A new FCA review of algorithmic trading firms has found improvements since 2018. While governance frameworks have matured, the FCA urged closer alignment with MIFID’s Chapter 29, highlighting deficiencies in governance, testing and surveillance under RTS 6.

The FCA has published findings from a multi-firm review into algorithmic trading controls. It says that many firms have strengthened governance since its last review in 2018 but that it still found material weaknesses in compliance oversight, testing procedures and market abuse surveillance. The review sampled ten principal trading firms of different sizes and business models and assessed their compliance with RTS 6.

It has found that: “The quality of self-assessment documents and the overall self-assessment process have improved since our 2018 review.”

But the FCA also said: “There was, however, a significant variation in the sophistication of firms and their level of compliance, even taking account of the nature, scale and complexity of their trading activities.”

Better suited firms had external auditors review their RTS 6 self-assessments, which “often resulted in recommendations and tracked actions for firms to complete, to further strengthen their compliance.”

At weaker firms, the FCA said more detail was often required with deficiencies being addressed more efficiently. “This included out of date policies and unclear processes and documentation which indicated a lack of formal governance and accountability,” it said.

The role of compliance in monitoring algo is also not uniform. The FCA found that: “In some firms’ compliance staff had very strong technical knowledge and provided strong challenge to algorithmic trading processes. “

Others fell short, with the FCA noting that: “the compliance functions of some firms did not have as strong technical knowledge of algorithmic trading. This meant the ability of compliance staff to challenge trading behaviours was limited.”

RTS 6 requires firms to conduct robust conformance and simulation testing. But the FCA said while most complied with Article 6 obligations, that in some cases procedure to conform were not well specced which led to substandard recordkeeping processes. In simulation testing the FCA found a starker contrast with some firms allocating significant resources to testing, while others did not: “Simulation testing carried out by some firms lacked sophistication or did not appear to consider a wide range of market scenarios.”

The FCA found all firms operated pre-trade controls, but oversight was not always clear.

The review said: “In certain cases, ownership of pre-trade and post-trade controls was poorly defined and not documented”.

Market abuse surveillance systems were stronger at larger firms, many of which had in-house tools which were operationally sound to deal with potential market abuse.

But the FCA also said: “In certain cases, firms had not done enough to update or invest in their market surveillance systems. This meant their surveillance was not developing commensurately with the nature, scale, and complexity of their trading activities.”

While the review results were mixed, the FCA stressed that: “This publication creates no new requirements for algorithmic trading firms and is intended to help them comply with existing requirements.”

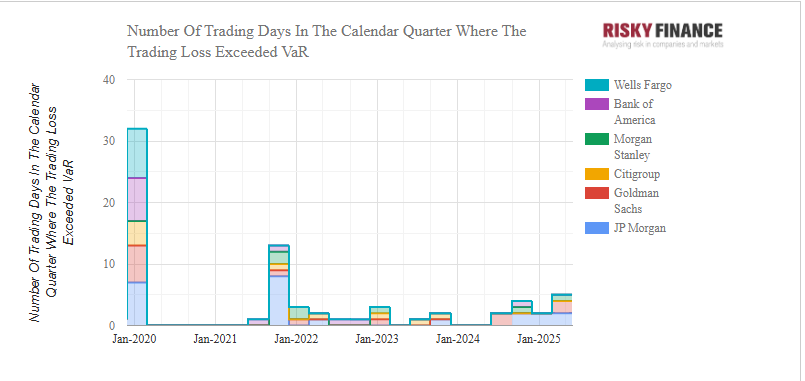

The Fed has started cracking down on bank trading book volatility, forcing JP Morgan to hold billions more in market risk capital. This happened after a quarter in which not only did US bank trading revenues hit a record, but the number of value-at-risk backtest exceptions reached their highest level since 2021.

The largest US banks may have reaped record trading profits in the quarter that started three days before US President Trump introduced tariffs on 2 April, leading to a six-week period of unprecedented volatility. But this performance came at the expense of trading book stability, as measured by the number of VaR backtest exceptions tracked by the Federal Reserve.

US bank value-at-risk exceptions. Source: Risky Finance

Goldman Sachs suffered the most, experiencing two VaR exceptions of $153 million and $142 million, or $295 million in total. This is despite Goldman’s average daily trading revenue being $119 million during the 65-day time period, across equities and fixed income. Statistically, the only way to reconcile these figures is with a highly skewed distribution, that includes ten or more days of $200 million profits, and a few days of extreme losses when markets went haywire.

JP Morgan’s average daily trading revenue was $139 million, but that didn’t stop the bank from also experiencing a pair of VaR exceptions, losing a combined $188 million on two trading days during the quarter. This gives JP Morgan a slightly less riskier profile during the second quarter than Goldman Sachs, with 40 profitable trading days versus Goldman’s 33, according to the banks’ Fed filings.

Morgan Stanley had only 38 profitable trading days during the quarter, but it managed to scrape through with just one VaR exception, losing $87 million on a single day, while making $91 million per day on average.

Although Goldman lost more this quarter, JP Morgan’s third successive cluster of VaR breaches has exhausted the tolerance of the Federal Reserve, which has increased the bank’s capital multiplier to 3.5 as a penalty. By forcing JP Morgan hold more capital against market risk, the Fed may hope to rein in the bank’s risk-taking mentality.

Sources familiar with the banking giant downplay the Fed’s action, noting that the increased multiplier is automatically pre-determined by regulations based on the number of VaR exceptions in a 250-day period. Bankers argue that the increased VaR exceptions are a fact of life given the tariff-driven market volatility.

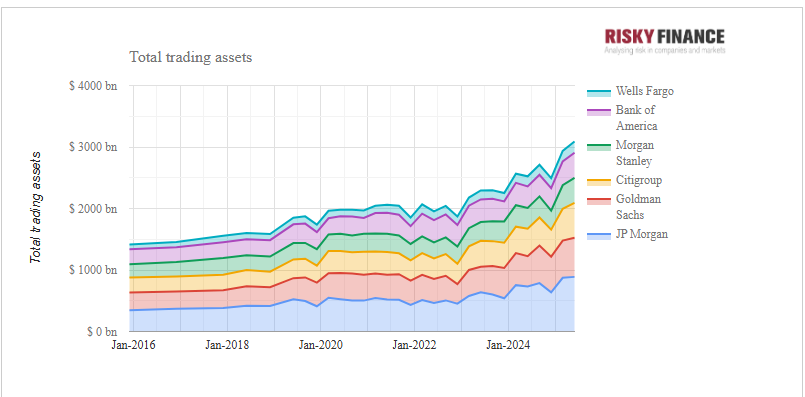

In any case, reducing risk may be easier said than done, since all six big US banks have increased trading book positions and derivatives exposures in order to drive profits. JP Morgan’s total trading assets hit a record high of $888 billion in June, followed by Goldman with $636 billion, while JP Morgan’s equity swap notionals approached $1 trillion for the first time, followed by Goldman and Morgan Stanley in joint second place.

Unwinding such eye-watering exposures may generate the same kind of trading book volatility that the Fed wants to see reduced. JP Morgan declined to comment.

Cantor Fitzgerald has hired seasoned financier Tony Nash as co-head of EMEA portfolio & electronic trading.

Nash joins from Stifel where he was managing director for electronic trading from 2019 to 2025.

His career spans managerial roles in electronic trading since the 1990s.

After starting in derivatives at Natwest from 1991 to 1997, he joined Deutsche Bank as a managing director in portfolio trading until 2005. He then took on a similar role at Lehman brother until the bank’s demise in 2008. He was partner at Execution Noble from 2008 to 2014, and also a partner at AutonomousRresearch from 2015 to 2019.

Since the appointment of Howard Lutnick as secretary of commerce, Cantor Fitzgerald partnership is co run by Pascal Bandelier, Sage Kelly and Christian Wall. As of 31 December 2024, the partnership had US$ 14.4 billion in total assets.

Announcing his new tenure, he was enthusiastic about the new position and its electronic trading suite that would soon offer an “upgraded Sonic dark algorithm”.

Everitt has more than 25 years of industry experience and joins the firm from Stifel Financial, where he has been managing director of electronic trading since 2011.

Prior to this, he was a senior equity trader at Seymour Pierce and FXCM.

Junya Umeno has joined OneChronos to lead the firm’s new Japan operations, effective September.

Alternative trading system (ATS) OneChronos was launched in 2022 and covers US equities. European, UK and Swiss equity and equity-like securities are expected to be made available this year. The firm also plans to introduce spot FX trading to its platform.

It is the 12th largest US ATS according to FINRA data.

Via LinkedIn, Umeno commented, “Japan’s financial markets are at an important turning point, and I believe OneChronos’s innovative approach can bring new opportunities for efficiency, fairness, and better liquidity access.”

Umeno has been a managing director at BlackRock in Japan since 2006, specialising in trading and market structure.

Tom Stilwell, client execution trader, Citadel Securities

Tom Stilwell has joined Citadel Securities as a client execution trader.

Based in London, Stilwell will cover US equities. The firm holds 23% of the US equity market share, according to a spokesperson.

He will also work on the expansion of Citadel Securities’ extended hours offering amid growing industry interest in 24-hour trading. Earlier this year, the firm requested that the SEC be more consistent in its rules for a 24-hour operating structure.

Issuers’ growing use of buybacks has drawn fresh scrutiny from the UK Financial Conduct Authority, which has concluded a multi-firm review of bank structuring, marketing and execution with no material concerns about outcomes or unmanaged conflicts. But an industry expert insists that the current system tilts advantages to the corporate bankers who perform the buybacks for issuers.

The FCA study covered 165 buybacks worth £40 billion executed by seven banks for FTSE 350 non-investment companies over 18 months; by comparison, FTSE 350 companies repurchased £78 billion over the same period. The FCA also notes buybacks have risen from 20% of shareholder distributions pre-COVID (2017–2019) to 42% in 2022–2024.

VWAP

The regulator distinguishes vanilla agency mandates from structured products, where fees are linked to “outperformance” versus a benchmark defined as the arithmetic average of daily VWAPs during the actual execution window. Benchmarks typically use continuous trading on the LSE and exclude auctions, reflecting Market Abuse Regulation (MAR) safe-harbour constraints. The FCA found structured buybacks represented 39% of transactions by number (45% by volume), that fee outcomes varied widely—including negative fees (rebates) in 30% of cases—and that, across four strategies, it found no statistically significant differences in average price outcomes.

This comforting message is disputed by ex-Goldman Sachs veteran Michael Seigne, founder of Candor Partners, which provides consulting services on buyback execution. Speaking to Global Trading, Seigne argues that the review “does not draw the right conclusions” and leaves “the goal open to misalignment, opacity, and avoidable cost.” He welcomes the work’s scope but says the findings reveal structural weaknesses that boards and regulators should not ignore.

“When the regulator’s own findings reveal how these products tilt the playing field, it’s right to ask who really benefits from the current design and whether issuers, their boards and investors are getting the whole picture,” Seigne says.

On volatility risk transfer, Seigne notes the FCA describes banks monetising volatility by varying participation and determining the buyback’s completion within contractual bounds, discretion that drives outperformance versus the benchmark. Seigne says that “a well-designed buyback execution strategy does not need to incorporate a volatility bet.” He contrasts structured buybacks with convertibles, arguing the latter are securities with prospectuses and listing safeguards, whereas “structured buybacks lack these protections.”

Seigne’s second concern is the design of variable “outperformance” fees. Because the fee is calculated after completion as the difference between the achieved price and the contracted benchmark, he argues it “functions economically as a retroactive change to purchase price,” pointing to the Companies Act 2006 requirement that shares be fully paid at purchase.

Third, Seigne challenges benchmark construction. The FCA acknowledges that the common benchmark is the average of daily VWAPs (equal shares per day). “If the purpose is to execute a value-based buyback, the suitable product is self-evidently the one with a benchmark that uses the correct maths,” Seigne says, framing it as a suitability question when banks both design the benchmark and control the calculation window.

Seigne also highlights constraints embedded in the UK market abuse regulation (MAR) safe harbour, which exclude certain liquidity sources and can extend durations. The FCA acknowledges features of the listing rules and MAR “could weaken the efficiency of an issuer’s buyback programme” and pledges to “consider this feedback” in future reviews.

“Safe harbours are intended to protect against market-abuse liability, not to lock in long-term inefficiencies in the cost of returning capital to shareholders,” Seigne says.

Finally, Seigne points to asymmetric economics and fee caps. “A fee cap is not automatic; they must be contractually negotiated,”. He argues banks can retain upside from outperformance while their downside is limited by structure.

The FCA concludes it saw no unmanaged conflicts and that enhanced issuer education and clearer option menus—fee caps, price/volume constraints, early-termination terms—would improve outcomes. Seigne agrees education is necessary but insists it is not sufficient: boards should interrogate volatility transfer, benchmark suitability, disclosure of post-trade fee effects and asymmetric payoffs before approving structured buybacks.

With just a handful of traders, Swedish pension fund AP2 leverages machine learning-based vendor technology to handle $25 billion annual equities turnover for its quant strategies

Working as a trader for a Swedish government pension fund might seem a recipe for lifelong career stability. But for Mathias Eriksson, senior trader equities and credits, trading at the country’s AP2 buffer fund, the situation is anything but. The government is in the midst of consolidating five buffer funds into three. While Eriksson can glean comfort from the fact that AP2 will survive, he can’t predict the final outcome.

If performance is a guide, Eriksson should have nothing to worry about. The Gothenburg-based US$48 billion fund reported a 8.2% net return in 2024, with an expense ratio of just 8 basis points. Of this, US$27 billion is invested in equities, which the fund manages using a quantitative dynamic asset allocation approach.

“The main part of our equity management is based on a quant model”, he says. “We have a large developed market mandate, that is about $8 billion of value. And we have an emerging market mandate, and the value of that is about four and a half billion dollars. And we have two domestic mandates as well, based on fundamental research”.

“The quant team are rebalancing or running the model on a scheduled basis. They do that every week, and the total turnover for the quant team is about $25 billion a year. From a turnover perspective, it’s huge. And, given that our trading desk has only three people, or four, if you add the FX trader, we need to be very streamlined. We need to have a lot of straight-through processing (STP). We need to have as much technical help as possible in order to handle this amount of trading”.

However, Eriksson cautions that trade-offs are involved. “Being a governmental pension fund, there is always cost pressure”, he says. “If everything was STP and automated, we could probably save transaction costs with help from technologies and from models. But we still think that human beings add value to the process”.

Moreover, Eriksson points out that AP2’s traders are less important than the investment team when it comes to the fund’s total performance. “We use technology to save parts of basis points when we are trading. But what is even more important is the investment strategy. We are talking of percentage points if we choose the wrong strategy. So that process is more manual in that sense that more people are working on it.”

Optimising quant signals

As a 20-year veteran of AP2, Eriksson understands his colleagues’ strategy well. “We use traditional quant factors, like momentum, value, quality and size”, he says. “We try to optimise the best blend of factors or signals for each specific region, on a continuous basis”.

“We have a huge library of different signals, of different factors that the quant team can use, at different points in time”, Eriksson continues. “Some factors are better than others, so we continuously evaluate which factors or signals are optimal. And that can differ from region to region, and it differs over time. We also have a liquidity model for creating the trades, and also a kind of TCA model to create trades that are liquid”.

And that is just the alpha side, since AP2 also determines asset allocation using its own custom benchmark. “We build our own benchmarks internally, on the beta side, trying to have optimal benchmarks compared to a strategic benchmark”, Eriksson explains. “On the equity side we use the MSCI universe, all the stocks within MSCI standard indices. Then we run an optimisation to define the starting weights after each quarterly MSCI index rebalance and send these to MSCI, to calculate the custom index on a daily basis”.

“For the Swedish population, the benchmark is actually much more important for their pensions, than each bet, or the alpha. The beta is what adds value. Of course, our goal is to beat the benchmark, so we aim to earn alpha as well. But the contribution to the P&L of the alpha is much lower than the contribution of the of the beta or the benchmark index selection”.

Only after all these multiple stages are carried out, the AP2 trading desk can see an actual order, Eriksson explains. “The quant team generate a list of orders, a list of trades which is imported into our trading system, into our EMS. When the trade hits the EMS, the trading team owns the trade. We own the P&L, while the underlying positions are owned by the quant team or by the equity team. From a pure P&L perspective it’s up to the trading team to decide strategy, to decide where to trade, and so on.”

Using AI for broker allocation

Using only regulated markets (AP2 doesn’t do any OTC equity trading), Eriksson’s team is heavily dependent on its favoured vendor, Virtu.

“We use Virtu, both for EMS, and also for TCA”, Eriksson says. “We do that because it’s very convenient for us when we trade, all the trading information is already in the EMS, and then it’s automatically fed into the TCA.. Whenever we have traded, we can immediately do a TCA analysis of what we have done”.

“If we’re looking at a developed market trade, for example, it’s between maybe 300-500 names or unique equities per trade. We can’t go into detail with every single order. And we need to decide which broker to use for each trade.”.

Allocation of trades to brokers is another area where AP2 is a heavy user of technology, this time with UK-based vendor BTON, using machine learning. “They have trained their model on our historical data, as well as other clients’ data”, Eriksson explains. “When we are going to trade, we upload the orders into our EMS, and the BTON algo wheel is built into our EMS. So we choose a strategy for the trades and send that off to BTON’s service. They run the evaluation and suggest a broker that optimal for that individual order, for that individual stock. With just one click, we then send the trade to the identified broker with a preset strategy. So, we define the strategy, and when it’s sent off to the broker, all the parameters are already set.”

“The trading strategy defines parameters such as what algorithm is the best to use? How should they treat the trade? Should it be internalised as trading on their own risk book? Trading lit or trading dark?

Significantly, as a government pension fund, AP2 is not subject to EU MiFID 2 regulations so is free to adopt a fully bundled research model.

“We are still bundled, which means that in order to get research, we need to allocate orders to each individual broker”, Eriksson explains. “We conduct a broker evaluation once a year, when we look at both trading performance, and the quality of the research that we get. “The broker review is based on the review for all asset classes, including derivatives, fixed income, FX, and equities. So all teams are involved in the evaluation.”

After that, we set a broker list, and the commission allocation for each individual broker. This is fed into BTON as well. And BTON’s tool has a memory – it knows whom we have traded with in the past, and keeps track of the commission allocation over time. At the beginning of the year, it doesn’t matter much if we allocate 100% of the trades to one broker, but the closer we get to year-end, the more important it is that we end up with a commission allocation close to our target.”

Stable execution

According to Eriksson, the new approach is popular with the sell-side. “Historically, we traded one week with one broker, the next week with another broker, trying to evenly spread out the commission allocation. We have six brokers on the broker list, so they got one week of orders every six weeks. Now, we have a closer connection with all the brokers. They get approximately the same number of orders, on a yearly basis, as they had before. But now they get orders every week. The brokers think that this setup is much better because we have a closer connection.”

This is particularly important when volatility increases, Eriksson continues. “It’s a fairer evaluation of the brokers as well. If it was a very volatile day when you got the trade, then the P&L might look bad compared to your competitors, even though it was just the volatility that created that. But now it’s the same volatility for all brokers that we are trading with every time. So it’s a fair comparison, in that sense.”

Mathias Eriksson.

“The spreads have come up a little bit this year, or pretty much so over a period of time. But despite that, we can see a more stable execution, even though the spreads are wider and given the situation in the world, the volatility has been higher as well. But we can still see a more stable execution – in other words, the variation of the P&L, is lower than we have seen in the past. That is a result of the BTON strategy and algo wheel.”

So far, AP2 has applied BTON to its development market portfolio but emerging markets are a work in progress. “The problem with emerging markets is that we don’t have as much data as we have for developed markets”, Eriksson explains. “We do not only evaluate the brokers, we evaluate BTON as well. Before adding it to emerging markets, we would like to do the evaluation to see that the algo wheel is working”.

“As for using non-traditional brokers, the scope for that is limited by AP2’s bundling policy”, Eriksson says. “We use execution only brokers as well. But that is used for a smaller portion of our execution. That’s because when we trade with them, we pay commission to a broker who we don’t get any research from.

Mathias Eriksson, in conversation with Virtu’s Rob Boardman at TradeTech 2025.

Meanwhile, AP2’s quant investing strategy is being broadened into derivatives. “We did a pretty big strategic change in March 2024 where we added a number of new mandates”, Eriksson notes. “Historically, almost all our mandates have been cash mandates so we haven’t been using derivatives to very large extent. But in this strategic overview, we added a number of derivatives-only mandates that take into consideration the size of the underlying cash holdings for collateral purposes. Now we can use that muscle on the derivative side, and are building up new mandates with derivatives exposure.”

Gurdeep Bumbra has joined Mirabaud Asset Management as a senior portfolio manager within the global equities franchise.

In the London-based role, Bumbra will lead the global focus equity strategy.

Andrew Lake, chief investment officer, commented, “His appointment reflects our focus on strengthening our core capabilities where we can add meaningful value for clients, particularly through concentrated, forward-looking strategies.”

As of year-end 2024, Mirabaud Group holds CHF 32.3 billion (US$40 billion) in assets under management.

Bumbra has more than two decades of industry experience and joins Mirabaud from Tourbilon Investment Management, where he has been a managing director for the past year.

The majority of Bumbra’s career has been spent at Pictet Asset Management as a senior investment manager for international equities.