Cross-asset trading is exactly what it sounds like: trading multiple asset classes to diversify a portfolio and better manage risk. With a single point of execution, the strategy has the potential to reduce operational costs and increase efficiency – but measures need to be taken before a team can get out of siloed structures.

Global Trading speaks to Andrew Etherington, head of multi-asset total return at AXA Investment Managers, and Antish Manna, principal quant and head of execution analytics for central trading at Man Group, about what it takes to run a cross-asset desk – and why the strategy is effective in a tumultuous landscape.

The year so far

In a string of unprecedented years, 2025 has provided its fair share of challenges so far. From tariff back-and-forth to global conflicts and rapidly-developing technology, both volatility and overall uncertainty have been front of mind.

Andrew Etherington, head of multi-asset total return, AXA Investment Managers.

“Momentum has been upended by policy uncertainty with bouts of intense intraday volatility which has left the appreciation of markets from a valuation perspective largely redundant. It’s been a helter skelter of a ride,” Etherington reported.

AXA IM’s multi-asset strategy covers equity, fixed income, currency and commodity assets.

“In terms of asset allocation, we had the peak of volatility in April. It’s come down across all asset classes, and that encourages the quantitative style systematic strategies to re-engage with risk. They’re reengaging slower than they sold off, and that’s because they need past volatility to wash out of their data set.”

Etherington highlighted the changing role of central banks, noting that many in the industry have not worked during a time when central banks were not taking a ‘hand-holding’ approach.

“In fixed income, there’s a steepening trend on global yield curves. Central banks have been stepping back from intense forward guidance.”

During times of stress and change, agility is crucial; and that’s where cross-asset strategies can come in.

“You need things under the hood for when things inevitably go wrong,” Etherington stated at TradeTech in Paris earlier this year. The benefits of diversification are increasingly apparent, and for traders working in a climate they’re not used to, being prepared is key.

Structure

One of the most important things for cross-asset desks to succeed is also one of the simplest: having everyone in the same place.

“I’ve been in places before in my career where the fixed income desk would be on a

Antish Manna, principal quant and head of execution analytics for central trading, Man Group.

different floor from equities, with very little to no interaction. Different toolkit, different philosophies on how you approach the market and trade. It’s a missed opportunity,” explains Manna.

At Man Group, traders of all disciplines sit together – across asset classes and across strategies.

“We have high-touch traders covering markets where there’s little or no electronification and automation, then we have quant traders and researchers looking at the systematic side of the business and optimising our algos,” Manna illustrated.

“It’s beneficial for people to sit together. We centralised trading in 2018, we’re in the seventh year of being one team, one unit servicing the whole of Man Group without silos.”

Beyond physical structures, cross-asset trading desks also allow people to spread insights and learnings across asset classes.

Having the team all in one place allows for operations to improve more quickly, Manna continued. One those on the strategic side of the business have optimised the operations of the market they’re covering as much as possible they’ll jump onto another project, bringing their learnings with them.

“That lets us reallocate resources to make maximum return on investment,” he said.

“There will be areas where you can reach an optimisation plateau, but you can reuse the same transferable skill set – of understanding markets, modelling cost, automation, algo optimisation – in other markets where the opportunities are still untapped.

“Sometimes when people are only looking at one market, they’re limited as to what they view as possible. A side effect of having people move around is that they start to see things in common across the business, often augmenting what they then see as possible.”

Speaking the same language

Key to enabling this is having a shared, standardised language and toolkits, which allows traders to move between disciplines without having to learn new ways of operating.

“That’s one reason why our team is very fluid in terms of people’s ability to pick up new asset classes. If you have a really good understanding of venue toxicity, you can apply that from one asset class to another without having to relearn things, but at the same time doing so without diluting our very laser focused way of dealing with specific markets in specific ways,” Manna said.

“In periods of market stress, it is equally useful to know where you don’t have to focus,” he noted. “Without a strong communications and operations framework across the board, critical information and insights can be lost, dampening the overall confidence in the process. You want simple, clear, and data-backed insights.”

Challenges between asset classes

Jumping from one asset class to another isn’t always easy, though, no matter how well-aligned operations are. Some markets are more liquid, some are more electronic, regulation is lagging in some and information is harder to come by in others.

On the liquidity side, Etherington emphasises AXA IM’s focus on remaining nimble when juggling various asset types.

“Our clients require daily liquidity, so all our assets could be liquidated in a couple of sessions. We have to be careful that we’re able to get in and out,” he says.

“In a futures market, it’s not always sufficiently liquid to do that comfortably, especially in a time of stress. Even with listed options, when the market takes a significant shift higher in stress, bid offers go out and a lot of the profit and loss that you would have expected to be able to realise disappears. You have to be conscious of that – you can’t rush into every instrument.”

This requires a level of specialism from cross-asset teams, alongside their ability to cover multiple instrument types concurrently. That’s where high-touch traders come in, Manna says, explaining how Man balances specialism and generalism.

“High-touch traders usually have a business or type of business that they’re servicing. They have a really rich understanding of their PMs’ intentions and the names and markets they are in every day.”

Discrepancies between asset classes don’t stop at the point of execution; they need to be taken into consideration during trade cost analysis (TCA) too.

“TCA works differently across asset classes because the underlying asset classes trade differently. When you try to pull it all together, you realise that you’re measuring different things, and there’s a question mark over what you’re going to end up with,” commented Matt Howell, global head of trading strategy at T Rowe Price, at TradeTech this year.

“It’s becoming increasingly important as different asset classes bleed into each other.”

Ash Sharma, global trading analytics manager at Aviva Investors, explained at the event that TCA is still siloes at his firm. “We’re hopefully moving to the stage where we’ll be able to look at all the costs associated with each of the asset classes within a fund, in terms of the instruments that are traded,” he said. “There are always ways to refine the analytics that you’re looking at, whether they’re in-house or outsourced.”

Both AXA IM and Man Group declined to share the names of service providers used by their cross-asset desks.

It’s unlikely that high levels of volatility and uncertainty will come down any time soon. While specialist knowledge is still a valued part of the trading environment, the flexibility and agility that generalist traders – and those willing to break out of their silos – can provide are increasingly in demand as the industry, and the challenges it faces, evolve.

The equity issuance rules overhaul raise the prospectus waiver threshold to 75%, halves initial public offering (IPO) waiting times to three days and launch a new public offer platform (POP) to promote large crowdfunding like private issuance.

These changes closely mirror the proposed listing regime change contained in the July 2024 consultations.

The changes aim to boost UK public markets amidst a year where UK equity issuance has all but disappeared and a year after these changes were first proposed.

So far this year the UK represents only 0.8% of worldwide primary issuance at US$1.1 billion and just 5% of the secondary market at US$13.9 billion.

The FCA reform aims to invigorate the UK equity market. Companies already listed can now issue up to 75% of their existing share capital without needing a full prospectus rather than the previous 20% threshold. The FCA projects it will deliver annual savings of £40 million.

The waiting period between prospectus publication and IPO execution has also been reduced from six to three days to improved access and responsiveness for retail investors.

Finally, a newly launched public offer platform (POP) allows private firms to raise £5 million or more via authorised intermediaries without undergoing full prospectus obligations, effectively scaling crowdfunding mechanisms for larger offerings.

Based in London, he specialises in UK, Europe and MENA sales.

Revenue at Marex was up 28% in Q1 2025, reaching a reported US$239.5 million.

Eryuksel led business development at UBS’s outsourced trading division from 2023, before which he was director of global emerging markets sales trading and head of equity trading at the firm.

Earlier in his more than 25-year career, Eryuksel held senior roles at Turkish capital market brokerage firm Global Menkul Değerler including director of institutional sales trading and country manager for Egypt and Azerbaijan.

Eryuksel’s appointment is part of Marex’s broader expansion in the MENA region, with Charlie Monson joining the outsourced trading team in Dubai last month. Monsoon was previously a senior broker and director of equity derivatives at the firm.

Joseph Nehorai, global head of futures and options execution sales, Goldman Sachs

As exchanges compete with one another through rival products, their efforts can increase liquidity fragmentation for their users. With the same derivatives contracts being listed in multiple locations, market participants must decide where they want to trade – adding another layer of decision-making to the process.

At the International Derivatives Expo (IDX) conference in London last month, Joseph Nehorai, global head of futures and options execution sales at Goldman Sachs, explained that many clients are likely to choose the exchanges they trade contracts on based on where they already operate.

“Because of the increased use of futures across every asset class in every region, they want to maximise their leverage through optimising their margin,” he said. “[That might be] posting different types of collateral, or forcing prime brokers to provide margin offsets within their own risk models, or choosing to execute the future on an exchange where they have an existing position around the future that gives them a correlated margin offset – choosing ICE or Eurex to trade an MSCI future because they have an existing equities index future exposure in another product, for example.”

ICE, the predominant MSCI futures exchange, offers 161 MSCI futures products to Eurex’s 146. Not satisfied with European dominance, Eurex is challenging the American exchange by launching futures on the MSCI Korea Net Total Return Index.

While Korea has the fourth largest presence in the MSCI Emerging Markets Index, representing 10.73% of the pie, Eurex is the only non-Korean derivatives exchange to provide access to a Korean equity index.

A previous clearing link between Eurex and the Korea Exchange (KRX) angled towards retail investors and market markets was decommissioned effective 5 June this year, following an expansion of KRX’s trading hours.

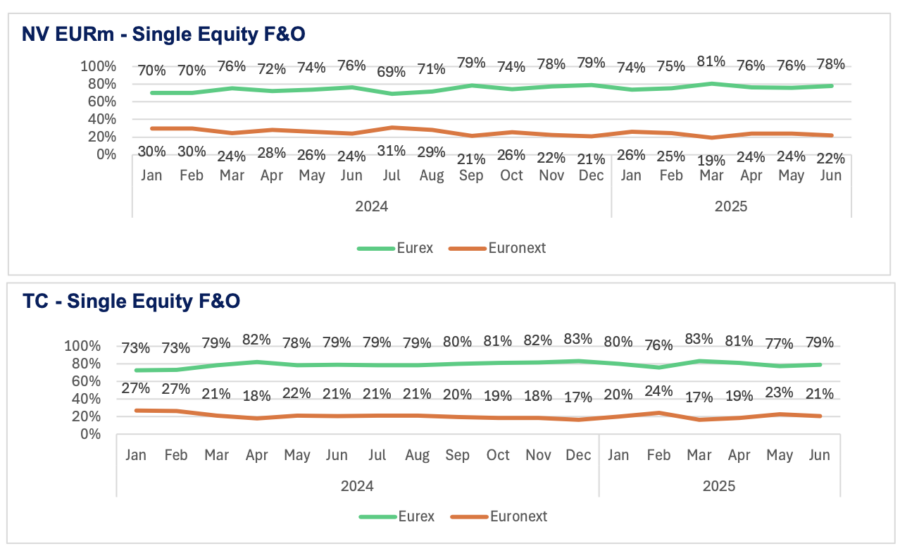

Back on home turf in Europe, rival exchange Euronext has not managed to budge Eurex’s market share in 2025 – despite numerous efforts to encroach on the incumbent’s territory. In fact, its overall market share has declined since January, both in terms of notional volumes and contracts traded.

In June, 9 million contracts were traded on Euronext and 81.8 million on Eurex.

Speaking to Global Trading, Charlotte Alliot, head of financial derivatives at the group, pointed out, “Comparing the market share of Euronext and Eurex doesn’t make sense on some asset classes. For example on equity indices, the underlyings are different – CAC 40 is different from the DAX or the Euro Stoxx, for example. We do not sell the same thing.”

Where they do sell the same thing, however, is in single stock futures and options – which is also where the only bump of note for Euronext took place, at the start of the year.

Single equity futures and options, notional volume and contracts traded

The group’s market share by notional value jumped up five percentage points to 26% in the first month of 2025 for this category, and took 24% of the market by contracts traded in February. This was short-lived, though, falling back to 19% by volume and 17% by contracts traded in March despite much higher trading activity across the board.

Eurex offers 905 single stock futures, while Euronext provides access to 562.

Alliot argued that Euronext is doing better than it seems on a consolidated basis.

“On single equities, Euronext market share is quite strong. In Q2 2025 it’s above 70% in Italy, 80% in the Netherlands and above 50% in France. France is a more challenging market, but things are improving on our side. This is due to the creation of the liquidity pool of Euronext Clearing which led to the repatriation of market share from some members,” she said.

Euronext’s launch of mini German single stock options in June, following French and Dutch equivalents in April, was characterised as “an attack on Eurex” by Alliot earlier this year. By offering a product that Eurex does not, the exchange aims to claw back market share.

Updating Global Trading, Alliot stated, “Our mini options on Dutch, French and German underlying are doing very well. They have nearly 100k lots traded.”

While the impact of the German offering remains to be seen, the earlier launches did not take the group above the market share highs of February.

There has been an overall decline in notional volumes in single stock futures and options since March – falling from €224.6 billion to €149 billion over three months. However, US uncertainty and related high trading activity have driven up volumes YoY in H1, rising 19% to €1 trillion.

Year-on-year (YoY), Euronext’s overall market share has remained static in contracts traded and declined by one percentage point in overall volumes.

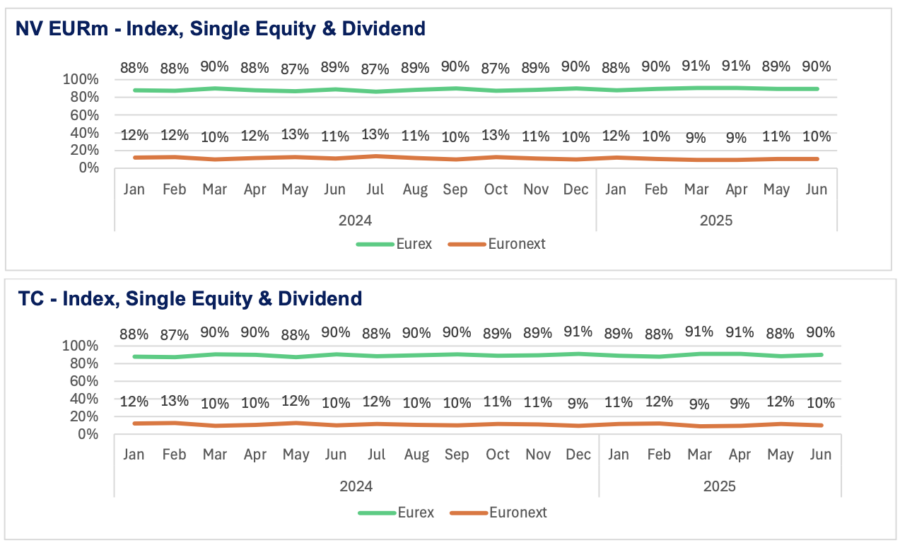

Index, single equity and dividend futures and options notional volume and contracts traded

In index futures and options notional volumes, Euronext has broken through the 10% market share barrier just once this year, taking 11% of the pie in January. By contracts traded, its share has hovered between 5% and 6% since last November.

Across dividend futures and options, Eurex has continued its long-standing domination with between 99% and 100% of the market share.

There has been a marked decline in overall activity for the two groups YoY, falling by 38% to 90 billion contacts traded and by 30% to €3.6 trillion in notional volume in June 2025.

Isabelle Scemama, head of alternatives divisions, BNP Paribas Asset Management

News of the leadership structure for BNP Paribas and Axa Investment Management’s massive merger is trickling in, with the latest announcement seeing responsibilities divided up for alternatives and liquid investments.

The merger, completed at the start of July, resulted in a €1.5 trillion assets under management asset management business.

AXA IM stated that there have been no portfolio manager departures from its team following the acquisition.

Isabelle Scemama will lead the company’s €300 billion AUM alternatives divisions, expanding her role from global head of AXA IM Alts to cover AXA IM Prime, BNP Paribas REIM and BNP Paribas Asset Management (BNPP AM) Private Assets.

Rob Gambi, global head of investments at BNPP AM, will also lead liquid investment capabilities across both AXA IM Core and BNPP AM. Liquid strategies at the new firm now hold more than €1,000 billion AUM, around €700 billion of which sits in active fixed income, including money market funds. A further €40 billion is held in exchange-traded funds.

Scemama has been with AXA IM for more than two decades, having held her current role for over five years. Prior to this, she was CEO of real assets at the firm and head of corporate finance for real assets at AXA’s real estate business.

Six of Gambi’s 40 years in the industry have been spent with BNPP AM. Before this, he was chief investment officer at Henderson Global Advisors and global head of fixed income at UBS Global Asset Management.

Natixis IM: Growing concerns over stubborn inflation, Fed leadership, and the threat of currency wars

While US and European markets have largely recovered from the latest round of tariff announcements and delays rolled out this July, Mabrouk Chetouane at Natixis Investment Managers, warns of key risks ahead. The head of market strategy shares his views on persistent US inflation and the impact on Federal Reserve cuts this year, he talks uncertainty over the Fed’s leadership, and discusses the threat of currency wars and the wider implications this could have on outflows, hedging costs, and market volatility.

Chetouane also unpacks how his team calculates volatility and adapts his investment models in unpredictable markets using Markov techniques and inputting monetary policy factors.

Jane Street is accused by India’s securities regulator, SEBI, of allegedly employing its “immense trading, financial and technological prowess” to realise outsized profits in India’s derivatives market.

The detailed interim order from SEBI, covers trading activity from January 2023 to March 2025. It gives a vivid account of how Jane Street exploited the different liquidity profiles and intricate relationship between index options, futures, and underlying stocks.

At the heart SEBI’s allegations is its analysis, and supporting documents, of Jane Street’s trading activity

Its analysis for two specific days, 17 January 2024 and 10 July 2024, indicate the gigantic trading, risk and profits Jane Street’s traders put on, and extracted from, the retail heavy market.

On 17 January 2024. Jane Street opened the day aggressively purchasing shares and futures contracts of the twelve constituent stocks of the BANKNIFTY index.

SEBI says Jane Street bought US$500 million of stocks and futures, and by pushing up the stocks and future prices, inflated the index from its opening at 46,573.95 to a morning high of 47,176.97. SEBI’s granular trade-level analysis indicates that Jane Street’s purchases significantly influenced upward price movement, even as broader market sentiment remained bearish.

Janes street trading in Bank NIFTY stocks, futures and derivatives, 17 January 2024, SEBI analysis

Simultaneously, as prices climbed, Jane Street allegedly began taking substantial bearish positions through index options, by selling large amounts of call options and buying put options at prices made advantageous by the artificially inflated index level. By midday, Jane Street’s net delta exposure had shifted to an enormous net short position of US$4.5 billion.

SEBI estimated that on that day, the Indian options market in that banking index to be ninety-eight times larger than the cash market on which settlement prices are nevertheless based.

Alex Gerko, CEO of XTX, a rival electronic market maker, estimated on a post of LinkedIn that a US$200 million imbalance would have a market impact superior to 0.4% on index prices.

Later that same day, Jane Street unwound its early long delta one positions in the index components’ stocks and related futures. After 11:47 AM, the firm sold its morning purchases, rapidly unloading US$618 million worth of accumulated shares and futures, which SEBI says exerted significant downward pressure on the index. The index, responding to this massive sell-off, declined sharply, ending the day near 46,064.45.

By the close Jane Street’ traders were up US$84.5 million on what they say was an index arbitrage.

SEBI’s investigation further highlights that this strategy was not isolated. It identifies 15 days between January 2023 and March 2025, primarily on options expiry days, when Jane Street allegedly repeated variations of this pattern. On these occasions, the firm would first push the index upward or downward through aggressive cash and futures trading, subsequently positioning itself in index options to benefit from reversing market moves, according to the regulator These alleged manoeuvres yielded cumulative index options profits of US$450 million.

Jane Street contends that its trades constituted legitimate arbitrage activities aimed at maintaining market efficiency. However, SEBI strongly contests this claim, asserting that such trading patterns clearly manipulated the market, adversely impacting numerous retail investors.

Famed and successful traders have long debated the boundary between legitimate strategy and market manipulation.

Alex Gerko proposes a litmus test for such market manipulation: “How to tell if your strategy is likely legit Vs something that will result in SEBI sending you a 100-page pdf: imagine reducing all sizes in your strategy by a factor of a 100. If it works better than before (per unit of risk/in terms of margins) then it looks legit. If it stops working altogether after scaling down then question your life choices.”

The interbank market in MSCI Emerging Markets derivatives that five years ago was 98% swaps is now 98% futures, according to Goldman Sachs. But the buyside still remains swayed by the advantages of OTC contracts.

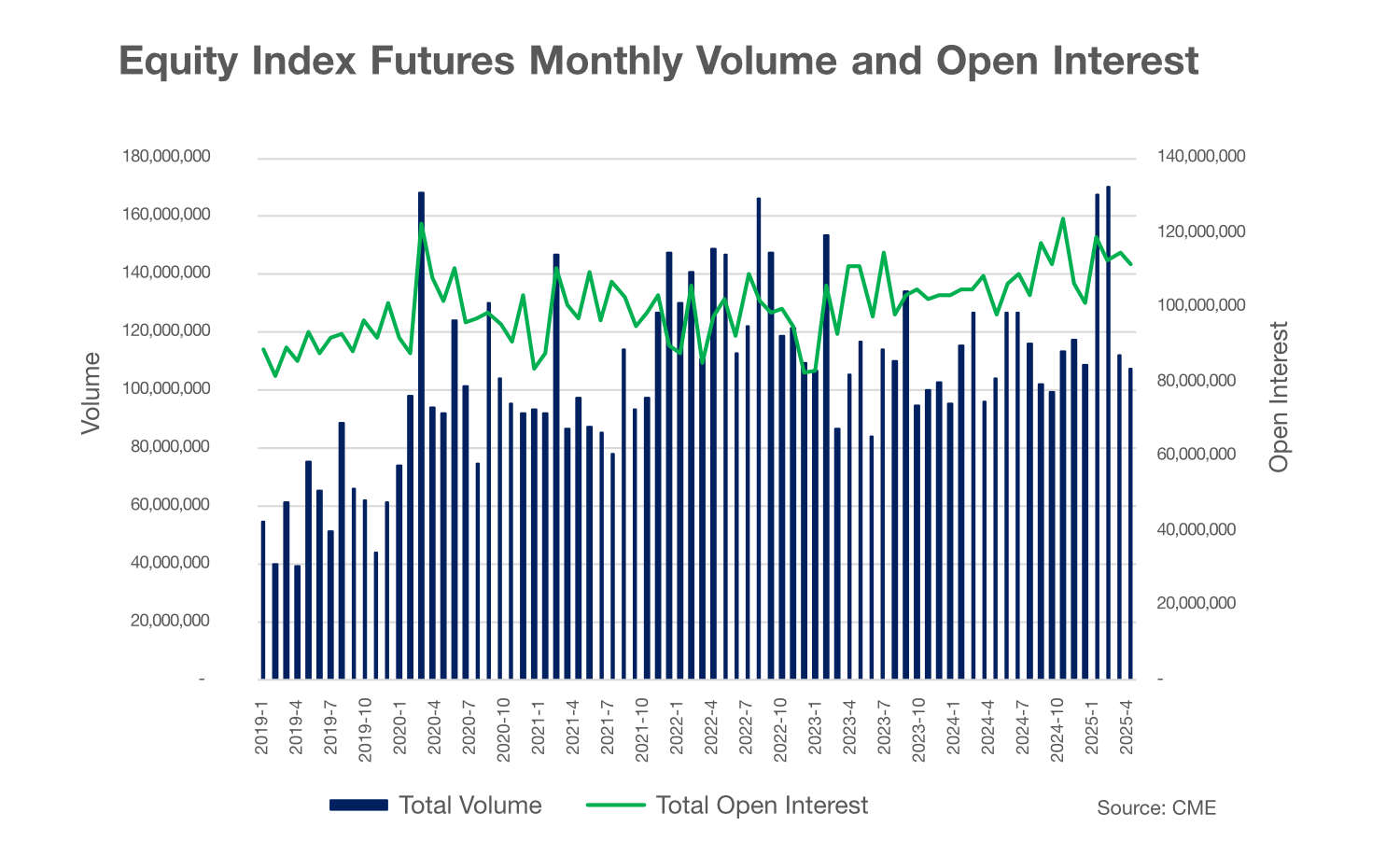

Listed equity derivatives are booming. In April, volume in US equity futures contracts reached an all-time high, according to CME. Similar records were broken in listed equity options as well. European equity derivatives volumes peaked in March, according to data compiled by Eurex.

Buyside firms have also increased their derivatives activity.

Matt Howell, T.RowePrice.

According to Matt Howell, global head of trading strategy at T Rowe Price, “Our derivative use continues to grow, and it’s growing in terms of the strategies that are using derivatives. It’s growing in notional volumes, and it’s growing in the variety of different instruments that we are trading”.

Axa Investment Managers is already well-known to Global Trading readers for its use of tail risk hedging.

This year, derivatives usage has risen further, according to the firm’s senior derivatives trader Dimitri Mongeot. “We have been pretty active since the beginning of the year, so we did increase our volume significantly with the volatile environment. When there is volatility, we try to be a bit more tactical as banks do.”

All this increased activity comes amid claims by sell-side firms and exchanges that the tide is beginning to turn away from OTC derivatives, and in favour of listed products. The buzzword is ‘futurisation’, where structures that in the past would have traded in swap format are being refashioned as listed products.

Joseph Nehorai, Goldman Sachs.

“It’s a fundamental shift in our markets and how they’re perceived and how they’re utilized”, according to Joseph Nehorai, co-head of global futures at Goldman Sachs, speaking at the FIA’s IDX conference in London in June.

“I see futurisation actually being an incredibly important part of the growth in listed derivatives, as people migrate away from trading swaps,” he said. “The interbank market in MSCI Emerging Markets, five years ago, that was 98% swaps, now it’s 98% futures. The Eurostoxx total return future has a higher open interest than the classic Eurostoxx future, and that’s all interbank hedging”.

Exchanges can take some credit for this growth.

Alessandro Romani, Nasdaq.

“Europe has been showing leadership when it comes to moving from OTC to listed with the introduction some years ago of total return futures on established indices as an alternative to the use of equity swaps”, Nasdaq’s head of European equity derivatives products Alessandro Romani told the TradeTech audience. “What we are able to offer today to clients that are trading OTC, is the possibility to create their own custom baskets based on the universe of over 1200 stocks covered in Europe and US, and have a futures contract that is listed on exchange and centrally cleared on the very next day as an alternative to using OTC equity swaps”.

Bilateral derivatives are ‘good tools’ However, large buyside institutions in Europe do not seem to have received this sell-side memo. Instead, they respond with complaints about fragmentation between exchanges and lack of on-screen liquidity. Axa IM’s Mongeot makes his firm’s preference for OTC derivatives clear.

“We are significant users of OTC products”, Mongeot told the TradeTech audience. “People talk about fragmentation, but to be a bit of a contrarian, for OTC products, as an asset manager, we don’t feel the issue of fragmentation, because we can get large sizes done on the OTC market. OTC bilateral products are good tools to transfer risk without being visible in the market”.

Trying to assess any buyside trends in derivatives use can be a daunting task, however, because of the sheer variety of the portfolios involved and their investment goals.

“Derivatives are another tool in the toolbox for lots of different strategies that have different objectives”, notes Howell. “If you think about what derivatives can bring to a portfolio, there’s hedging, or removing an exposure from an existing investment. There’s directional, where you’re looking to add an exposure via a derivative, and often embedded in the derivative is some form of leverage. And then there is liquidity which the derivative allows you to access in a way that you’re not able to access directly in the underlying”.

Choosing the right kind of derivative involves understanding portfolio manager objectives, Howell explains.

“The implementation discussion, which is what my team spends a lot of time doing, involves understanding the exposure, the investment time horizon, the strategy that they’re running, and then coming up with the cleanest, operationally-supported implementation suggestions, backed by data, coherent with the wrapper that’s being used, and liquidity is obviously a big factor”.

“The reason you’d use a particular instrument is dictated by the combination of investment objectives, strategy that it is residing in and the fund wrapper.”

Howell is reluctant to publicly describe T Rowe Price’s mix of derivatives, but in the one case where Howell does express a preference for OTC products, he explains that for buyside institutions, bilateral contracts overcome the drawbacks of listed products when trading options in Europe. The problems stem from multiple exchanges offering the same contracts on-screen, each with multiple strikes and maturities with limited liquidity. Institutions that need to trade larger size off-book are frustrated by block trade crossing rules that vary between different exchanges.

“I’ve been working for US firms transacting European business across derivatives for many years, and often our challenges accessing listed option markets have been because the lack of on-screen volume, because of rules around crossing blocks, etc, and that’s always been difficult to interact with and we’ve often fallen back on OTC because it’s easier”, Howell says.

Collateral convenience Being able to trade in size is not the only reason that many buyside traders favour OTC.

“It does have another advantage for us”, says Mongeot. “When we do these trades for institutional clients, from a collateral perspective, you can post [investible] assets you have on your balance sheet against it”.

This flexibility contrasts with listed derivatives, where exchanges require cash in order to meet margin calls – often a scarce resource for buyside firms.

“OTC products are governed by a credit support annex (CSA) that is negotiated bilaterally and optimized to the need of each account, giving the client the freedom of a bespoke collateralization in opposition to listed products that are subject to daily margin calls in cash”, Mongeot told Global Trading.

However, this flexibility is less important for fund managers that ringfence their funds.

“All of our strategies and funds have their own legal entity identifier (LEI)”, one such buyside trader told Global Trading. “We trade as an advisor across all of those entities. What we can’t do is use positions in one legal entity to support positions in another legal entity”.

“If you’re trading for one LEI that’s running lots of strategies, then collateral becomes much easier. This is why large hedge funds can often implement new strategies faster. It’s because they’re not dealing with onboarding 400 separate agreements just in order to enable the platform to trade”.

For Howell, collateral is ultimately determined by the underlying fund, which often determines the type of derivative used.

“You’ve got this exposure you want to take, and you’ve got the strategy it operates within – if you’re talking about an equity strategy, then you’re not going to be a natural holder of bond collateral,” he says. “But if you’re executing in a fixed income strategy, you’re probably holding Treasury bonds, which you might want to use as collateral, rather than posting cash. That asset class strategy would help you decide whether you’re going to trade bilateral or whether you can trade listed”.

And some fund management clients might not even be able to trade OTC derivatives at all.

“We might have a situation where we’ve got a client who doesn’t have ISDA agreements”, Howell points out. “An exchange traded derivative makes more sense for that client than a bilateral product”.

Transatlantic differences For all the talk of record listed equity derivatives volumes, growth is still dominated by the US. In Europe, Frankfurt-based Eurex may have seen record volumes in March, driven by its benchmark Eurostoxx contracts, at a time when uncertainty over US policy was at its peak. However, Paris-based rival Euronext reported equity derivatives volumes that were actually lower than the previous record in July 2024, despite a flurry of recent derivative product launches aimed at prompting new business.

Market participants highlight the difference between the freewheeling culture of the US versus Europe, where market counterparties are more risk averse and counterparties expect options to be packaged together with their underlying hedge, which reduces risk.

“Talking about trading style, it’s completely different between the US and Europe,” Axa IM’s Mongeot explains. “In Europe you will trade options against the delta, and you need to actually hedge the delta, whereas in the US you don’t”.

By contrast, US markets have liquidity providers happy to take the opposing side of an option trade without any hedge in place, Mongeot says.

“The US structurally has bigger volume, which creates a dynamic where, when you trade with a liquidity provider, a bank, or newcomers in the market, they take the opposite side of your trade. You don’t have that at all in Europe, which I think is one of the main reasons you have a lot of engagement in the US market”.

One reason for this difference is retail use of options in America, which has sparked a craze for zero-date-to-expiry (0DTE) contracts facilitated by online zero-commission broker platforms. According to CBOE, 61% of S&P 500 options volume in May was 0DTE, driven by retail. If exchanges want to transform equity derivatives in Europe, retail needs to be involved, insists Mongeot.

“Retail participation is much lower in Europe than it is in the US, and something needs to be done,” he says. “Now in the US, 0DTE equity options is actually 50 to 60% of the volume, and it’s nowhere in Europe”.

Mongeot believes that 0DTE has improved liquidity across the entire US options market.

“It just shows that if you have traction in these options at the front end of the curve, you might have it propagating towards the other end of the curve as well, and probably more trading volume overall,” he says.

There are some encouraging signs in Europe, such as from the Nordic region. “We have seen strong growth in retail participation from the domestic client base”, Nasdaq’s Romani told the TradeTech audience. “The retail flow from online brokers serving the local market has been growing 40% over the past five years”.

European exchanges should also learn to be less tight-fisted when it comes to fees and data feeds, according to Iouri Saroukhanov, head of European derivatives at CBOE.

Iouri Saroukhanov, head of European derivatives, Cboe Europe.

“[The industry] can start being more generous with our data that we give to the retail participants. We [CBOE] offer it for free. We are committed to that. I’m sure there’s other ways of doing zero-fee retail broking. That’s what actually allowed retail to spring up in the US. So, let’s have a look at some of the lessons from across the pond.”

Others warn that retail growth in Europe will have to wait for an easing of over-coddling regulation and the development of a risk culture, moves which have only just begun.

De-fragmenting European listed derivatives In the meantime, industry participants urge getting to grips with the perennial bugbear of fragmentation. This can mean a number of things, from multiple exchanges offering the same contracts which have low levels of liquidity, and the lack of interoperability between Europe’s numerous clearing houses.

Charlotte Alliot, Euronext.

Charlotte Alliot, head of financial derivatives at Euronext questioned the framing of the debate in her comments at TradeTech. “The issue is not fragmentation, it’s culture. Because if you look in Germany or France, they do structured products rather than options. When you go to Holland, the minister used to be an options trader. Everyone does options, and it’s fantastic. And if you go to Italy, they love fixed income, and they like futures.”

Meanwhile, CBOE Europe, which is not competing against European listing exchanges with new contracts [in the equity space], focuses on the clearing problem. CBOE’s Saroukhanov told the TradeTech audience, “Fragmentation comes up a lot, and we’re offering pan-European access and also pan-European clearing as well. When you start talking about equity options and the multiple central securities depositories (CSDs) that we have in Europe, it’s hugely important to be able to offset options against equity flows and here, clearing is extremely important”.

According to the sell-side, fragmentation is no longer an obstacle. “The level of sophistication from our clients has gone up”, Goldman’s Nehorai told the IDX audience. “Because of the increased use of futures across every asset class in every region, they want to maximize their leverage through optimizing their margin, whether that’s posting different types of collateral or forcing prime brokers to provide margin offsets within their own risk models, or choosing to execute the future, or give an exchange where they have an existing position around the future that gives them a correlated margin offset”.

Yet the public numbers still fail to support such assertions. Even Goldman’s own quarterly Federal Reserve disclosures show the firm’s equity futures positions lagging well behind OTC equity derivatives notionals. Exchange derivatives volumes are still dominated by their biggest index products rather than new contracts. When it comes to futurisation, the jury is still out.

Joseph Lee, APAC head of high touch sales trading, Barclays

Joseph Lee has joined Barclays as head of high touch sales trading for the APAC region.

Based in Hong Kong, he reports to Christian Treuer, APAC head of equities distribution, and Peter Ramsey, global head of cash equities.

Lee’s appointment marks Barclays’ push into high-touch execution in the region, offering an alternative to its existing program and electronic trading capabilities.

The firm stated, “This appointment reflects Barclays’ long-term commitment to its APAC equities business and its focus on building a differentiated platform that delivers stronger execution, deeper client partnerships, and sustainable growth.”

In global markets, Barclays’ equities income was up 38% quarter-on-quarter to £963 million in the first three months of the year. Year-on-year, this marked an 8% increase.

The announcement is the latest in a string of appointments on Barclays’ APAC equities team, with Paul Johnson named head of equities for the region in January.

In May, Avinash Thakur was promoted to head of the APAC investment banking division. Changes were also made to leadership in the overall region, India, and Australia.

Lee has three decades of industry experience and joins Barclays from HSBC, where he was head of block liquidity in Hong Kong. Prior to this, he held roles including head of Korea equities and APAC high touch execution at Credit Suisse and worked at firms including Deutsche Bank and Goldman Sachs.

")

Listed equity derivatives are booming. In April, volume in US equity futures contracts reached an all-time high, according to CME. Similar records were broken in listed equity options as well. European equity derivatives volumes peaked in March, according to data compiled by Eurex.

Listed equity derivatives are booming. In April, volume in US equity futures contracts reached an all-time high, according to CME. Similar records were broken in listed equity options as well. European equity derivatives volumes peaked in March, according to data compiled by Eurex.