Philip Macartney and Mark Heslop, ex-Jupiter Asset Management

Portfolio managers Philip Macartney and Mark Heslop have left Jupiter Asset Management as the company shutters their European Smaller Companies Fund.

Macartney has been at Jupiter Asset Management since late 2020, and Heslop since late 2019. The pair both joined Jupiter from Columbia Threadneedle Investments.

Earlier in his career, Macartney was an analyst at Bramshott Capital, Moore Capital Management and Columbia Threadneedle Investments. He has now joined Invesco as a deputy fund manager, on a temporary basis.

Heslop has not announced his next steps. Before Columbia Threadneedle, where he spent more than a decade, he was an equity analyst at Citi.

Another Jupiter alum, Spencer Copp, recently joined Jefferies as an equity trader. He was a senior dealer at Jupiter between 2020 and 2024, a role he also held at Merian Global Investors and Old Mutual Global Investors. Earlier in his career, Copp was an executive director at Goldman Sachs and a senior programme trader at ITG.

Seilern investment, with US$ 2.5 billion under management, has promoted John Grand to head of trading.

After six years at the firm as a equity trader, he has been internally promoted. He started his career at J O Hambro in operations before moving to Barings investment management as a equity trader.

Gaelle Jarrousse Ducomble has joined Goldman Sachs in London as Executive Director in FIG Specialist Sales, moving from Kepler Cheuvreux, where she held a similar role for nearly eight years.

Jarrousse Ducomble specializes in covering the banking sector.

Prior to Kepler, she held senior specialist sales roles at Macquarie Group, Mediobanca, and Morgan Stanley.

She holds a Master of Science in Finance (Magistère BFA) from Université Paris Dauphine.

ESMA is attempting to address the downward spiral in liquidity of smaller-cap European stocks. The challenge: fund managers expect research coverage before they invest, but coverage dried up post-MiFID. One solution is to combine payment for research with execution, but for some unloved companies, the issuers themselves must pay to be covered.

Issuer-sponsored research (ISR) is financial analysis commissioned and directly funded by issuers themselves, particularly smaller firms that lack sufficient independent analyst coverage. Post-MiFID II regulation, the requirement for asset managers to separate payments for execution and research (the ‘unbundling’ regime) caused a dramatic reduction in coverage of smaller European companies, exacerbating liquidity problems. In a related consultation on MiFID II research provisions dated 28 October 2024, ESMA acknowledged that allowing joint payments for research and execution services could revitalise research coverage but recognised the need for clear guidelines to manage conflicts of interest and ensure transparency.

In this context, ESMA’s recent consultation specifically on ISR proposes adapting the French Charter—a structured code of conduct outlining conditions for ISR—to the broader EU market, naming this approach “Option 3”. Option 3 aims to ensure ISR transparency, reduce conflicts of interest, and standardise contractual terms, remuneration structures, and disclosure requirements across Europe.

AlphaValue, a French independent research provider, underscored the issues with traditional research models in its answers to the consultation: “While the problem always existed, it has become worse over the past few years with the rising share of passive investing (doesn’t pay for research) and the flows out of small and mid-cap funds towards large caps. The available wallet for Small and mid-cap research is simply too small.” AlphaValue concluded “having sponsored research is better than no research.”

However, German respondents uniformly rejected ESMA’s preferred Option 3, strongly advocating for maintaining their national standards and contractual freedom. The German Association of Investment Professionals (DVFA) opposed additional EU-wide regulations: “We do not consider the introduction of a code of conduct expedient, especially as existing regulations are sufficient. We think the existing freedom of contract between issuers and research providers should remain in place.”

The German fund industry association, BVI, similarly dismissed the proposed changes: “We do not see any additional value to introduce a completely new code. Existing national codes should in practice be sufficient beyond current regulations.”

By contrast, French stakeholders strongly aligned with ESMA’s Option 3, which mirrors their existing national framework. AMAFI, the French sell-side market association, advocated clearly for the proposal: “We fully support leveraging the successful French Charter. Existing contracts should be grandfathered to avoid disruptions, maintaining equivalence with regulatory standards already present under MiFID II and MAR.”

BNP Paribas also expressed clear support for Option 3: “We support the ESMA initiative, taking the French Charter as a base, as it already provides clear standards that effectively address independence and conflicts of interest, with only minor necessary adaptations for broader European applicability.”

Support for Option 3 extended beyond France, with pan-European bodies such as Euro IRP, representing independent research providers, underscoring the approach’s balanced nature: “Euro IRP agrees with Option 3. A tightened code of conduct as proposed by ESMA is welcomed, provided it does not restrict independent research providers from participating. Sponsored research remains essential for market competition and coverage of smaller issuers.”

Elsewhere across Europe, the consensus favoured balanced, proportionate regulation. Italian and Spanish regulators called for simplicity and flexibility to support SMEs. The Austrian Federal Economic Chamber endorsed upfront payments but also recommended flexibility for smaller issuers. Nordic respondents agreed on structured independence standards yet opposed overly stringent disclosure obligations.

Professional analyst associations across Europe supported enhanced transparency but diverged on contractual specifics and payment terms. Financial institutions and industry associations consistently favoured greater contractual freedom, reflecting concerns over flexibility and practicality.

Investor-centric bodies advocated for immediate transparency and strict conflict-of-interest management to protect investor interests.

Eumedion, representing institutional investors dedicated to long-term investment, highlighted transparency’s critical role: “We would strongly advise to require any issuer-sponsored research to be made public immediately, at no additional costs to investors, irrespective of whether these investors have a client relationship with the research provider.

Teun Johnston has been named CEO of Artemis Investment Management, effective April.

Artemis holds £28.5 billion in assets under management.

On future plans, Johnston said: “We will seek to further enhance Artemis’ strengths in ongoing collaboration with our supportive strategic partner, AMG, with a focus on broadening our client base internationally and diversifying our investment offering.”

He replaces senior partner Mark Murray as head of the company. Murray will retire in June.

Johnston has more than 30 years of industry experience, most recently serving as CEO of Man Group GLG, the company’s discretionary investment manager. He left the company during a reorganisation in January 2024, which also saw GLG combine with other investment teams.

Earlier in his career, Johnston spent two years at Oakley Capital as head of investments.

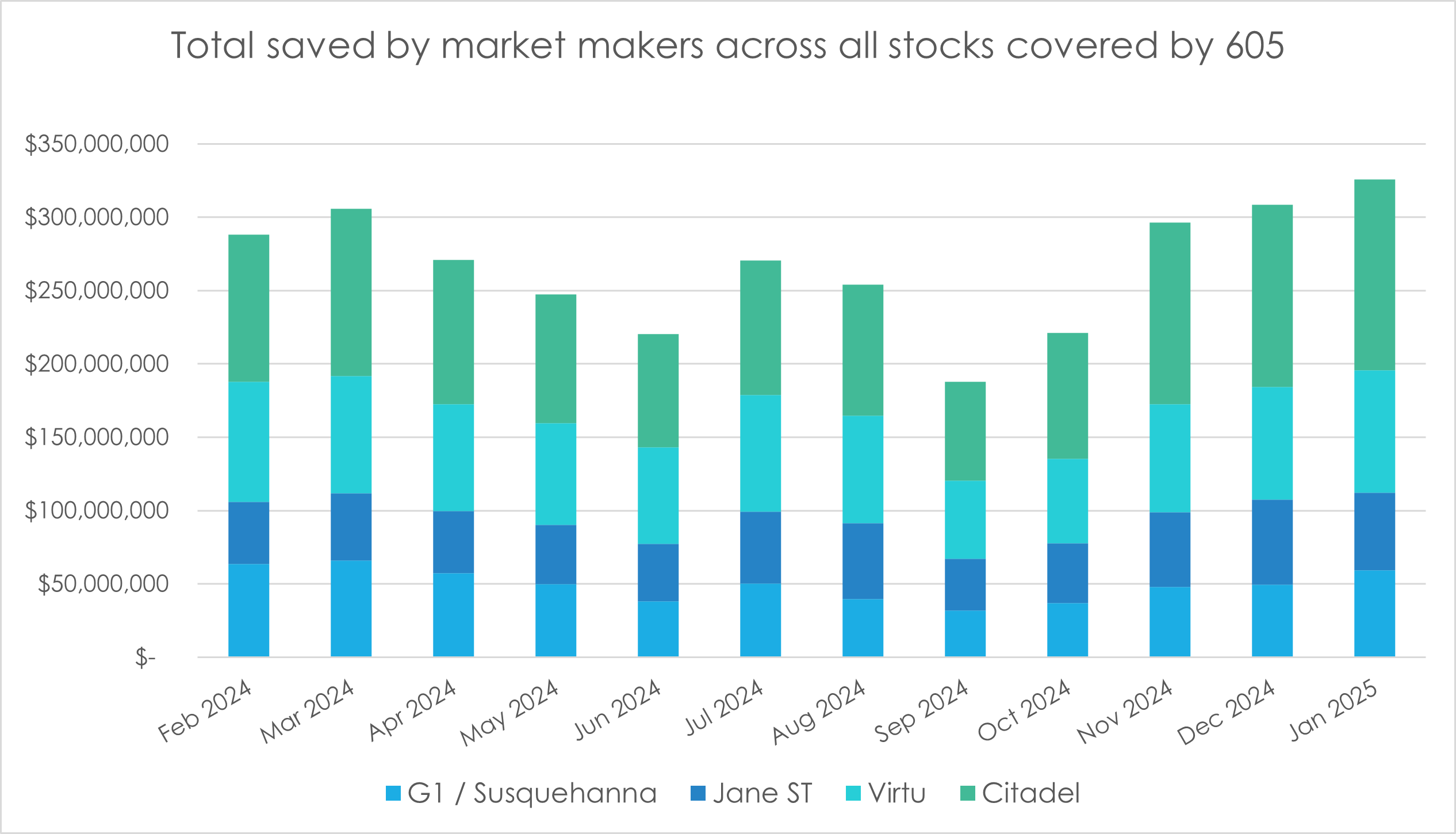

Citadel Securities, Susquehanna, Jane Street, and Virtu offered retail customers of brokers a combined US$3.2 billion improvement on pricing compared to public venues during 2024, according to Global Trading analysis of best execution filings.

US retail brokers such as Robinhood have become notorious for selling their order flow to large market makers.

In return, these market makers are required to provide best execution for retail traders. Evidence of their compliance and performance can be gleaned from regulatory filings. So-called “price improvement,” defined as the difference between the execution price offered by the market maker and the quoted price on public exchanges, must be disclosed under SEC Rule 605.

Yet these disclosures, aggregated across hundreds of thousands of trades, reveal substantial differences between market makers in execution quality, trading strategies, and areas of expertise.

Effective Spread represents the difference between the execution price of a trade and the midpoint of the National Best Bid and Offer (NBBO) at the time of execution. A lower effective spread indicates superior execution quality, as it implies that traders are receiving prices closer to the mid-market price.

Dollars Saved quantifies the tangible benefit retail traders gain from market makers’ price improvements relative to public exchanges. It effectively captures the direct economic advantage transferred from the market maker to the retail investor.

Across the period from February 2024 to January 2025, retail investors trading through these four market makers saw average monthly savings of approximately $267 million, underscoring the significant scale and economic impact of price improvement. This translates into an total of more than $3.2 billion saved for retail traders across the entire year.

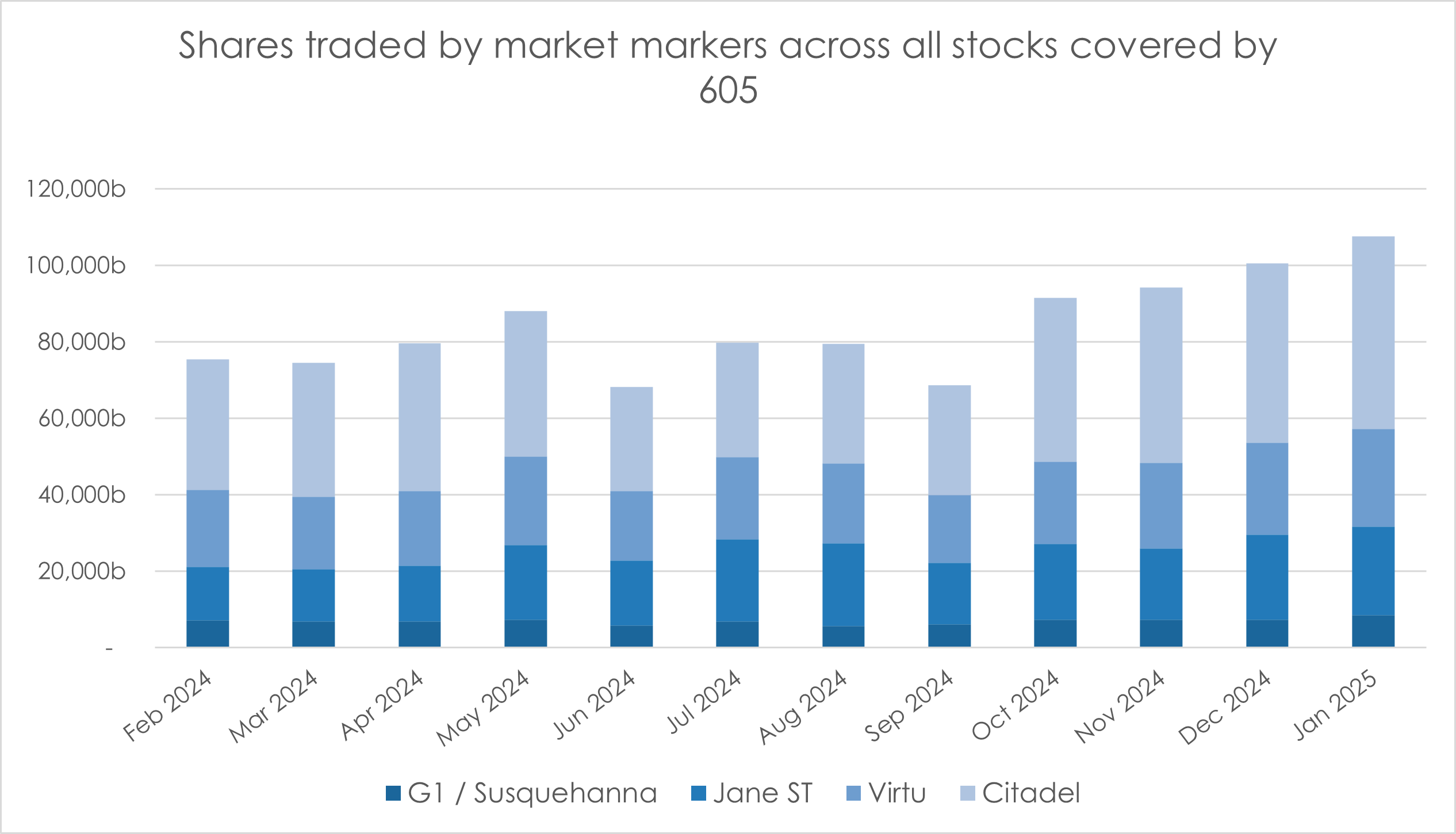

Trading activity was equally robust, with the market makers collectively handling over 567 billion shares during the year. This volume indicates substantial retail engagement, highlighting the critical role these market makers play in facilitating market liquidity.

Virtu distinguished itself by consistently providing the lowest effective spread among its peers, averaging $0.004 per share. This indicates a strategic focus on highly liquid and stable stocks, where competition and efficient markets lead to narrower execution margins.

Susquehanna (G1SUS), in contrast, achieved the highest average dollar saved per share, at around $0.0085. This suggests that Susquehanna specialises in trading environments characterised by greater volatility and lower liquidity, where opportunities for price improvement—and therefore potential dollar savings—are more pronounced.

Citadel Securities and Jane Street occupied intermediate positions, successfully balancing tight execution spreads with substantial dollar savings. Citadel, for instance, averaged effective spreads around $0.005 per share while providing considerable savings. Jane Street delivered an effective spread averaging $0.0052 per share, maintaining a solid middle-ground performance. Citadel traded 150 billion shares and saved retail traders over $900 million during this period, while Jane Street dealt around 110 billion shares, achieving savings close to $650 million.

The data revealed clear specialisations among market makers. G1SUS frequently prioritised trading in volatile or less liquid stocks, accepting wider effective spreads—sometimes exceeding $0.01 per share—as a trade-off for delivering higher price improvements, often above $0.009 per share, to retail clients. G1SUS’s total volume for the period exceeded 140 billion shares, contributing over $1.2 billion in dollar savings. Virtu, meanwhile, was clearly more comfortable operating in stable, liquid markets, achieving superior execution quality with narrower spreads but lower average dollar savings, typically around $0.003 per share. Virtu traded 160 billion shares, saving retail traders about $450 million overall.

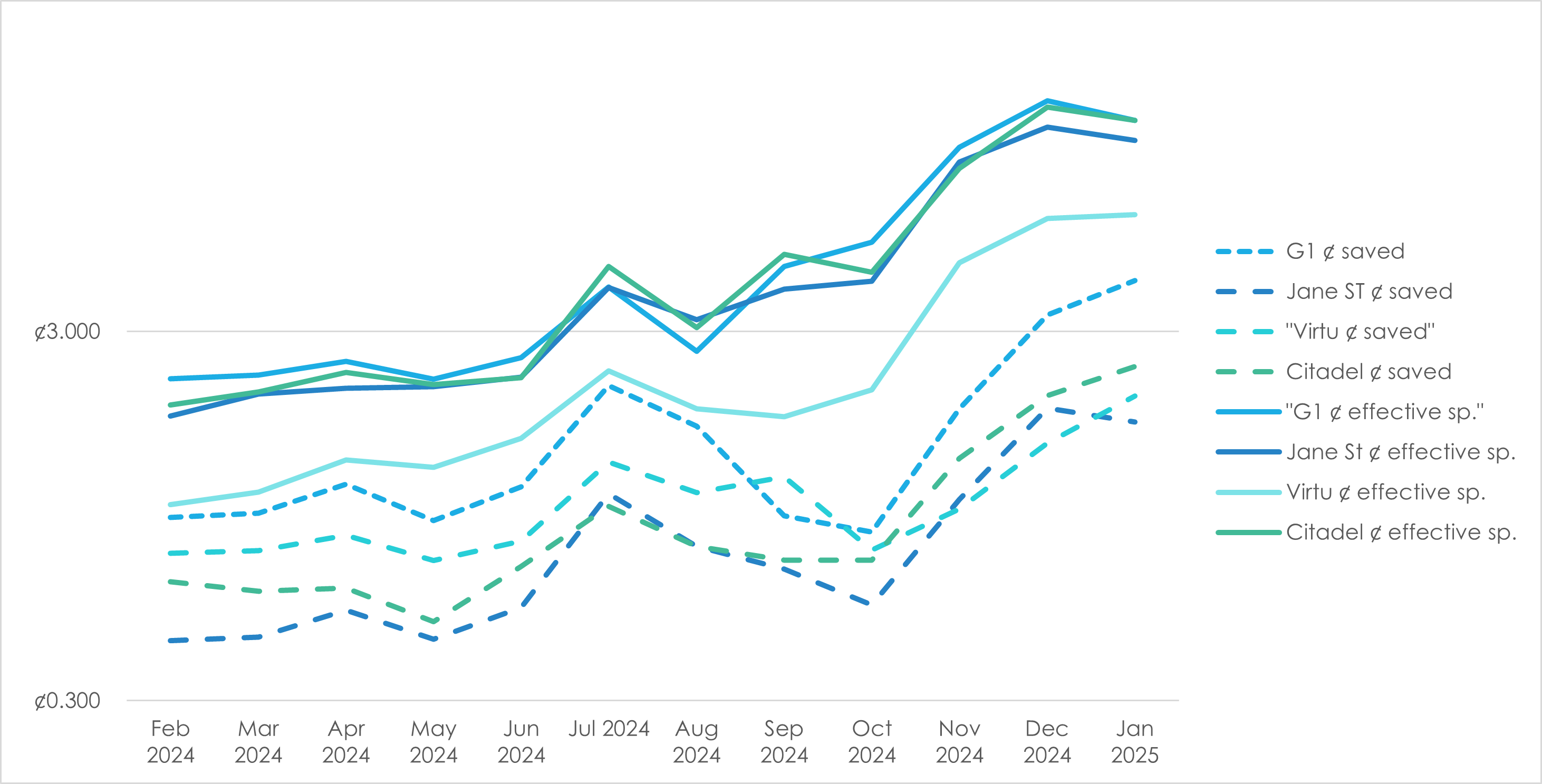

In the most actively traded stocks and the high-profile ‘Magnificent Seven’ (Apple, Amazon, Alphabet, Microsoft, Meta, Nvidia, and Tesla), Virtu again led in execution quality, recording effective spreads averaging just under $0.004 per share across approximately 65 billion shares traded, saving around $180 million. Susquehanna notably excelled in providing greater dollar savings in complex and volatile stocks such as Tesla and Nvidia, saving traders on average over $0.01 per share, equating to about $320 million across 45 billion shares traded, reinforcing its expertise in handling challenging market conditions.

Average dollar (cent) saved and effective spread for select market makers in TSLA from Feb 2024 to Jan 2025

Leveraged ETFs

Notably, among the ten most actively traded stocks handled by these market makers were leveraged exchange-traded products (ETPs) such as SOXS, TQQQ, and SQQQ, popular vehicles among retail traders for speculative bets on market direction. SOXS provides triple-leveraged inverse exposure to semiconductor stocks, TQQQ offers triple-leveraged long-exposure to the Nasdaq-100, and SQQQ provides triple-leveraged inverse exposure to the same index. Trading activity in these leveraged ETFs was remarkably high, collectively accounting for approximately 45 billion shares traded during the period. Effective spreads on these products varied significantly, from as narrow as $0.003 per share with Virtu to above $0.008 per share with Susquehanna. Susquehanna demonstrated notable performance in volatile conditions, delivering substantial average dollar savings of $0.009 per share, totalling approximately $150 million. Virtu maintained the lowest effective spreads, consistent with its preference for liquid and stable trading conditions, with total savings around $50 million on similar volumes.

As the only publicly traded entity among the four market makers, Virtu Financial provides transparency into the economic scale and profitability associated with its market-making activities. During 2024, Virtu executed an average daily volume of 554 million shares specifically under Rule 605 disclosures, peaking at 612 million shares daily in the fourth quarter. This represents but a tiny fraction of the actual volume of shares traded by Virtu which stood at 12.2 billion shares on average daily in 2024. This translates into daily average adjusted net trading income (NTI) from market making increasing from US$4.5 million in Q1 to US$5.5 million in Q4.

Virtu’s financial results also highlight significant expenses related to Payments for Order Flow (PFOF), brokerage, exchange, and clearance fees. These totaled $674 million for the year, with $207 million incurred specifically in the fourth quarter. Although Rule 605 disclosed activities represent a substantial and measurable segment, it is crucial to acknowledge they form only part of Virtu’s and other market makers broader and more opaque market-making and execution services, particularly in derivatives markets and other asset classes.

John Fawcett, head of equities engineering, Citadel

Robinhood’s director of product management for brokerage API has jumped to Citadel, taking on the head of equities engineering title.

Citadel Securities has a close relationship with Robinhood, paying $191 million per quarter for equities and options order flow, according to regulatory filings.

John Fawcett replaces Juan Leon, who left the company in June 2024 to operate boutique consultancy firm LightWake.

Citadel confirmed, but declined to comment further, on the appointment. Last September, it also hired William Pan as an engineering lead for the equity business.

Fawcett has more than 25 years of industry experience, and has been at Robinhood since 2020 covering brokerage data products and leading the trading platform and clearing product management team.

Earlier in his career, he founded investment algorithm development platform Quantopian and research management solution provider Tamale Software, which was acquired by SS&C Advent in 2008.

Stephen Peyser, global head of trading and capital markets, Balyasny Asset Management

Stephen Peyser has been named global head of trading and capital markets at Balyasny Asset Management.

US-based manager Balyasny holds more than US$21 billion in assets under management. It covers multiple asset classes, with a focus on equities.

Peyser joins from Bank of America Merrill Lynch, where he spent more than a decade as a managing director and head of US cash equity trading.

Earlier in his career, Peyser was a vice president of equity trading at Goldman Sachs, focused on consumer discretionary stocks, and a consumer sector-oriented equity trader at JP Morgan.

UBS has shuttered its outsourced trading business, the UBS Execution Hub, for global markets clients. The decision brings the purported success of the strategy into question.

Those familiar with the situation say that the decision is part of resource reallocation for the global markets. More broadly, the firm as a whole is reorganising its business plans following last year’s merger with Credit Suisse.

Ian Power

Just a few weeks ago, Ian Power was appointed head of the Execution Hub service. UBS has not confirmed his new role within the company.

In a statement, a UBS spokesperson said: “In the fourth quarter of 2024, our global markets division recorded its highest quarterly market share gain for cash equities and the highest prime brokerage balances ever. We continue to focus on growth and remain dedicated to our clients as we service them through our broad and leading global markets offerings.”

Outsourced trading allows firms to expand their coverage geographically and across asset classes, and is often used to minimise operational costs. However, concerns have been raised by market participants that engaging such a service reduces the value managers can pass on to clients.

The strategy is a significant source of revenue for providers, although most are hesitant to disclose their earnings details. UBS is no exception, with figures for the Execution Hub not published.

Clients using UBS’s Execution Hub will be offered alternative services from the global markets division. It will remain available for global wealth management and ‘banks for banks’ users for the foreseeable future.

The Depository Trust and Clearing Corporation (DTCC) is introducing 24/5 clearing hours for the National Securities Clearing Corporation (NSCC), effective Q2 2026.

This will allow the NSCC to provide its central counterparty guarantee of transaction completion to overnight activity and for those in different timezones, DTCC explained, reducing counterparty risk and increasing liquidity.

Plans to extend the trading hours schedule began in September 2024 with the decision to let market centres and trading platforms submit trades at 1:30AM ET. The initiative follows demand for standard operating hours across US market exchange and alternative trading system (ATS) providers, DTCC said.

Kevin Tyrrell, head of markets at NYSE, stated: “This initiative highlights the continued advancement of our capital markets and the increasing global demand for US listed securities.”

The NSCC will work with SIFMA, regulators and industry participants to ensure alignment across extended exchange and ATS hours and support any changes required to post-trade processes, it said.

Interest in 24-hour trading for US equities has steadily increased over recent months, with a number of exchanges announcing plans to move to an all-hours model.

Cboe Global Markets announced in February that it planned to offer 24-hour trading for stocks on its EDGX venue, however significant market changes are required for the project to be operational.

In October 2024, NYSE shared that it would be extending trading hours on the NYSE Arca equities exchange to 22 hours a day.

Oliver Sung, head of North American equities at Cboe Global Markets, commented: “We are pleased to see DTCC’s support and commitment to providing the critical clearing infrastructure that will be an essential component to a successful implementation.”

A month after Cboe, Nasdaq announced its own plans to begin 24/5 trading in 2026.

Kevin Kennedy, executive vice president and head of North American markets at Nasdaq, stated: “Overnight trading represents the next step in the evolution of the US equity markets, offering a pivotal opportunity to broaden investor access and redefine the trading ecosystem. We recognise the magnitude of this change and the need for the industry to come together to ensure a seamless transition for market participants.”

From 24-hour trading to the T+1 shift, the amount of time that international US equities investors have to determine execution strategies and hedge US exposure is being condensed. As a result, demand for real-time US market data is rising – particularly among APAC clients, according to market data provider QuantHouse.

Part of software company Iress, QuantHouse has expanded its US equity market data suite by providing clients access to Cboe Feed One. It is the 17th vendor to distribute the feed.

Cboe One Feed provides consolidated data from Cboe’s four US equity secondary electronic trading venues, BZX, BYX, EDGX and EDGA. According to Cboe, quotes from the platform are within 1% of the national best bid and offer 97.26% of the time.

Nasdaq declined to comment on the accuracy of this statement.

Cboe One Feed users can select either the summary or premium feed, the latter of which provides five levels of aggregate depth information along with top and last sale data. The data will be accessible on a subscription basis, as with other data feeds on the QuantHouse platform, with the data itself accessible via Cboe directly.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] Please review our updated Terms & Conditions and Privacy Policy carefully. By continuing to use our services after Aug 25, 2025, you agree to these