management (Asia Pacific).

These difficulties often lead Japanese buyside equity traders to explore non-order based liquidity such as indications of interest (IOIs). Yet here too, problems with information leakage are rife. “When we send IOIs, the market moves, which is very strange”, one trader told Global Trading. According to Nomura Asset Management’s Takeda: “I feel that IOI has become much more transparent than it was in the past, but at the same time, I still feel like some parts of it are fake”.

Acknowledged as having a more systematic approach than domestic buyside firms, JP Morgan Asset Management’s Nishi told the FIX Japan conference that her firm quantified broker liquidity using data such as past reverse IOI hit rates. “All transactions, including IOI crosses, are incorporated into our broker evaluations, enabling us to analyze the impact of each trade on overall performance”, Nishi said.

New solutions coming to Japan

Junya Umeno, Head of Japan for OneChronos.

But improved analytics won’t solve a problem that is endemic to Japan’s trading venues, according to former Blackrock senior trader Junya Umeno, who recently was appointed CEO of OneChronos Japan. “The challenge for buy-side traders is that all the existing trading venues are based on price-time priority”, he told Global Trading. “That means first come, first serve. So buy-side traders don’t always have the budget to invest in their trading infrastructure, while algorithmic traders are investing a lot.”

Now, a new game is coming to Japan in the form of US-style Alternative Trading Systems (ATSs), that include Intelligent Cross parent company Imperative Execution, which is acting as a fintech in Japan, as well as OneChronos. Umeno explained what his firm was offering. “By conducting randomised periodic auctions roughly 10 times a second, we can remove the time factor from matching mechanisms as well. By doing that, the playing field is levelled for all participants, fast or slow”, he said. “OneChronos is addressing the specific needs for large institutional traders that have a goal to minimise information leakage.”

Conditional order matching is also growing in Japanese equity markets, though still far less prevalent than in Europe and the US. According to Umeno, “We support conditional orders, which allow participants to express intent to trade under defined conditions. Once those conditions are met, the order becomes firm – a transparent and efficient alternative to traditional IOIs.”

Meanwhile, the country’s markets regulator is moving to rein in the HFTs, and poor sell-side practices by imposing much larger penalties, with the Japanese Securities and Exchange Surveillance Commission (SESC), a division of the FSA, proposing changes in June 2025 according to its website.

A source familiar with the SESC said, “We would like to strengthen deterrence against unfair trading using accounts in other people’s names, raise the level of the surcharge for submitting large-scale holding reports, and, as cases of unfair trading involving HFT have also emerged, establish a method for calculating surcharges that corresponds to these new forms of trading”.

To download the full Japan Report click on the image below:

ION’s Fidessa platform is being used to support auction events on the London Stock Exchange’s (LSE) Private Securities Markets, operating under the Private Intermittent Securities and Capital Exchange System (PISCES) framework.

LSE was approved as the first PISCES operator in August. Participants on the platform have not yet been named, but Tom Simmons, director of private markets development at the LSE, confirmed to Global Trading that a number of companies are “in the preparation phase”.

“We’re trying to reuse as much of the public markets infrastructure as makes sense – principally that’s around trading execution, sharing of trading data and settlement. Investors will be using the existing pipes and plumbing from public markets to access intermittent trading events on the Private Securities Market,” Simmons said. As such, the LSE has tapped long-term collaborator ION to support its PISCES auction events.

ION’s Fidessa offers automated equity trading, covering execution and order management and middle-office operations. More than 6,500 buyside customers and 600 brokers are connected to the platform via FIX, and more than 200 global equity markets are covered.

Robert Cioffi, global head of equities product management at ION, told Global Trading, “We’re been able to leverage the existing connectivity we have with the LSE, and created a new trading segment for PISCES.

“Our clients are constantly looking to evolve their business and expand new market segments. So when something like the Private Securities Market comes along from the London Stock Exchange, which already has a large market presence, it made sense to be early movers in this new area of interest.”

ION’s customers will be able to access PISCES directly.

“Because of Fidessa’s scope of client coverage, many of the tier one broker-dealers who would be interested in accessing PISCES are already on our network,” Cioffi added.

PISCES will be delivered through a financial market infrastructure sandbox by the FCA before a permanent regime is established in 2030.

Barclays is set to open a Riyadh office next year, having received a provisional licence form the Saudi Arabian Capital Market Authority (CMA).

Once fully active, the licence will allow Barclays to practice investment banking and global markets activities in the country.

The bank’s total investment banking income was £3.3 million in the first nine months of 2025, up 4% year-on-year (YoY). The global markets business generated £6.9 million in income over this time, up 15% YoY – led by strong debt capital market activity.

Barclays’ existing Middle East franchise, with offices in the UAE and Qatar, is led by co-CEOs Khaled El Dabag and Walid Mezher. Trading operations for the region currently take place in London.

Group chief executive C S Venkatakrishnan commented, “Saudi Arabia is central to our Middle East growth strategy. Expanding our capabilities in the Kingdom is a significant milestone for us as we continue to grow our regional footprint in key markets.”

Mohammed Al-Sarhan has joined Barclays as independent non-executive chairman of the board for the Saudi Arabia franchise.

Chief bone of contention is the dominance of high-frequency traders in Japan’s lit equity markets, a development encouraged by the Tokyo Stock Exchange, whose Arrowhead system allows low-latency access to its matching engine. According to the Japan Financial Services Authority (FSA), which regulates HFT firms and compiles data on their activity, HFTs accounted for 35% of TSE volume at the end of 2024. That compares to 17% on HFT-friendly Eurex, based on Global Trading analysis.

Chief bone of contention is the dominance of high-frequency traders in Japan’s lit equity markets, a development encouraged by the Tokyo Stock Exchange, whose Arrowhead system allows low-latency access to its matching engine. According to the Japan Financial Services Authority (FSA), which regulates HFT firms and compiles data on their activity, HFTs accounted for 35% of TSE volume at the end of 2024. That compares to 17% on HFT-friendly Eurex, based on Global Trading analysis.