By Francis So, Head of Trading, APAC, BNP Paribas Asset Management

Francis So, BNP Paribas Asset Management

The COVID-19 pandemic has had a profound impact on our daily lives, from the way we live to the way we work. At BNP Paribas Asset Management (BNPP AM), the priority has always been the safety and well-being of our staff, supporting our clients, and ensuring business continuity.

Before COVID struck, business continuity planning was always a top priority at BNPP AM. Even so, the concept of an extended period of working from home was just that – a concept (at least for traders). The reality of trading from home brought to the fore new and sometimes unexpected challenges for our trading teams.

Just a few of the obstacles included: ensuring regulatory compliance within each jurisdiction; the lack of a recorded telephone line; hardware issues; internal and external communication; and unstable internet connections. Overcoming these issues required resilience, agility and innovative thinking. The speed at which the industry adapted and evolved has been impressive.

In Hong Kong, we increased our focus on Business Continuity Planning in February 2020, where employees worked from three different locations (the office, a BCP site, and home). This recalibration was to ensure the safety of all employees, reduce contamination risk, and minimize disruption to the business. Our European and US offices followed later with BCP adapted to their specific markets. I have the deepest respect for my colleagues as they have shown commitment to the business and continued to support our clients, even while not physically present in the office.

New ways of working

Globally, trading volumes have surged with higher market volatility. With pressure at unprecedented levels, traders have had to continue to handle these orders promptly and accurately – all the while operating from their home office.

One of the major challenges of trading from home is communication, not just with external parties but also internally. Communication with our brokers, many of whom were also working from home, was slower than normal; sales and traders were separated and were either working in different locations or from home. For example, in the fixed income space, we witnessed slower responses to RFQs (Request for Quotes), wider spreads, liquidity fragmentation and hesitation to take positions (not a total surprise given heightened volatility and political uncertainties).

Internal communication with different stakeholders (fund managers, operations, etc.) was facilitated relatively smoothly through systems such as Symphony and Skype – but having a face-to-face conversation is always more preferred.

I cannot stress enough the importance of communication, especially with our operations/back office support who are not located in Hong Kong. Given that many markets in Asia have a buy-in regime when trades fail, close monitoring of trades and communication between the trading function and trade support is required to ensure timely and accurate settlement of trades. I am proud to say that we didn’t have a single buy-in incident during this time.

The Future

Increasing the productivity and efficiency of the trading desk has always been a key objective. This pandemic has highlighted and accelerated the need to do so by automation, whereby orders are automatically executed with little or no trader involvement, and defined by specific parameters.

Automation by no means will replace the traders but will allow them to focus on more difficult trades and generating alpha. Electronic platforms such as MarketAxess, Liquidnet and FXall will continue to thrive as they enable traders to access liquidity pools and trade more efficiently with transparency. As face-to- face contact with brokers has become restricted, new forms of communication have evolved; teach-ins via video conference (via Zoom, Webex, others) are becoming the norm and numerous virtual conferences have emerged.

On a personal note, one of the positives of working from home has been more time with family. While BNP Paribas Asset Management always strives to ensure employees nurture both their work and personal needs, there is no doubt that more flexible work arrangements make getting the balance easier. From my experience, people who are happy and balanced are more productive and positive in the office.

One thing is for certain, change is constant and the industry must be flexible to adapt and evolve or be left behind. The work from home concept is no longer a concept but a reality – and it works.

Markets Media Group spoke with Richard Cohen, Head of Primary and Credit Markets, APAC, and Allie Eom, Head of Advisory Sales, APAC, at BNP Paribas. Cohen is an Executive Sponsor of BNP Paribas’ Women in Global Markets Asia Pacific, and Eom is a Board Member.

What is the current state of the landscape for women in finance. What progress has been made, and what progress is still needed?

Richard Cohen, BNP Paribas

Richard Cohen: One thing that’s clear is that there are disparities in the number of women in markets divisions of banks, especially at senior levels. From personal experience, when I started in the business over 20 years ago, the number of women on a trading floor wasn’t really a topic, but over the years, it has grown in importance as we recognize the need for gender diversity. We still have many challenges and things to work on, such as including more women in management, especially senior management, and increasing the number of female traders across The Street. If you look at our teams, you see many female salespeople, but still relatively few female traders.

Allie, what has been your personal career experience as a woman in finance? Have you found that any doors were closed (or open), specifically because of your gender?

Allie Eom, BNP Paribas

Allie Eom: I also started my career about 20 years ago, and of course the industry has evolved over that time. I started my career in Seoul, then worked in New York for about 10 years, and now I’m in Hong Kong. I have been very fortunate and I don’t think my gender has held me back at all. I’ve always been in cash equity sales, and particularly in Asian equity sales, there has always been a great gender balance, even at the senior level. That said, beyond cash equities, there is room for improvement across different divisions and different regions, especially at the senior level.

How does BNP Paribas support and encourage women employees?

AE: This is my 14th year at BNP, so I have a good perspective on this. We get great support from day one, whether as a graduate trainee or as part of the BNP Paribas internship program. There is also internal mobility, and consideration in external hires. I benefited from internal mobility when I transferred from New York to Hong Kong. BNP also has great initiatives, including Women in Global Markets Asia Pacific; Male Allies, which Richard is part of; diversity networks such as Mixed City and Pride; as well as mentoring programs, talent programs, and training.

RC: The program Allie and I are most involved in is Women in Global Markets APAC. The key for this is that it’s not driven by HR, it’s led by the front office business, and it’s about setting up identifiable, measurable and achievable targets to ensure we increase the number of women in Global Markets APAC at all levels, from the most junior to the most senior level. The three main streams here are recruitment, retention, and client engagement, which entails engaging with our clients specifically around gender and gender diversity.

2020 has been a very unique and challenging year. How might 2020 evolve the cause of women in finance?

AE: The first words that come to mind when I think about 2020 are adaptability and agility. We all have had to adjust to a very new world. And one of the more interesting products of this unfortunate situation is the success that we have seen of working from home across various roles, and how it is actually possible. Now it’s up to employers, all organizations, to embrace this new, adaptive agility that we have shown.

Obviously working from home has its challenges as well as rewards. We have connectivity issues, we have kids running around. We might be watching kids at school while dialed in to the morning meeting — we all have different situations. But I think overall, it has made us stronger and better equipped for whatever changes the future might bring.

RC: This year has demonstrated that people can successfully work from home — in our industry especially, there were a lot of doubters about that. And I would expect, assuming the regulatory framework is there, that some of us could continue work this way in the future.

And indeed it hasn’t all been plain sailing in terms of the flexibility component, particularly when it comes to things such as homeschooling, which often falls to women. And for many people working from home, the hours have actually got very long because there’s not a true cutoff. So it is important to recognize that this flexibility has also brought challenges.

What is the value of industry events that recognize women in finance, such as Markets Media’s Women in Finance Asia Awards event?

RC: Everyone likes to be recognized and complimented. It is important and it also helps raise that person’s profile. Some studies have shown that women are less likely to promote themselves in the workplace compared with men, so I think these kinds of awards can help counterbalance that.

It’s also important for companies such as BNP, because we want to be recognized for our market-leading position in diversity. It’s good for business and it helps us attract the best talent with a diversity of backgrounds.

How can men in finance best support and encourage their women colleagues?

RC: BNP’s Male Allies program focuses on this. When you’re a male ally within BNP, it’s not just about being a mentor or sponsoring women, it’s also about how you influence others and influence the behavior of the organization. A good example is when a mother returns from maternity leave — as men, we need to understand the challenges this time brings, and guide others to think similarly so they can understand as well.

Male Allies is about helping, sponsoring, and mentoring. More importantly, it’s about nurturing a culture that promotes and sponsors balance at the firm by increasing the number of women at all levels.

What is the value of mentorship for women in finance? Can either or both of you recall any personal experiences of being a mentor or a mentee?

AE: Before I answer, I wanted to add to what Richard mentioned about how women being less likely to promote themselves or ask for help. I can say personally from my experience, that this is definitely the case!

When I first started in this industry, I had a senior manager as a mentor, who I still keep in touch with. This mentor provided me with a lot of great perspectives, as well as the ability to see a bigger picture, especially when it came to making important career decisions. He also gave me some really great advice, which I still think about. He said: ‘Don’t chase money, let money chase you.’

I can only hope that every firm has the kind of mentorship that BNP does, as it can have such a lasting impact on a person’s career.

RC: Mentorship is valuable to all people, but I think especially for women as a way to help develop their careers. A good mentor can act as a role model, help with coaching, give career advice, and then help with networking and visibility at a firm, which addresses some of the points we made earlier.

As a mentor, I always feel content when I see that someone I’ve mentored has become a success in whatever path they choose. You always hope that you had some small part to play in that.

One notable experience I had was with a mentee in a division, outside markets. One of her goals was to work outside of Asia, so we came up with a plan on how she could achieve that. One big part was networking into other groups within the bank, including senior people that I knew, and we also did interview coaching. It was successful, and she’s now a successful manager in New York.

What is the future of women in finance? Will there ever be a day when women in finance programs are no longer needed?

RC: Like many initiatives, I think the ultimate aim is that you don’t need it anymore. The aim is not to have to even think about if women have equal representation, it’s just completely natural. I believe it’s an achievable goal, but it’s going to be still a reasonably long path to follow because we still have quite a lot of ground to make up in certain areas.

AE: I always think about questions like this from the perspective of my 16-year-old daughter. If she chooses to work, in finance or wherever else, hopefully we will not have these kinds of initiatives the way we have today, and everything is quite balanced. And that for me is the goal, and it’s why I feel driven to help reach this goal. We want to create a world for our children where these programs are not needed as much.

The EMEA Trading Conference will cover the most pressing issues facing the institutional trading community and provide a neutral platform for buy-side, sell-side, exchanges, vendors and regulators to share their ideas on how the community can continue to collaborate. Designed to appeal to all asset classes, the agenda will maintain a great balance of topics across multiple asset classes.

Building on FIX Trading Community’s unrivalled knowledge of the trading issues impacting this region, a dedicated industry team is creating an event that not only focuses on current issues, but also those that will impact electronic trading in the EMEA region and beyond for years to come. Leveraging the latest technology, FIX will deliver a fully virtual mixed media conference facilitating a fully interactive and immersive virtual debate. This one day virtual conference will provide thought-provoking, forward focussed insights through a concurrent two stream agenda. The EMEA Trading Conference is renowned for its expert speakers who impart their knowledge and experience throughout the day. Previous speaker firms include ESMA, FCA, and the European Commission to name a few.

As business leaders we stand by the principle of being capable and thoughtful about the functions we’ve been entrusted to look after. There is an emotional investment, in people and product, and there is rigour around how we execute.

Do we take the time, though, to assess the efficacy of how we scrutinise our businesses?

We are willing to do the right thing when taking honest assessments of what we do, but sometimes we are actually not sure how to go about it. There’s an innate sense of needing to “fix” or “upgrade” or “rethink” something, but the operational management of running complex Trading and/or Investment platforms takes over, so we often revert to simply keeping the plane in flight, as opposed to understanding whether we should be travelling by an altogether different means of transport.

Or more worryingly, we sometimes struggle to face up to the realities of what scrutiny, as in real scrutiny, may unearth, preferring to lean on the status quo and be seen as “doing a great job”—frequently used as a euphemism for being a solid operational figurehead, as opposed to a strategic thinker—by the people around us or above us.

A Hong Kong-based friend of mine, a senior member of a large Investment organisation, recently shared with me how his firm spent a six-figure sum on commissioning a deep-dive consultancy project, only to take issue with the outcomes to such an extent—in a nutshell, local management didn’t like the optics of how the findings would land with their overseas head office—that they buried the report, choosing not to share the results outside the immediate local management committee.

Behaviours like this are rare, but distill this down to smaller, day-to-day actions: despite the usual rhetoric, do we genuinely operate in an environment of continuous improvement, of honesty, putting aside ego, appeasement or politicking so that businesses are on a real pathway to improvement?

If you are a Head of Investments, a CIO, a buy-side Head of Trading, a sell-side Head of Execution Services or Product, or a COO, the need for the re-engineering of platforms, disentangling existing infrastructure, thinking more about Electronic Trading and coherent, data-driven systems of measurement—to name a few—has never been more stark.

Working practices have been upended by Covid-19. The configuration of Trading and Sales desks (along with PMs, if you’re on the buy side) has long been seen as a model for collaboration and shared insights, but this has been severely tested given the sudden removal of the human element; that organic, ad hoc ability to share and help and advise. That physical separation has meant financial firms are having to work harder to maintain that intellectual and commercial curiosity. That loss of immediacy, on top of practical things like WiFi-based encumbrances, means businesses now face the real danger of functional and creative drift.

But perhaps this is an opportunity? While client- and operational-related travel may have stopped in its tracks, leaders have now been afforded a somewhat unique chance to slow their heart rates down, and reflect on how their businesses are shaped. Collaboration continues but in a different form; more time is being spent with internal teams—albeit remotely—focusing on core competencies, being able to think philosophically about key questions such as:

Is the value proposition to both my clients and internal stakeholders well understood and articulated?

Do the organs of my business work effectively with one another?

Is there an authentic sense of technological progression, for example exploring enhanced use of Electronic Trading?

Have I got the right people in the right seats, both in terms of helping careers progress as well as delivering product/service optimally?

In facing up to the things that need improving, external validation from a third party often produces unfettered and bias-free counsel. After all, if a group of internal stakeholders get together to, say, deploy a years’ worth of IT budget, it’s no wonder that outcomes can become skewed, a result of an amalgamation of singular opinions which are driven by internal interests, or client-specific objectives that may not be aligned with broader strategic aims.

As a sell-side contemporary recently noted to me, “I wonder; we spend all this time coming up with cool Algo products we love, but then have difficulty selling them into the client base. Why don’t we ask the clients what they need, first, then go and build them? We struggle sometimes because we’re so focused on the competitive landscape, we forget to really think about the people we’re selling into.”

An external, experienced opinion removes these potential issues by taking the emotional or political investment out of the process.

It offers an authentic fresh set of eyes—a pulse check—which, when executed in partnership with the firm being assessed, creates a validation and recommendation process which can then be used in a more powerful way.

If you are an asset manager for example, have you considered how the triangulation of Trading, Portfolio Management and Sales/Client Service is brought to bear on your clients? Have you empowered a culture of measurement throughout the investment life cycle, as opposed to just fund performance?

You may be a small/newer fund, or a start-up: have you thought about how your business is going to scale? Do you see value in Trading, or see it as more of an operational overhang that can be outsourced? Are you cognisant of building appropriate Best Execution policies, for example, to fall in line with the climate of regulatory rigour?

If you are an end asset owner and have moved down the path of in-housing assets, what is your plan for execution? Can you price technology, people and IP accordingly, so the value proposition of your external managers becomes obsolete?

Or finally, if you are a broker, have you made a proper assessment of your client landscape, your commercial proposition against this, your client-facing team and their operational bandwidth? How about the forward on the execution landscape, and how that might fit in with shifting client habits?

The process of scrutiny starts here. How will you go about it?

David Rogers launched 23rd Parallel Consulting in June 2020 after two decades in institutional trading, most recently as Head of Trading, Asia-Pacific for State Street Global Advisors.

During the pandemic we have seen a significant increase in retail activity in the stock market.

Main Street investors are good for stocks

Phil Mackintosh, Nasdaq

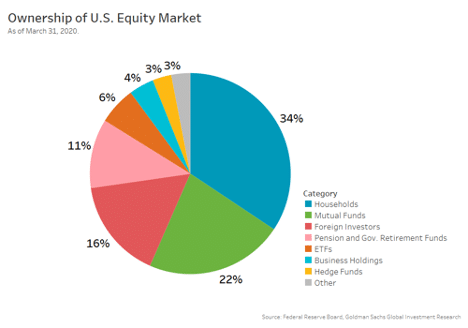

The entrant of new, Main Street investors into the stock market is mostly good. Data shows that around 45% of U.S. households still have no exposure to the stock market. Despite that, Federal Reserve data shows direct ownership of stocks is even higher than mutual fund ownership. That makes individual (direct) investment a significant source of capital for U.S. firms.

Fed data also shows that many low income households are overinvested in housing and bonds. Over the long term, stock performance beats residential real estate and fixed income. That means increased retail ownership of stocks should improve the retirement security of more households, as asset diversification reduces volatility and improves overall returns.

Chart 1: Households are already the biggest owner of stocks

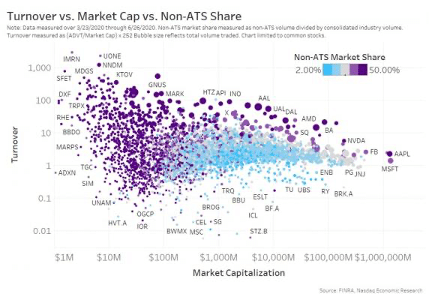

Also, stocks with higher Main Street participation (purple stocks below) seem to have higher liquidity. That tends to reduce trading costs for all investors and lower the cost of capital for companies.

Chart 2: Households appear to boost liquidity too

So there are good economic reasons to encourage these new entrants into the stock market.

Understand how stocks work

Given that, it is important that these new investors generate positive long-term returns so they remain invested in stocks. Since stocks are not “risk free” assets, this requires many new investors becoming more familiar with markets.

The good news is that there are plenty of resources for new investors online, including Nasdaq’s own page on smart investing. There you will find information on some important principles of investing—from how diversification can help reduce risks to how ETFs and options work.

We can also highlight the most important things for individual investors to know as they become more involved in the stock market.

Five things everyone should know about the stock market

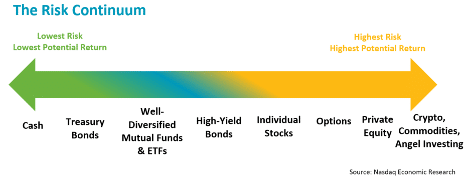

Stock markets have a lot of transparency and information for investors

Although stocks are not risk-free, they are more transparent and considered less volatile over the long term than many other investments.

Compared to other markets, stock markets are well regulated with transparent company accounting and auditors. Investors can gather a significant understanding about the financial performance and stability of any listed company.

Trading rules also require all investors see the public exchange prices from all buyers and sellers. That in turn ensures investors get the best prices on trades and receive best execution services from their brokers.

Chart 3: Stocks and ETFs lay in the middle of the risk spectrum

Stocks can go down; diversification can help

Stocks go up AND down. Diversification is what professionals use to weather the storms.

Some of the shares you buy will rally, or pay good dividends, or both. While others might not even return your initial investment to you, even after many years.

Stock prices can fall if company profitability falters. Some companies will even file for bankruptcy, and they usually return no money to stock holders. That’s why financial statements showing company balance sheet stability and profitability is so important.

Diversification is a tool used by professional investors to minimize that risk. Buying more than one stock reduces the impact on your portfolio from stocks that rise but also those that fall. Importantly, it reduces the likelihood that you will lose all of your savings. Done right it can also expose you to gain from different parts of economic cycles. Commodities, tech and healthcare stocks all tend to gain during different times in the economic cycle.

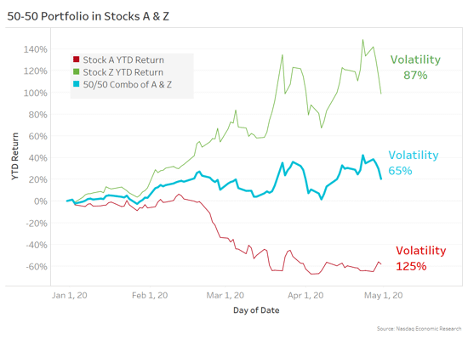

Usually diversification also reduces the volatility of your whole portfolio. This can be seen in the example in Chart 4, which tracks two real stocks in 2020. Both stocks were doing well before COVID-19 struck the market in March. Even though Stock A’s price fell more than 60% thanks to the impact of the Coronavirus on its business, it saw days with large gains. In contrast, Stock Z benefitted from changes caused by the pandemic, more than doubling, but still saw some days with significant falls. But as a portfolio, some of the down days offset, reducing overall portfolio variability (technically called volatility) and also outperformed.

Chart 4: Buying a diversified portfolio of stocks reduces risk

One of the easiest ways to build a diversified portfolio is to buy exchange-traded funds (ETFs). Almost all ETFs represent an already diversified portfolio of stocks. They may hold a collection of tech stocks, small cap stocks or even bonds.

Earnings drive valuations

At the end of the day, shares represent a part ownership in the value of a business. That valuation in turn is driven by current earnings and expected future earnings growth. In fact, a recent study by Bank of America found that over the long term, earnings explains around 80% of stock price performance.

The importance of earnings to company valuation is one of the reasons that financial statements showing company profitability and historic growth are so important. It’s also why a lot of investors look at the Price-to-Earnings (PE) ratio and might say that stocks with a high PE ratio are “rich.” But sometimes those high PE ratios will be justified by a company’s strong future earnings. Investors need to determine if growth forecasts are accurate.

Chart 5: Actual and expected earnings drive stock valuations

Interest rates also affect company valuations. Low interest rates make it easier for companies to grow faster than the economy. The current near-zero interest rates are one reason used to justify the fact that share prices have gained much more than company earnings in the past decade.

Economies can go up and down, and that affects companies

Even with a diversified portfolio, the whole market can be dragged down by a slowing economy (or a pandemic). Chart 6 shows that often these “bear markets” can last longer than a year, and diversified portfolios can fall well over 20%.

When that happens, it’s often important to be able to wait for the economy (and stocks) to recover. Bear markets often represent good buying opportunities, as stocks are cheap. Experts advise not to wait for the economic data to show the economy has started to recover, as markets are also usually better at forecasting the end of recessions and typically lead the recovery in real economic data.

Chart 6: Economies can drag whole markets down too, sometimes a lot

The economy can also affect market-wide earnings. Recessions usually cause sales to fall, which reduces profitability. That in turn leads to some job losses which cause sales to fall further.

Because of the feedback loop that these pressures can create, governments often act to limit recessions by reducing interest rates, which lowers costs, or increasing government stimulus, which increases revenues. Both these actions can improve the balance sheets and profitability of companies.

Not all trading is free

It’s easy these days to think that stock trading is free. Trading costs have certainly compressed to just a fraction of prices paid for stocks, with many popular retail trading services bringing their commissions down to zero. But not all costs are commissions.

All buyers would like to buy (bid) for less than sellers would like to sell (offer). The difference between these bid and offer prices is called the spread. When you buy or sell a stock with a market order, you also cross a spread. For many liquid stocks, spreads are fractions of a percent. But some smaller or less-traded stocks can have wider spreads, and possibly not enough shares. When that happens, market orders may trade at even higher prices too, until there are enough sellers to match your order size.

Crossing spreads increases the price you pay for a stock. For those trading frequently, the costs of crossing spreads can add up.

In contrast, investors using limit prices to join other buyers at the bid will need to wait in line for a seller to trade with them. Sometimes a more urgent buyer will instead lift the offer and you’ll need to increase the price you need to pay to remain in the market. Sometimes it can cost even more than buying the stock at the offer in the first place.

There may be other less explicit costs too, like different interest rates for cash balances than loans, management fees for ETFs, or financing and hedging costs included in options prices.

Trading may be easy, but successful investing is hard

It’s important to remember that stock markets are filled with many sophisticated and experienced investors. That often works in Main Street investors’ favor, as it means assets are reasonably accurately priced and spread costs are low. But the fact that even professionals have to work hard to beat the market should limit the expectations for new investors.

For example, a recent study found that professional traders were less likely to cause price bubbles, and understood trading strategies better. Other studies have found that individual investors often trade too much, or at the wrong times in the cycle, harming their returns.

The reality is that although investing is easy to do, it is hard to do well. We welcome new investors to the market, but encourage them to use the resources available to avoid common investing pitfalls. If we can do that, the U.S. equity market will be more vibrant and more liquid as a result.

Hedge Fund’s Mid-Year Trends and Strategies Currently In Demand

The hedge fund industry is dynamic, comprising numerous strategies that attract varying degrees of interest over time. Demand for each strategy is impacted by many variables including capital market valuations, expectations of economic growth, market liquidity and risk appetite among others. Industry professionals spend a great deal of time analyzing these variables in order to identify which strategies they believe offer the best opportunities for outperformance. In this paper, we share some data and thoughts on where investors are focusing their time and resources starting with a brief overview of developments year to date.

2020 has been one of the most volatile years for the capital markets over the past century. The year began with questions looming about the sustainability of the seemingly ever-rising equity markets. That uncertainty accelerated dramatically at the end of the first quarter. Equity and credit markets experienced material market value declines in response to the expectation of a sharp economic stall instigated by COVID-19. Generally, most hedge fund strategies performed in line with investors’ expectations. Still, some less liquid fixed income strategies that were not properly hedged sustained large, unanticipated, drawdowns leading to large redemptions. In some cases managers imposed gates and suspended redemptions. A flight to quality by investors combined with a disproportionate amount of time required to address fund “blow ups” resulted in the postponement of the majority of new hedge fund allocations.

Entering the second quarter, the response of central banks around the world, in the form of massive monetary stimuli, drove nearly immediate, strong recoveries across the global capital markets. As a result, a large portion of world sovereign debt is trading close to 0% at mid-year. Concurrently, most equity markets are trading at valuations well above their historical averages, by the belief that monetary stimulus would result in a quick rebound in economic activity.

As the summer comes to a close, many of the drivers of volatility remain unchecked including the spread of Covid-19, the US trade war with China, the US election and massive increases in global debt. The big question is, how are investors processing these uncertain variables and what is the impact on their investment thinking?

One way to address this question is to ascertain which strategies are attracting current investor interest. As of last week, nearly 300 “approved” investors are registered to participate in the upcoming Gaining The Edge – Global Virtual Cap Intro event. In the registration process, they completed a detailed survey about what type of strategies and managers they are interested in meeting. Of the investors completing the survey:

33% are institutional investors(including large pensions, endowments, and foundations);

9% are advisors and OCIOs;

36% comprise family offices, multi-family offices, and high net worth individuals;

22% are funds of funds.

We believe this survey contains high quality data and provides an accurate depiction of current demand across the hedge fund industry. This is both a function of the composition of investors participating in these surveys and that these preferences will be shared with hedge fund managers as part of the meeting scheduling process.

From the survey data, we share the following observations:

Investors were first asked to list their current strategies of interest. Long/short equity captured 65% of respondents, the largest share among all strategies. This indicates a positive change in investor sentiment regarding a fund manager’s ability to generate alpha in stock selection. Long/short equity has been losing market share for a number of years in the hedge fund industry and this data suggests a potential reversal of that trend.

Multi-strategy and event driven showed the second highest level of interest at (57%). This was followed closely by equity market neutral (54%), global macro (53%), special situations/specialty financing (52%), distressed (51%).

The increased interest in global macro, compared to a few years ago, indicates investor confidence that this strategy can take advantage of the increased volatility. More importantly this increase, along with the high level of interest in equity market neutral strategies, further supports the trend of increasing demand for strategies that are uncorrelated to the capital markets. Driving this trend are a combination of reducing portfolio tail risk and institutions shifting assets away from low yielding fixed income to a diversified portfolio of uncorrelated hedge fund strategies in order to enhance returns. Other strategies that will benefit from this trend include relative value fixed income, short term CTAs, and reinsurance.

The interest in distressed and special situations shows an increased willingness by investors to consider less liquid strategies along with a blurring of the lines between hedge funds and private equity as investors consider both structures to access these strategies.

A few niche strategies that are beginning to gain interest include cryptocurrencies at 21% and cleantech/Impact investing at 29%. Below is a full breakdown of the survey results.

Strategies of Interest:

Asset Based Lending (ABL)

31%

Cleantech / Impact Investing

29%

Convertible Arbitrage

40%

Cryptocurrencies

21%

CTA / Managed Futures

30%

Distressed

51%

Emerging Markets

49%

Equity Market Neutral

54%

Event Driven

57%

Fixed Income

43%

Global Macro

53%

Long / Short Equity

65%

Merger Arbitrage

36%

Multi-Strategy

57%

Options / Volatility

38%

Private Equity

33%

Quant / Stat Arb Strategies

42%

Real Estate

24%

Reinsurance

24%

Short Bias

20%

Special Situations/Financing

52%

Structured Credit

43%

Other

14%

In addition to indicating strategies of interest, investors were also asked to indicate the minimum fund size to which they would consider making an allocation. Of the respondents, 41% would consider new fund launches and an additional 23% were open to funds with less than $100 million. 32% of investors said they would consider funds between $100 million and $1 Billion and only 4% said they required a fund to be $1 billion or bigger. They were also asked about the minimum length of track record with 43% willing to invest with less than a one year record and 71% less than a 3 year record. These results were somewhat surprising, considering institutional investors represent almost one-third of those participating in the event (and this survey). However, this data confirms other indications that the minimum asset requirement for various investor types has declined over time and especially in the past several years. This may be, in part, attributable to the significant investment large pension funds have made into improving their internal processes. A majority have built out their research staffs and, in so doing, have increased their confidence and comfort with investing in smaller and emerging managers.

As we head into the 4th quarter, we anticipate an increase in hedge fund allocations due to pent up demand from earlier in the year. This survey should provide good guidance on the strategies to which assets will flow.

Additionally, as most investors and managers have become comfortable using Zoom and other virtual meeting providers, most will adopt this technology as part of their ongoing due diligence process. It will likely become a highly used tool to facilitate introductory meetings. In some cases, as we have already seen, investors may use virtual communication to facilitate their entire due diligence process.

Gaining the Edge – Global Virtual Cap Intro Event to benefit at risk youth is expected to be one of, if not the largest, virtual cap intro events in the industry. If you would like to see more information on the event please visit: https://www.agecroftpartners.com/virtual-cap-intro-2020

About the author

Donald A. Steinbrugge, CFA – Founder and CEO, Agecroft Partners

Don is the Founder and CEO of Agecroft Partners, a global hedge fund consulting and marketing firm. Agecroft Partners has won 38 industry awards as the Hedge Fund Marketing Firm of the Year. Don frequently writes white papers on trends he sees in the hedge fund industry, has spoken at over 100 hedge fund conferences, been quoted in hundreds of articles relative to the hedge fund industry and has done over 100 interviews on business television and radio.

Don is also the Founder of Gaining the Edge LLC that runs the annual Hedge Fund Leadership Conference, the Hedge Fund Educational Webinar Series and the Global Virtual Cap Intro Events. Most revenue from these events are donated to charities that benefit at risk children, which have total over $2 million donated since 2013.

Buyer’s Guide: Fundamental Review of the Trading Book Compliance Solutions 2020

This report assesses the functional capabilities of nine technology vendor solutions that can be used by investment banks and other types of sellside firms to achieve compliance with the Basel Committee on Banking Supervision’s Fundamental Review of the Trading Book regulations.

This report reviews nine of the leading, vendor-provided FX e-trading solutions utilised by the investment banking industry in 2020.

Since 2017, long-running changes to the structural dynamics of the cash FX market in which principal-based, voice-centric processes and workflows were steadily replaced with agency-focused, algorithmically-automated business and trading models, which affected different segments of the investment banking industry in different ways.

This report looks at the implications and knock-on effects for sellside institutions in light of significant changes in the cash equities trading platform vendor landscape. Combined with secular changes to market structure that imperil traditional sellside execution franchise business models, changes in the platform vendor landscape induce a large number of sellside franchises to revisit both their long term business strategy and the associated technology requirements. This report supports these franchises to develop a robust technology change practice by highlighting key functional and non-functional areas of cash equities trading platforms for both current and medium-to-long-term needs.

This report examines the change in the structure of the global flow FX marketplace as it continues to shift away from the historic prevalence of the dealer-to-client and dealer-to-dealer modalities familiar to investment bank broker-dealers and their buyside firm clients and counterparties. In place of the old structural paradigms, an all-to-all structure emerged completely for the first time in 2019 as the majority of spot FX trade execution volume was done on an automated basis, according to GreySpark analysis of the Bank for International Settlements 2019 Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter Derivatives Markets.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.