Katherine Gallagher, senior portfolio manager, Procyon Partners; Massimo Santicchia, head of US equities, Procyon Partners

Investment strategies firm Alpha Quant co-founders Massimo Santicchia and Katherine Gallagher have joined Procyon Partners as senior vice presidents.

Santicchia has been named head of US equities, while Gallagher has joined the firm as a senior portfolio manager.

Alpha Quant did not respond to questions of how their management structure would change after the moves.

On the appointments, Santicchia said: “Our strong track record across various equity styles reflects our disciplined and systematic investment process developed over more than 20 years of research. These strategies are now available to both Procyon’s advisors and their clients and on several external platforms. I look forward to developing innovative equity strategies that drive performance while managing risk in meaningful ways.”

Investment advisor Procyon, part of the Dynasty Financial Partners Network, holds more than US$8 billion in assets under management and specialises in institutional retirement consulting and private wealth management.

Prior to Alpha Quant, Santicchia’s nearly 30-year career included leading S&P Investment Advisory Services’ investment strategy programmes and associate roles at Credit Suisse First Boston and Goldman Sachs.

Gallagher also spent more than a decade at S&P Investment Advisory Service, latterly as a senior portfolio officer.

Jaafar Amrani, EMEA head of liquidity strategy, BNP Paribas CIB Global Markets; Alexandre Roubaud, EMEA head of secondary and options markets, iShares Global Market, BlackRock

BlackRock’s Alexandre Roubaud and BNP Paribas’ Jaafar Amrani have joined the EuroCTP advisory committee.

On the appointments, EuroCTP said: “These recognised professionals in the financial sector will help enrich our discussions and contribute to the creation of an optimal European shares and ETF consolidated tape. We look forward to the upcoming exchanges”

Roubaud has more than 15 years of industry experience, spending the bulk of his career specialising in ETFs. He has been EMEA head of secondary and options markets for BlackRock’s iShares Global Markets since 2018.

Amrani, currently EMEA head of liquidity strategy at BNP Paribas CIB Global Markets, has spent more than 20 years in the industry. He spent more than a decade on the cash equities team at French investment bank Exane.

EuroCTP was established by 15 European exchange groups, with the supervisory board consisting of representatives from BME Exchange, Deutsche Boerse, Euronext, Nasdaq and the Bulgarian and Vienna Stock Exchanges.

ESMA is expected to begin its selection process for the equity consolidated tape in June, with authorisation scheduled for the first half of 2026.

José Manuel Ortiz, head of securities services, SIX

Spanish stock market operator BME has amended its settlement model in preparation for T+1.

From 17 March, the Spanish central securities depository Iberclear is no longer required to have a post-trading interface (PTI) for the traceability of securities during their lifecycles.

The PTI is an information system for the supervision of trading, clearing, settlement, and registration of negotiable securities.

This means that registry management and the settlement process no longer need to be simultaneously linked, reducing post-trade operational risks and costs and minimising settlement fails, BME said.

The reform aligns Spain with Party 2, the European matching criteria standard, ensuring that it is prepared for the expected October 2027 transition to a T+1 settlement cycle.

José Manuel Ortiz, head of securities services at BME parent company SIX, commented: “The collaboration and commitment of all stakeholders have been key to the success of the project, as well as the involvement and participation of the National Securities Market Commission (CNMV). We are very satisfied with the boost to the efficiency and competitiveness of the Spanish capital markets and their settlement system that this reform brings.”

The Texas Stock Exchange (TXSE) has named a number of hires before its expected 2026 launch, poaching senior names from incumbent rivals as it seeks to become “the premier listing for exchange-traded products (ETPs) globally”.

The focus on ETP listings may be a reaction to NYSE’s plans to reincorporate its Chicago exchange in Texas.

Robert Marrocco has been appointed global head and Allison Hennessy managing director of the ETP division.

Marrocco has been a vice president and global head of ETP listings at Cboe Global Markets since 2023, spending almost a decade at the company. Prior to this, he was at NYSE and ICE for three years.

Hennessy has more than a decade of industry experience and joins TXSE from Nasdaq, where she was most recently head of ETP listings. She also spent two years as managing director of US equities at the company, and almost seven years at State Street Global Advisors.

Two other Cboe alums, Kyle Murray and Laura Morrison, have joined the exchange as legal head of global listings and strategic advisor respectively.

Murray was legal head of global listings at Cboe for more than two years, a role held by Morrison between 2018 and 2022. He also served as assistant and associate general counsel at the firm and its predecessor, Bats Global Markets, from 2008.

Within the capital markets team, ex-Long Term Stock Exchange CEO Zoran Perkov is taking on the vice president of strategic operations role, and former head of client analytics at Nasdaq Global Indices William Bailey has been named managing director of market intelligence.

Nicolas Rivard, global head of cash equity and data services at Euronext, spoke to Global Trading about the liquidity landscape in European cash equities, and the evolution of dark trading.

Nicolas Rivard.

How would you characterise the liquidity picture in European cash equity markets? The picture is good. In terms of trading volumes: focusing exclusively on Euronext markets, since the beginning of the year, cash equity trading turnover is up by more than 30% versus last year, with a daily trading turnover of about €13 billion on average. It is both driven by conjunctural events but also by a more fundamental geopolitical shift, where European markets are regaining traction globally.

Then, in terms of market structure. Whilst European markets can first appear as over fragmented, the reality is more subtle. For lit trading, one can access 98% of available lit liquidity across European markets by connecting only to nine trading venues. Lit liquidity on European equities is therefore highly accessible.

And Euronext is a pioneer in the space. We have spearheaded a unique model which balances on one hand seamless cross-border trading and on the other hand strong local market grounding. On Euronext, global and local market participants can seamlessly access to seven European markets via one single connectivity and one single trading platform. As a result, in the cash equity market, Euronext is the largest lit venue in Europe, with more than 25% equity volumes and more than 2000 equity instruments traded. And Euronext is now willing to further facilitate cross-border trading and investments by addressing one of the key remaining pain points of EU equity markets: post-trade fragmentation, with the ambition to further boost the attractivity of EU markets.

How do you see the use of lit and dark trading in Europe? The share of reported trading outside of lit trading venues is growing in Europe, being it on so-called dark pools (dark MTFs) or on bilateral platforms (systematic internalisers, off-book on-exchange and OTC). Lit markets are still, I think, working very well. The price formation has not suffered, the liquidity at-touch on Euronext is as good as before COVID. So the market quality is there but indeed, there needs to be an honest and open industry-wide debate around the balance between bilateral trading and price-forming markets. And this cannot just be a market structure practitioner debate, as it equally impacts investors, issuers and the overall attractiveness of the European capital markets. To do so, first things first: we need to have a shared diagnosis. Today, it is still very difficult to get an accurate granular view of the market structure. The soon to be launched EU Consolidated Tape on equities will hopefully help to get a better sense of the market structure evolution and create a new impetus for more informative transaction flagging and reporting.

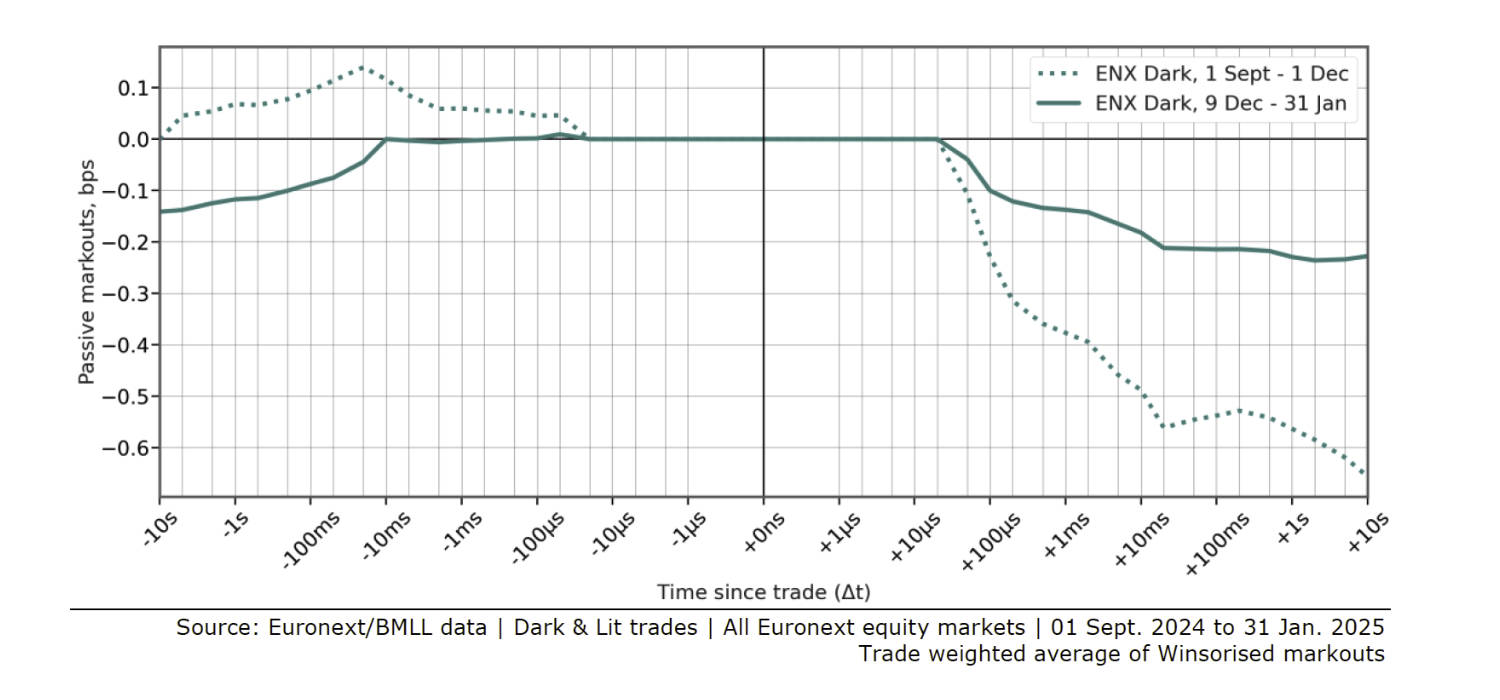

Euronext launched its dark trading offering in 2024. One year later, what’s the state of play? Euronext introduced its Mid-Point Match following our move to a new data centre near Bergamo, Italy. This initiative was driven by client demand for a dark pool that offers zero latency with the reference price from Euronext’s lit book, ensuring members can trade at the real PBBO without any latency tax. A key differentiator of our offering is our technology, in which we invest continuously. We aimed to provide brokers with a seamless way to trade at the midpoint on the same infrastructure they already use, eliminating the need for additional IT development.

One year later, we are pleased with the platform’s progress. Nearly all global brokers and many local brokers are now connected, and volumes continue to grow steadily. Building liquidity takes time, but we made three key moves in December to accelerate development:

Technical Enhancements: We made it much easier for clients to access the dark pool. If an order can’t be executed in the dark, it can now seamlessly transition to the lit book without latency, offering a plug-and-play experience.

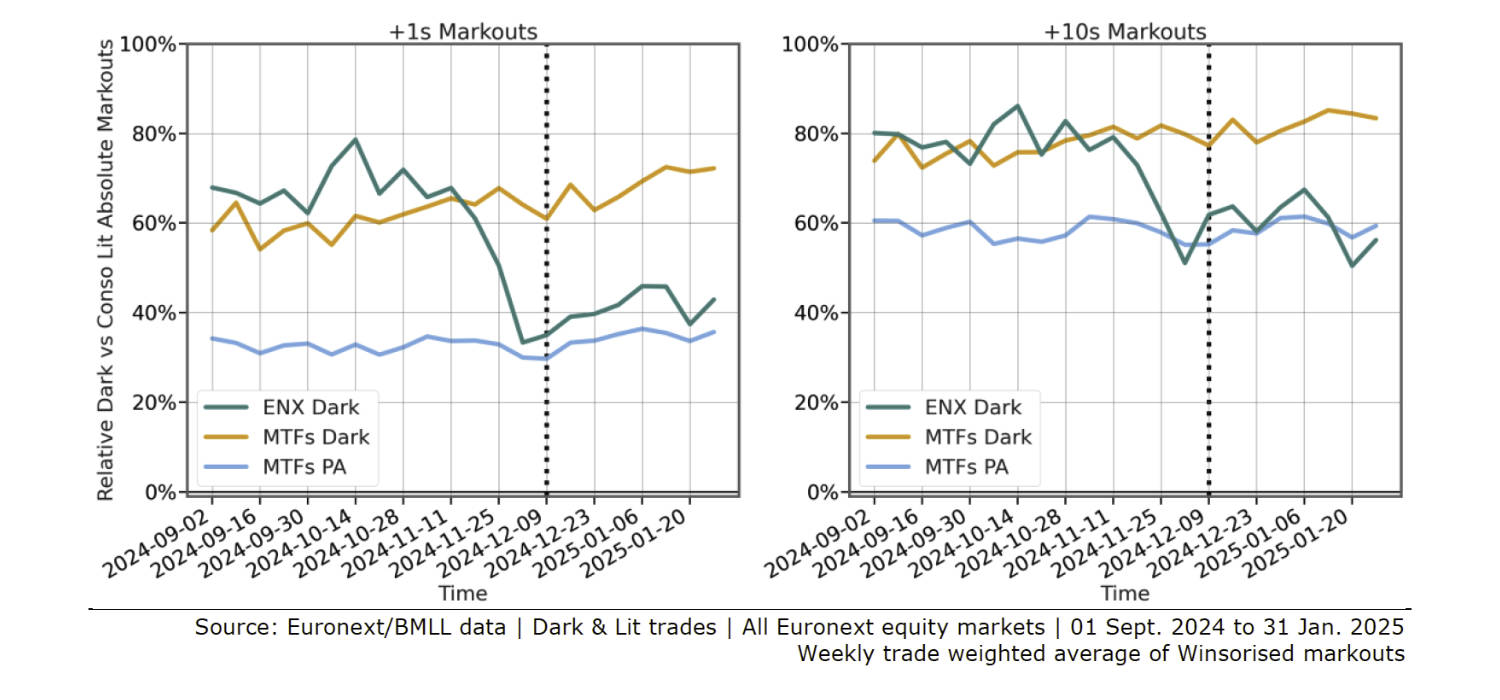

Market Quality Demonstration: Euronext Dark has proven to be significantly less toxic than competing Dark MTFs trading Euronext stocks. We delivered on our initial promise: trading at the real market price without unnecessary frictions.

Liquidity Incentives: We introduced a commercial rebate program to encourage liquidity provision, supporting momentum in dark trading and fostering deeper market participation.

With these improvements in place, we are confident in the continued growth and adoption of our dark trading offering.

What other product developments and innovations do you have in the pipeline as part of your 2027 strategic plan? We invest significantly in our trading technology and we have a number of products in design phase as we speak. In addition, we continue to develop our order entry via microwave technology we launched in July last year. We are also beefing up our retail offering. We are extending our Global Equity Market, GEM, to offer the ability to trade on Euronext technology and with the same rules basically all the blue chips in the Eurozone. Finally, there are a few areas in our market where there is untapped liquidity, and we are working to allow participants to tap into it.

Passive Markouts ENX Dark, halved since December 9 (bps, “Mid to Mid” PBBO)

Relative Dark & Periodic Auction vs Consolidate Lit Absolute Markouts (“Mid to Mid” PBBO). Euronext dark demonstrates much less toxicity than competing Dark MTFs

In the introductory panel of the FIX EMEA Trading Conference, attendees were polled on their primary regulatory focus for 2025. A significant 46% identified the rise of bilateral trading and its impact on price formation in public markets as their chief concern.

Jamie Whitehorn, head of trading venues at the FCA, acknowledging industry concerns stated: “On bilateral trading it’s our feeling that markets are effective when there’s a choice of trading functionality. We are conscious that when you kind of change one aspect of market structure, you have to be mindful of your impact on market structure as a whole.”

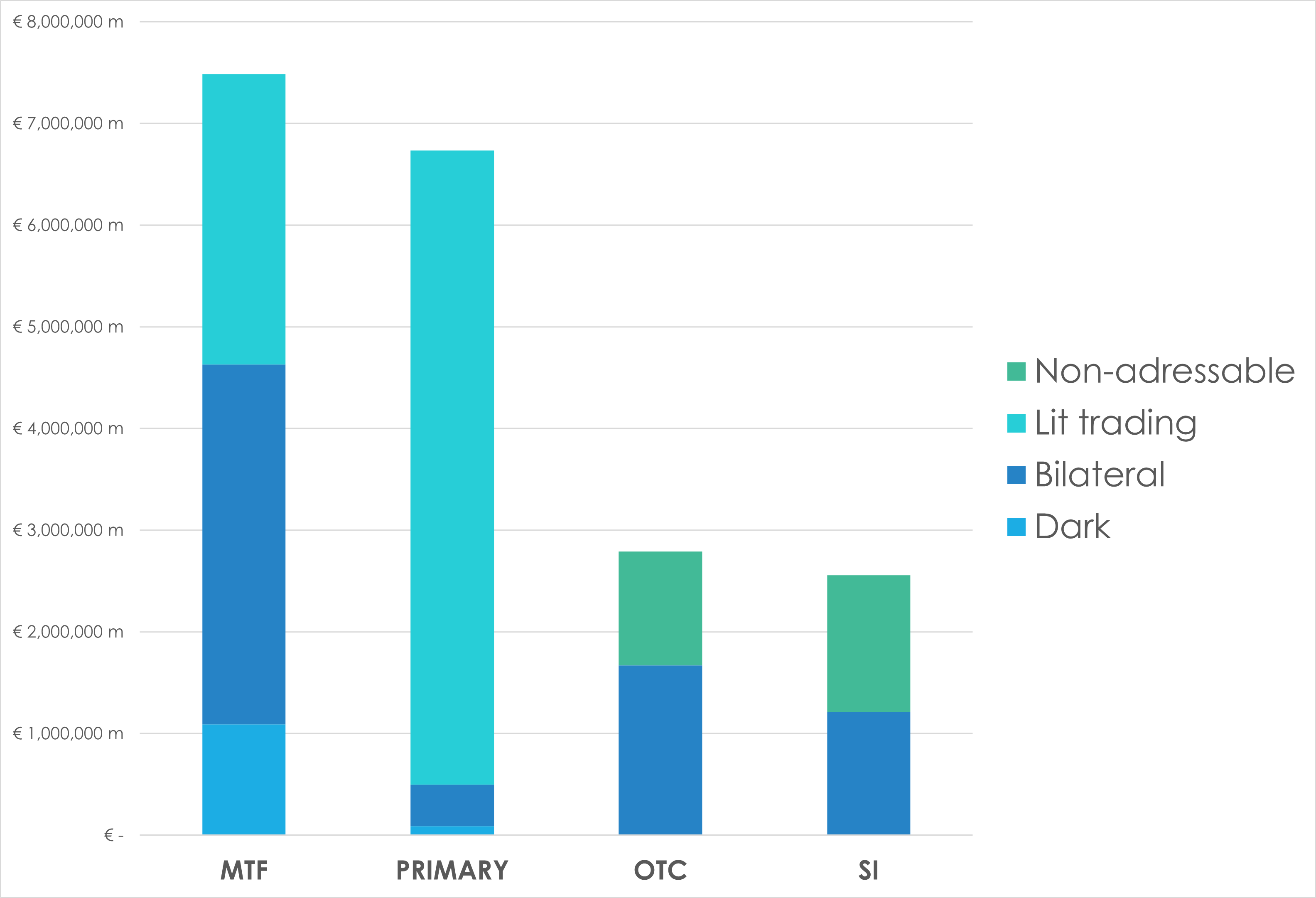

While roughly 51% of notional equity traded in Europe (Uk included) in 2024 happened in Multi Lateral Trading Facilities (MTF), principally as a function of their role providing Approved Publication Arrangement (APA)- CBOE is 90% of this in Europe- Systematic Internalisers (SI), on the other hand, represent 25% of these bilateral exchanges at €1.21 trillion in 2024 according to BMLL.

€ notional traded in Europe per class of trade, BMLL data

Recent discussions on these venues have centred on revising the SI regulatory framework: The revisions from the FCA shift the SI definition away from rigid quantitative thresholds toward a qualitative assessment of trading activity, aiming to reduce compliance burdens while preserving market integrity. The new approach, designed to align the SI definition more closely with that of a market maker by emphasizing continuous and stable liquidity provision, will come into force on 1 December 2025 in the UK with the implementation of both Handbook changes and the relevant regulatory provisions.

The AMF in France, despite being present at the event, declined to comment on these developments.

ESMA also declined to comment while Systematic Internalisers represented €1.63 trillion of notional traded in 2024 on markets under its supervision, roughly 54% of which were bilateral trades.

On 16 December 2024, in its final report on equity transparency, ESMA also presented an early Christmas disappointment to MTFs looking to offer further bilateral trading in the form of trajectory crossing order types by blocking their development plans to offer a similar service in continental Europe as in the UK.

Market participants expressed concerns about this decision as sell side firm can offer this type of services to their client, further pushing away the UK and EU regulatory regime.

When contacted, An FCA spokesperson further explained: “In Chapter 8, we considered the issue of the definition of an SI and provided conclusions on the Handbook changes we will make. In this Chapter we want to consider the future of the SI regime, for bonds and derivatives. We are not putting forward proposals for consultation but are instead asking questions for discussion. However, with the implementation of the new definition of an SI on 1 December 2025 it would be good to try and implement substantive changes to the obligations applying to SIs by that date.”

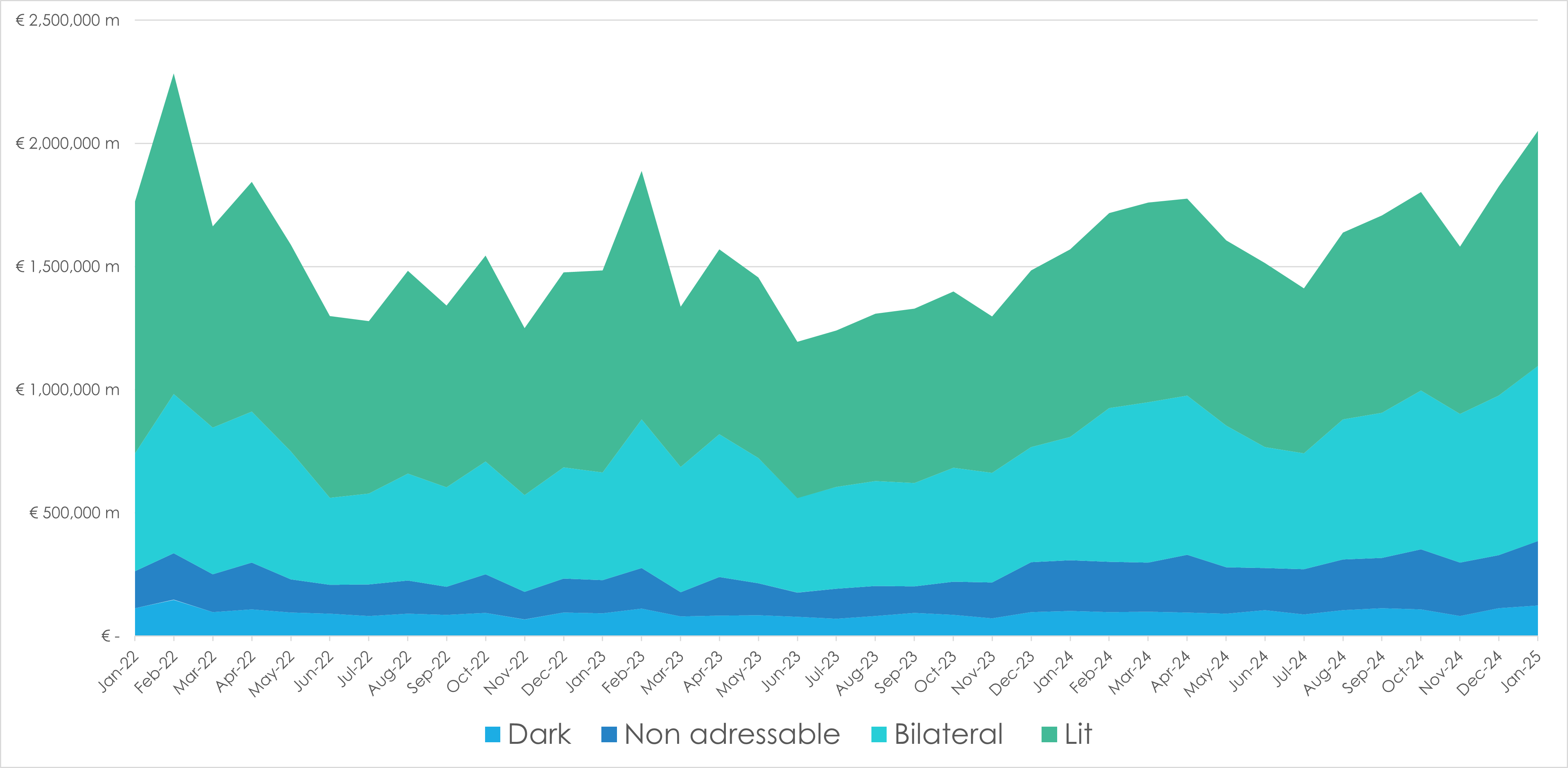

Data from BMLL highlights significant shifts in market volumes across European venues, including the UK, over the past three years.

Total notional trading volumes across MTF, primary markets, OTC, and SI markets reached €19.1 trillion). By 2024, this aggregate had increased modestly to about €19.6 trillion.

€ notional traded per venue, and type of trade in Europe in 2024, BMLL data

Looking at the market breakdown for 2022, MTF volumes were around €7.1 trillion, primary markets volumes contributed approximately €7.8 trillion, OTC volumes reached about €1.6 trillion, and SI volumes totalled €2.7 trillion. In 2024, these figures shifted: MTF volumes rose to close to €7.5 trillion, while primary market volumes declined to €6.7 trillion; meanwhile, OTC volumes increased significantly to around €2.8 trillion, and SI volumes experienced a slight drop to approximately €2.6 trillion.

A similar transformation is evident when classifying trades by execution type. In 2022, dark pool trading, captured through MTF and primary markets channel, amounted to about €1.2 trillion (roughly 6.2% of total volumes), bilateral trading totalled €6.3 trillion (33.1%), lit venues trading dominated with nearly €9.9 trillion (51.6%), and non-addressable trading accounted for around €1.7 trillion (9.1%). By 2024, dark pool volumes were marginally lower at around €1.2 trillion (6.0%), bilateral trading increased to €6.8 trillion (34.9%), lit trading declined to approximately €9.1 trillion (46.5%), and non-addressable trading expanded to €2. trillion (12.6%).

Nasdaq has been forced to suspend its high-speed trading function after accusations that it is giving select colocation clients access to lower-latency hollow-core fibre cables.

This is in violation of the SEC’s rule-filing process and the Exchange Act, and is promoting anti-competitiveness, according to a letter to the SEC from high-frequency trading firm McKay Brothers.

In the letter, McKay Brothers noted that Nasdaq was surreptitiously providing hollow-core fibre upgrades to certain clients, for a US$10,000 additional monthly fee. This option was not included in any of the exchanges regulatory filings.

“Several market participants were as surprised as we were to learn that Nasdaq covertly provides select market participants with such a latency improvement option,” McKay Brothers stated in its letter.

“[We] urge either a rule filing with respect to the hollow-core fiber offering or eliminating such offering (and any other undisclosed latency advantages) for all customers. It is extremely frustrating to periodically learn of yet another means by which Nasdaq provides hidden latency advantages to select market participants.”

Nasdaq confirmed that it is halting the provision, stating: “In close consultation with the regulator and our clients, Nasdaq has begun discontinuing the service.”

Colocation (CoLo) customers have servers and equipment running within Nasdaq’s data centre, stored in high-density cabinets. This facilitates lower latency and more efficient connectivity to Nasdaq markets.

Plans to expand the NY11 data centre and establish fees for the larger CoLo service were filed with the SEC in November 2024. The initiative was driven by greater demand for power and cabinets, Nasdaq said. The ultra-high density cabinets included in the expansion have a power density between 10 and 15 kW. They will be exclusively available in the NY11-4 centre due to the power distribution they require.

Nasdaq’s SEC filings outlined its intentions to establish a monthly fee for ultra high-density cabinets, an installation fee for cabinets in NY11-4, and power installation and distribution unit options fees.

The exchange assured that “Nothing in the proposal burdens intra-market competition because the Ultra High Density Cabinets, cabinet power options, and protocol data unit (PDU) optionality in NY11-4 are available to any customer under the same fees as any other customer, and any customer that wishes to order cabinets, power and PDUs in NY11-4 can do so on a non-discriminatory basis.”

Reserving an option on space in the expanded facility would cost US$1,000 to US$1,500 a month, the filing said, depending on cabinet density. The hollow-core fibre connection available to some clients is priced at up to 10 times this figure, and has not been listed on any fee schedules.

In promotions of its CoLo service, Nasdaq states: “Many telecommunications carriers are available, providing subscribers with an opportunity to establish diverse connectivity to and from the facility at competitive prices.”

As part of an equalisation project, Nasdaq stated its goal of creating more equal access to its data campus for all telecommunications providers. However, this development signals an anticompetitive nature to the facilities according to McKay Brothers.

“Unequal connections across the colocation service space will compel many customers to establish a third point of presence,” its letter said. “Nasdaq has not denied that its customers face this costly predicament, nor has it denied that it currently profits from maintaining unequal connectivity within NY11 and that it has a profit incentive to delay connectivity equalisation at its data centre. The situation perpetuates and expands an unjustified, inappropriate burden on competition and unfair discrimination in exchange access and connectivity.”

McKay Brothers issued further complaints around the opacity of the equalisation project, stating: “The November 2024 Chicago event on the NY11-4 expansion and the Equalisation Project was by invitation only. It is unclear why this event was not open to the public and the Commission.

“The event followed many months of Nasdaq’s selective disclosure through confidential technical specifications to select market participants only. It is unclear to us if Nasdaq affiliates also gain an information advantage.”

Concerns of ambiguous language in the information that has been released about the project, including references to “fibre”, “cable” and “media”, were also raised by the firm.

“[This] leaves open the possibility for specialized types of fibre, cable, or media that could provide hidden advantages,” the letter stated.

“Given our experience with Nasdaq’s hollow-core fiber offering, we believe the lack of specificity is intentional.”

Whether Nasdaq has been providing latency advantages to clients by other means is now in question, McKay Brothers said, stating that “given Nasdaq’s persistent lack of transparency, they can no longer be granted the benefit of the doubt”.

The financial industry’s escalating reliance on high-quality data is accompanied by significant cost implications, deepening the divide between firms with robust access to critical market data and those without.

Mike Poole.

Mike Poole, head of trading at Jupiter Asset Management, highlighted this disparity: “Not everyone has the same access to critical data, and that disparity directly influences trading behaviours and venue choice.”

Recent studies have underscored the severity of rising market data costs. According to Substantive Research, average renewal increases for major vendors fluctuated between 14% and 18% from 2022 to 2024, while annual market data budgets saw only modest growth of approximately 2% during the same period. This disparity suggests that firms are grappling with consistent annual cost increases that outpace their budgetary expansions.

Index and ratings data have experienced particularly steep price hikes. For instance, some clients have been charged up to 12 times more than their peers for identical products and use cases, highlighting significant pricing inconsistencies within the industry.

Giulia Pecce, AFME.

The rising cost of market data and research, especially in the context of research unbundling under MiFID II, has sparked considerable debate. Giulia Pecce, head of secondary capital markets and wholesale investor protection at AFME, expressed concerns over the escalating financial burdens firms now face. She noted: “The FCA draft rules on payment optionality last year were quite prescriptive, and we provided feedback that more flexibility was needed for the new regime to meet its ambition.”

Pecce further emphasised the complexity of the evolving regulatory landscape, pointing out emerging disparities between the UK’s and the EU’s approaches to market data and research costs. She stated: “There is some divergence between EU and UK rules. However, our view is that the changes introduced in the two geographies are sufficiently aligned to allow firms to adopt the new payment options if they choose to do so.”

Mike Carrodus.

During a panel discussing the future of information in financial markets, the growing tension between human-produced research and machine-driven analytics was identified as a catalyst for change in the shifting economics of trading operations. Mike Carrodus, CEO of Substantive Research, noted the industry’s increased spending on data even as traditional research budgets shrink. He remarked: “Data is such an important currency now; it’s transforming processes and market practices.” Regarding the associated costs, he added: “We’ve seen declining research budgets juxtaposed against significant increases in data pricing for indexes, ESG, terminals and ratings —14% to 15% higher in the past year alone.”

These changes have broader implications, particularly for smaller market participants who may struggle to justify increased spending on market data and research through commission sharing agreements (CSAs). As firms reassess their strategies, the role of technology providers and data aggregators becomes more crucial, offering potential solutions for managing these costs.

Ultimately, the critical question facing market participants and regulators alike is clear: who will bear all these escalating data costs, and how sustainable is the current trajectory? As Pecce succinctly concluded: “We were pleased to see that the rules, as finalized by the FCA, provided additional flexibility, which is important to maximize the chances that the new payment option is adopted.”

Tim Lipscomb, executive vice president and CTO, Cboe Global Markets

Cboe Global Markets has promoted Tim Lipscomb to executive vice president.

Lipscomb has been chief technology officer and a senior vice president at the firm since 2022, covering Cboe’s global technology platform expansion and supporting the firm’s overall growth strategy.

On Lipscomb’s time at the company, Chris Isaacson, executive vice president and chief operating officer, commented: “Tim also guided our technology team through major milestones, including multiple successful technology migrations that have brought our equities, options and futures markets globally onto one unified global technology platform, Cboe Titanium.”

Before becoming CTO, Lipscomb was chief operating officer for Cboe Europe and a managing director at Merrill Lynch.

Whether market fragmentation is causing a liquidity crisis in Europe depends on who you ask. Buy-side players often lament the financial and operational cost that fragmentation is bringing down on them, but the sell side is keen to dispel their concerns as myth.

The debate was centre stage at this year’s FIX EMEA conference, as sell-side speakers assured the audience that fragmentation is less of a problem than people think – and that change is possible.

Alison Hollingshead, chief operating officer for investment management at Jupiter Asset

Management and the sole buy-side voice on the panel, told the audience: “There’s a lot of data we need and at the same time, we’re being asked to optimise our setup and control costs. The buy side is being asked to do more and more for less, and to really up our game and ensure that execution is a core component of the investment process.”

Determining where the actionable and addressable liquidity is in Europe should be a priority, she said. “We need to understand where the flow lives and where it’s traded.”

Addressable liquidity, that which can be interacted with on or off exchange, is increasingly difficult to measure as more venues and trading routes are introduced to the market.

Speaking to Global Trading after the event, Hollingshead added: “I think the problem is not that there is no liquidity, but how best to get things done and where.”

Admitting that there is room for improvement but arguing misrepresented data when it comes to addressable liquidity, Eleanor Beasley, EMEA head of market structure and COO at Goldman Sachs, hit back. “Liquidity in Europe is not perfect,” she acquiesced, “but it’s not

Left: Eleanor Beasley, EMEA head of market structure and COO, Goldman Sachs

as bad as some say. Unlike the US, in Europe people aren’t looking at the whole pie. Less volume is happening on the lit market for many reasons, so if you only reference lit liquidity, you are underestimating what is really available.”

Also coming to the defence of the region, one sell-side panellist commented that Europe is, by nature, fragmented. “We need to stop apologising for that,” they urged. “The US is fragmented too, but not for geographical reasons – they wanted competition, to grow their market. What’s important is how you connect the dots, the layer you put on top to get market participants to choose to invest in you.”

Alex Dalley, head of European cash equities at Cboe Europe, was eager to bring up European markets’ performance in single-stock listings compared to the US.

Cboe’s European equities business took 24.6% of market share in Q4 2024, reporting an average daily notional value of €10.4 billion.

Alex Dalley, head of European cash equities, Cboe Europe

“Europe is actually much less fragmented than the US market in terms of how single stocks trade across the ecosystem,” Dalley continued, comparing AstraZeneca, a single stock on an interoperable cleared market in the EU, to Nvidia. The former has five options for lit trading venues, eight dark venues, six non-bank internalisers and 25 internalising brokers of meaningful size. The latter faces 17 lit venues, 30 alternative trading systems, eight single-dealer platforms and more than 100 systematic internalisers.

Fragmentation is more visible in whole portfolios in the EU, where domestic exchanges bring the total number to 30.

Considering post-trade processing, on an all-stocks basis, there are more than 20 settlement options – one per incumbent exchange, one or two more for ETFs, and two settlements per security, compared to just one settlement to a single CSD in the US.

“It’s not the degree of trading platform choice that is preventing Europe from being the biggest stock market,” he stated; although the whole-portfolio view illustrates that it is still a factor.

Dalley argued that the issues associated with fragmentation lie not in trading platform choice but in the complexity of how market data is purchased and post-trade processing.

From a buy-side perspective, Hollingshead shot back, “explaining where our volumes lead to reversion [prices moving away from their historical means] or higher toxicity levels [a high number of sub-optimal prices or bad fills] is really important.

“We need to be managing that, thinking about our impact, thinking about real market costs, about efficiency of settlement, and then also trying to take on board all these new ideas and innovations. Then we partner where adverse selection is limited.”

Simon Dove, head of liquidity, Instinet.

To truly address European market structure issues, significant innovation is needed – particularly around the lack of interoperability of clearing services. “We know where we need to get,” said Simon Dove, head of liquidity at Instinet. “We’re talking about the same thing we talk about every year, but we need solutions. We need to be frank and honest with ourselves.”

“People calibrate how much they trade by how much it costs. If we innovate to bring costs down, people will trade more in Europe,” he added.

Market complexity is, in some cases, a byproduct of market evolution. “We can’t put the genie back in the bottle and return to how the market was years ago,” Beasley concluded. “We need to acknowledge that the market is evolving, participants have changed and new workflows have emerged. This isn’t necessarily a bad thing as long as we ensure standards remain high.”

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] Please review our updated Terms & Conditions and Privacy Policy carefully. By continuing to use our services after Aug 25, 2025, you agree to these