The competition for Borsa Italiana is intensifying with pan European stock exchange group Euronext confirming it was in talks with the equity arm of Italian state owned bank Cassa Depositie Prestiti (CDP) to submit an offer to acquire the Italian bourse from the London Stock Exchange Group.

It has been reported that Italian bank Intesa Sanpaolo has also teamed up with CDP to safeguard Italian interests in the Milan exchange, while other Italian investors are set to join.

The proposal is for CDP to take a stake of around 8% in Euronext, equalling that held by French state investor Caisse des Depots et Consignations. In addition, it has been mooted that Intesa would get a smaller slice of about 2%.

This week Italy’s Finance Minister Roberto Gualtieri held talks over the future of the Italian bourse with Euronext CEO Stephane Boujnah in a private meeting in Rome.

The LSE, which bought the Italian group in 2007 for €1.6bn, said in July that it was in exploratory talks to either sell the MTS bond trading platform, or the entire group, in order to gain approval from the European Commission for its $27 bn acquisition of data provider Refinitv.

The EU’s antitrust regulators expressed concern in June about the dominant market share of the combined company’s trading of European government bonds because both MTS’ trading venue and Refinitiv’s Tradeweb are already market leaders.

The Borsa generated about 14% of the LSE’s earnings last year and is a key entry point for the London’s exchange into Europe post-Brexit.

The Italian Ministry of Economy and Finance, who owns the majority of CDP, is thought to be in favour of the deal with Euronext but it will face opposition from Switzerland’s SIX Group and Germany’s Deutsche Börse, both of whom are thought to be preparing to launch their own respective bids.

SIX became Europe’s third largest stock exchange operator by revenues after completing a €2.57 bn takeover of Spanish rival BME earlier this year.

As environmental, social and governance (ESG) criteria becomes more important, the International Organisation of Securities Commission (IOSCO) said it is looking to produce a set of global uniform sustainability disclosure standards.

The disparate definitions and guidelines have long been a problem but the increasing popularity of ESG funds among institutional and retail investors is putting pressure on asset managers to factor in sustainability risks when analysing existing and potential investments.

In addition, ESG ratings attracted scrutiny in the UK recently following revelations that fast-fashion retailer Boohoo had positive ESG ratings from MSCI and others despite being accused of poor working practices.

Speaking at an Investment Sustainability and Responsible Investment Virtual Conference, IOSCO secretary-general Paul Andrews said that the “plethora” of sustainability frameworks gives companies a multitude of choice in terms of what ESG risks they report. This makes it difficult to compare one set of company ESG disclosures with another, he added, meaning there is “no common definition of what a sustainable finance product is.”

IOSCO has been seen to be slow in grappling with ESG issues but the regulatory body has stepped up its pace over the last 18 months. In April, it released an extensive report looking at sustainability in finance which identified three key challenges: lack of ESG data and disclosures, greenwashing and how investment managers use ratings, sustainability standards, and make their disclosures.

More recently, IOSCO created a taskforce, which as Andrews notes is “to pick up the themes we have identified, We are going to try to get at the issue of disclosures and try to find a way to harness various different disclosures into something cohesive, more transparent, and hopefully more standardised. We believe it will be a huge value-add to the industry at large.”

Andrews said the task force will work to translate the different standards from around the world into “a more cohesive, more transparent and more standardised” form. The aim is to devise a set of guidelines that are principles-based yet “granular enough to be meaningful”.

As a standard setter, IOSCO’s output will not be legally binding, but it could influence the direction of future rulemaking as global policymakers enter the race to develop their own ESG rule books.

Aquis Exchange announced a 42% hike in revenues to £4.9m in the first half from £3.4 m during the same period last year and recorded a profit for the first time with an after-tax result of £16,000 versus a loss of £623,000 loss in the first six months of 2019.

The UK based exchange reported EBITDA of £0.54m against a £0.18m loss in the first half last year.

Alasdair Haynes, chief executive officer of Aquis, says, “We are pleased to announce our first period of profitability, reached through further strong revenue growth. This growth has been driven by our existing members continuing to increase their trading volumes through our pan-European lit equities market.”

Haynes notes that while volatility boosted volumes, the exchange also benefitted from a resilient and strong infrastructure and technology that was able to handle the additional activity.

Haynes adds that the completion of Aquis Stock Exchange, formerly NEX Exchange, was a “milestone for the Group and marked a significant step towards achieving our ambition to become the leading exchange services group in Europe. We have now entered the primary listings market, with exciting plans in motion to further build AQSE into the first choice for quality growth businesses.”

Aquis, which operates a pan-European cash equities trading business and provides exchange software to third parties, finalised the acquisition of Nex from CME Group in March.

Haynes says the objective is build an exchange at all levels, starting with growth businesses at the sub-£10mln market cap at the early-stage Access market, before moving onto the Apex market as they mature and then onto the AQSE Main Market.

At each stage of the journey rules support would be different, reflecting the fact the “requirements for a £4m, £400m and £4bn company are totally different,” he adds. “Great companies do start small, they grow and they ultimately mature and we want to support them at each stage.”

The rest of the year will also see the exchange continue to segment the market, gain greater institutional and asset manager support, prohibit short selling and enhance trading mechanisms

As for its results in the second half, Aquis says that current trading is in line with market expectations for the full year, although the Group recognises the volatility of licensing contracts and their timing in this climate and their potential effect on revenues.

By Henry Marriott, Vice President, APAC AES Systematic Coverage, and Nicole Kim, Vice President, APAC AES Sales, Credit Suisse

Problem Solving 101

Henry Marriott, Credit Suisse

Let’s admit it. We are willing information addicts, reluctant to admit that the constant information overload is simply exhausting. One has to wonder whether this perpetual state of overload is in fact helpful or harmful to our problem solving and decision making processes. So then, what are the steps involved in solving a problem? First and foremost, defining the problem is of course paramount. This is also the most crucial step as it involves asking the right questions to capture the essence of what you want to achieve and to understand your ultimate goal. Then comes the gathering and processing of all of the relevant factors for consideration, before finally sifting through the data to reach a robust answer.

No matter the number of steps involved, it should be stressed again that the most important step lies in asking the right questions. The evaluation of your answer will also heavily depend on getting this first step right. If you don’t even know where you want to go, how will you know whether you’ve reached the right destination?

Importance of Objectives: Lessons from the Plant vs. Meat Diet Debate

Nicole Kim, Credit Suisse

Think about the sheer amount of time, thought, and effort we expend on the problem of what to eat, every day, three times a day (usually). It is no wonder then, that the debate of the plant vs. meat diet has garnered such interest over the years as a topic that speaks to all of us.

The gathering and processing of all the relevant factors to consider for this debate is no easy feat. The complexity behind this seemingly simple topic is compounded by the countless studies and data points that continue to emerge, each defending their merit. From a health perspective, both vegans and meat eaters will argue that their approach is healthier. Some vegans believe meat causes cancer and destroys the planet. But meat eaters will argue that giving up animal foods leads to nutritional deficiencies. We have just looked at the health aspect of the problem, but what if we threw in more elements into the equation such as environmental impact, ethics, religion, cost efficiency, and individual taste? This is where establishing the objective becomes critical. What exactly are you trying to achieve from solving this debate?

We are by no means trying to propose a definitive answer. But we do want to emphasize that depending on what you wish to achieve, that answer may differ hugely. Quick and effective muscle gain could nudge one towards the meat-eater camp while environmental impact could have you with the plant-based dieters. Cost efficiency could swing you yet again to the other camp while taste could do the opposite. Again, the emphasis here is the importance of knowing your objective when solving a problem, as this will serve as a beacon plotting a path for you towards the answer.

Best Execution – Please Explain This to Me!

This same emphasis should also apply to our industry’s quest to solve the problem of Best Execution. We have yet to accurately define this concept beyond beating the VWAP or Arrival benchmarks. The reality is that Best Execution lacks a discrete objective, which is also why we are all over the map in our attempt to solve this problem, and why we also lack a means of definitive evaluation.

We should take pause and wonder, are we asking the right questions? Do we even know what we want out of Best Execution? Going back to the problem-solving sequence, knowing your objective ahead of solving a problem is critical. Thus, viewed in this light, should we not consider aligning Best Execution with each order’s investment objective?

Order Placement Process

The Investment Process, as a whole, is not something that brokers typically concern themselves with, but we are certainly aware that there is a lot going on behind the orders we receive. Indeed, idea generation, research, and establishing investment objectives all come before the placement of an order. However, generally speaking it has become accepted that the elusive solution (if it exists) to Best Execution sits within that Order Placement Process, and this is where the brokers come in.

Not so long ago, the Order Placement Process was relatively straightforward: a PM would deliver an order to a trader with instructions relating to their intention, and the trader would then select an algo to use based on an understanding of the investment objectives. This execution process was tightly coupled with that intention.

Over time, in trying to achieve Best Execution, mechanisms such as the Wheel have been introduced to remove subjectivity and improve efficiency. Now before we receive an order, a lot more is happening. A PM can send an order to a trader as before, or into a Wheel. The trader can send the order to us, or they can place it into a Wheel. Is the ticket we receive from a trader (or Wheel) the same size and price as the original order released by the PM? How is the Wheel configured? Taking it a step further, individual orders are not necessarily generated by a person at all, rather a quantitative model may generate orders autonomously which could then be routed via a Wheel-like process to brokers.

With this extended order placement workflow, brokers can still assess order characteristics (e.g. size, %ADV, mid/large cap) and market conditions, information no doubt valuable for execution. Yet, in our attempts to eliminate inefficiencies, each step and decision introduces separation, and information about the original intent is lost. And if the Investment Objectives do not readily inform the Execution strategy, what does that mean for assessing Execution performance, for example by using TCA?

How much does TCA reflect Execution Performance from the trader/PM’s standpoint?

Typically, TCAs are presented using benchmarks such as Arrival and VWAP – these are fairly straightforward, but in isolation they can only tell us what has happened for the duration of the order.

In the below chart we attempt to add some perspective to these metrics. We combine all of the trades done by each individual trader (for a single client firm) over a specified time period (e.g. a whole quarter) and plot these lines showing the average price move before, during, and after trades are executed.

To reiterate, this chart shows what transpired on average over an entire quarter, so we all but remove random market conditions as a probable cause for the variation in results. So what is going on? The algo did not just behave differently for each trader, but the results clearly differ.

We as brokers can only infer that there are varying underlying strategies precipitating these orders, and then try to draw a path back to that original intention. We could compare algo performance in each scenario in isolation (e.g. by looking at participation rate to try and ascertain whether we are looking at alpha or impact), or we could suggest that there appears to be momentum, or reversion and then make a suggestion. But what if the individual is trading for multiple strategies and/or PMs? What if they just have operational constraints? With context, TCA can be assessed in a more meaningful manner and we are far better placed to provide significantly effective execution advice beyond raw algo performance and optimization.

Align Execution Approach with Investment Objectives

Using TCA or otherwise, we need to expand the dialogue between the buy and sell-sidesin order to reconnect the Investment Objectives with the actual execution of the order.

Under the current framework, we often do not know if a ticket we receive is a short-term, stand-alone alpha based trade, or part of a larger, multi-day order to establish a large position with a long time-horizon. If we received two equally sized orders in the same stock at the same time, but in addition we knew those two different objectives were behind each order, our execution approach could differ hugely. Our clients can provide some insight into what they are trying to achieve by giving us a benchmark or assigning an urgency to an order, but this isn’t actually an objective – it is just a proxy for the objective of the investment strategy. As a result, where there is room for some discretion away from a scheduled instruction such as a VWAP basket, brokers have tended towards ‘smart’ spread-capture strategies that are largely intention-agnostic, precisely because we are somewhat unaware of the true intention behind the orders we receive.

In the world of algo trading, the final part of the Investment Process, order execution, is outsourced to brokers with more technology and processes in between than ever before. Brokers can continue to work on a single important factor of Execution, such as optimizing algo logic; however, similar to the Plant vs. Meat example, they are somewhat limited in their ability to contribute to Best Execution without knowledge of the investment objectives. We need to establish the right questions that need to be asked so that trades are put in the context of the overall intention. This is crucial in the mutual goal to execute orders in the most efficient manner, thus truly achieving “Best Execution”.

By Winter Chan, Head of Trading Technology APAC, J.P. Morgan Asset Management, and Co-chair APAC Technical Committee at FIX Trading Community

Winter Chan, J.P. Morgan Asset Management

COVID-19 has brought a totally different dynamic to how the world approaches work, and it has made many firms think about buy-side trading operations from a different perspective.

As equity traders, we have all had to reconfigure how technology and communications work in the absence of a typical ‘trading room’ setting. We’ve reimagined how we work while critically maintaining our ability to run processes with all the same speed, efficiency and efficacy, to enable us not only to continue to serve investors without interruption, but also to capitalize on the volatility that these disruptions have created. The key focus throughout has been on operational resilience and adaptive flexibility, made possible by years of infrastructure investment long before the onset of the global pandemic.

An example of this can be found in just how rapidly the trading function itself evolved since COVID, as working from home suddenly became a norm in much of the developed world in March and April of this year, and in Asia somewhat before that.

Certain trading functions were previously considered too difficult to operate outside of the traditional trading room. Equity buy-side trading teams such as ours drew on what had been a long history of well-established investment in technology infrastructure to recreate the controls and processes necessary to enable remote replacements for physical trading floors. This included leveraging advanced electronic trading whilst applying solid cyber security controls.

Working from home hasn’t stopped us from progressing with our business priorities and improving the trading desk’s global workflows. In order to make progress we’ve started with the tasks and activities that could be most easily accomplished, such as pre-existing structured flows on the desk. We’ve then moved on to tackling less structured and more nuanced and complex workflows.

For trading orders that are generally simpler and easier to execute, we’ve engineered effective ways to automate those workflows by leveraging data analytics and machine learning techniques. This enables our traders to focus on more value-added work with more costly, less liquid workflow.

The ultimate aim for trading technology teams has long been to work towards a globally consistent workflow, as well as to try to simplify what is often a complicated implementation process by continuing to invest in new technology solutions. Trading via China’s Stock Connect is a good example – it used to be a complicated implementation process because of the same-day settlement and pre-funding model, but with support from tech changing settlement instruction generation to brokers, we are able to take a layer of cash management and complexity out of the workflows.

With or without COVID, we focus on external collaboration, including enhancing communication across various channels, to help make our ever-increasing interactions with the sell side less bespoke and more scalable, whilst achieving the quantitative workflows the traders are looking for.

We believe there are three key aspects of successfully operating on secure and financially compliant messaging platforms such as Symphony and Bloomberg.

First, we are building interactions with the sell side via these systems to facilitate quantitative decision making. For example, our proprietary model that assesses indication of interest (IOI) quality is linked into our systems and has the potential to automate or semi-automate some of this flow.

Second, we are focused on searching for and sourcing enhanced liquidity. Similar to the above, this allows our traders to send our IOI selectively to brokers who may be best-suited or most efficient to execute the given trade. This allows our traders to take advantage of the power of our internal models to build structure around a key part of our liquidity landscape — another big step to a more quantitative approach to high touch workflow.

Third, we are exploring the use of Symphony as an open communication platform. We are doing this by working with the brokerage community to come up with innovative workflow solutions for two-way interactions via chatbots, so they can be leveraged by our traders and models. There are many different use cases that have developed, and these have become especially useful when workflows are structured, allowing them to empower trading decisions and supplement trading information.

Thus far COVID-19 has not compromised our ability to deliver on our vision, thanks in a large part to a multi-year investment in infrastructure as well as to the long-term trust we have built with our trading partners. This trust has been founded in delivering quantifiable outcomes and in a strong shared understanding and collaboration, facilitated initially by co-location next to them in the office over the last few years, which has transferred well to a remote working environment.

The modern practices we utilize around the application development lifecycle have also put us on solid ground as we have adapted and altered our working practices. Although the future is unclear with respect to the virus, firms with long-term commitment and investment in technology and infrastructure will be best-positioned to cope with ongoing COVID disruptions while still seizing new opportunities and maintaining efficiency.

By Dr Robert Barnes, Global Head of Primary Markets & CEO Turquoise, London Stock Exchange Group

2020 is the year electronic block trading at midpoint became mainstream via Turquoise and London’s capital markets remained open during the extreme conditions of H1.

PRIMARY MARKETS

Authorities including the Financial Reporting Council (FRC), the Financial Conduct Authority (FCA), the Bank of England’s Prudential Regulatory Authority (PRA) as well as infrastructure providers such as London Stock Exchange have implemented a range of temporary measures to give listed companies extra flexibility while retaining an appropriate degree of investor protection.

Dr. Robert Barnes, LSE Group

A good example of this has been the relaxation of Pre-emption Group Principles, supporting non-pre-emptive issuances by companies of up to 20% of their issued share capital (ISC), rather than the 5% for general corporate purposes with an additional 5% for specified acquisitions/investments.

Capital raising has happened quickly – often taking about one week.

Executed in an orderly fashion, since 1 March, discounts to last close for transactions above £5m have averaged 5.3%. Accelerated bookbuilds of some companies – such as ASOS, SSP and AutoTrader – were raised at a slight premium.

From 1 March to 14 August 2020, 311 transactions announced on London Stock Exchange raised £21.5bn, from £5m to £2bn each, highlighting the sheer range and scale of capital available in a very short time. Average price performance for deals above £5m+ for the period stands at +6.3%.

Retail has a new route for raisings.

London Stock Exchange has a partnership with PrimaryBid, the fintech platform that enables retail investors to access capital raisings on the same terms as institutional investors. This includes multiple placings over recent months including FTSE 100 constituent Compass Group’s £2bn capital raise.

Higpnosis Songs Fund became the first FTSE 250 fund to use PrimaryBid in its recent July 2020 transaction that brought its aggregate capital raised to more than $1 billion since listing on London’s Specialist Fund Segment in July 2018 then transferring to the Premium Segment of the Main Market in September 2019 with multiple fundraisings supported by investors.

London is where the world’s largest issuers and investors come to get their business done.

In 2019, London Stock Exchange was privileged to be selected as the sole Primary Market for the first public bond listing by Saudi Aramco. Its landmark bond issuance raised $12 billion with books reflecting demand via London of more than $100 billion.

In the first half of 2020, London Stock Exchange Group’s equity and fixed income markets helped issuers raise $722 billion: $388 billion on London Stock Exchange via $358bn in bonds plus $29.7bn in equity IPOs and Follow-Ons, and $334 billion on Borsa Italiana via $330.2bn in fixed income plus $3.8bn in equity. On 17 June 2020, China Pacific Insurance Company (CPIC) became the next successful Shanghai-London Stock Connect listing with a capital raise of $1.8 billion.

Sustainability

Companies can deliver a public good whilst supporting economic growth and wealth creation. Calisen came to market 2020 with the Green Economy Mark and a valuation of £1.3bn at IPO. Our Green Economy Mark issuers in aggregate have outperformed the FTSE All-Share Index over the past two years by 36%.

SECONDARY MARKETS

A key innovation of market structure has become mainstream in 2020.

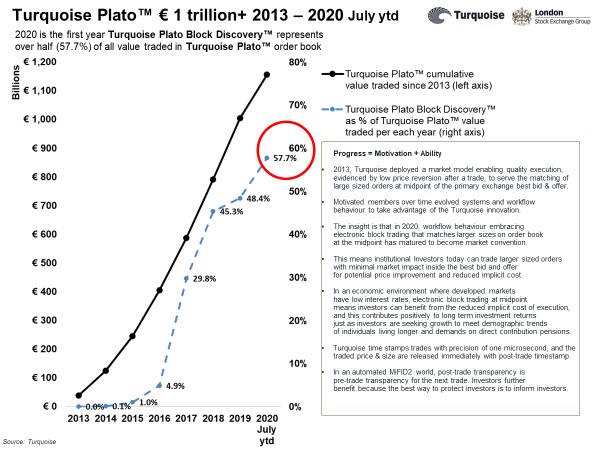

The industry leader for midpoint and electronic block trading as single order book dark pool for matching UK and European equities is Turquoise Plato™, according to independent analysis published by Rosenblatt Securities.

Figure 1. Since 2013, members have matched more than €1 trillion of equities via Turquoise Plato™. 2020 is the first year that Turquoise Plato Block Discovery™ represents more than half (57.7%) of all value traded in the Turquoise Plato™ order book. The insight is that electronic block trading at midpoint has matured to become a mainstream market convention.

Figure 1.

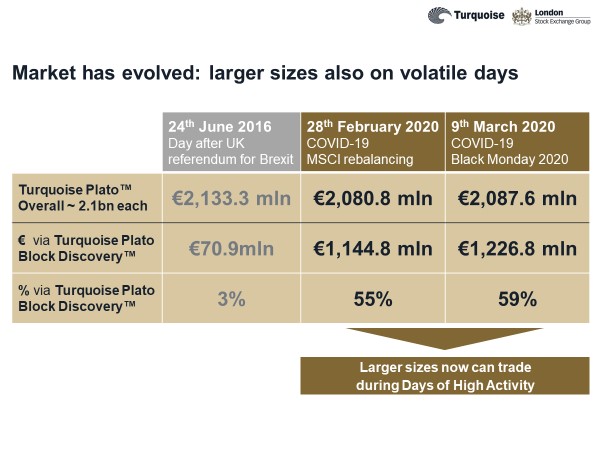

Figure 2. shows this is true even during record days on Turquoise Plato™.

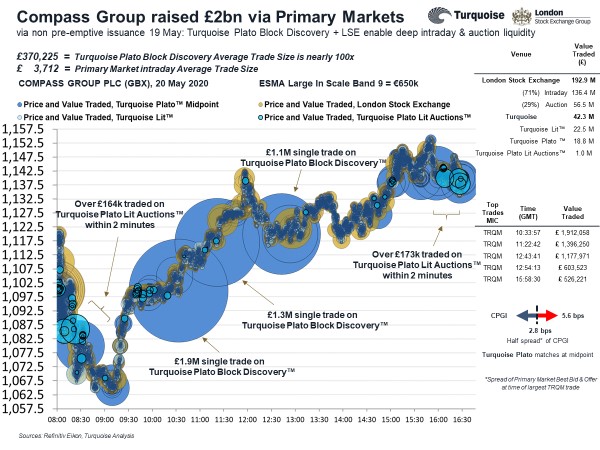

Figure 3. This chart shows Compass Group plc on 20 May 2020, the day after successfully placing £2bn via non pre-emptive issuance 19 May, including retail participation up to €8m via Primary Bid.

A feature of Exchanges world-wide is small average trade size. While many small trades can sum to large value, investors placing large orders into such an environment risk significant market impact to the detriment of an investor’s long-term investment returns.

The closing auction of an Exchange, however, can be a significant liquidity event – 29% of London Stock Exchange order book value for Compass Group on 20 May. Active asset managers also appreciate the ability to trade larger orders earlier in the day, and this is possible using Turquoise for midpoint and electronic block trading that minimises market impact and offers potential price improvement. For Compass Group on 20 May, its £370,225 average trade size on order book via Turquoise Plato Block Discovery™ is around 100x that of the primary exchange’s £3,712.

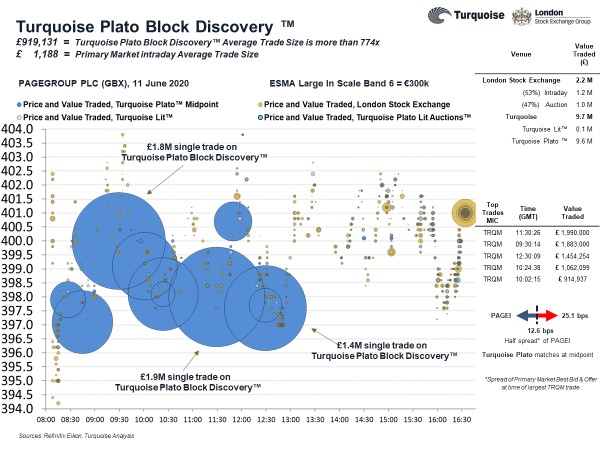

Figure 4. PageGroup plc has a small intraday liquidity profile. On 11 June 2020 turnover on London Stock Exchange is £2.2m including £1m via auction. Turquoise Plato™ enabled Investors to trade an extra £9.6m intraday, at midpoint saving significant implicit cost and market impact. The £919,131 average trade size on order book via Turquoise Plato Block Discovery™ is more than 774x that of the primary exchange’s £1,188.

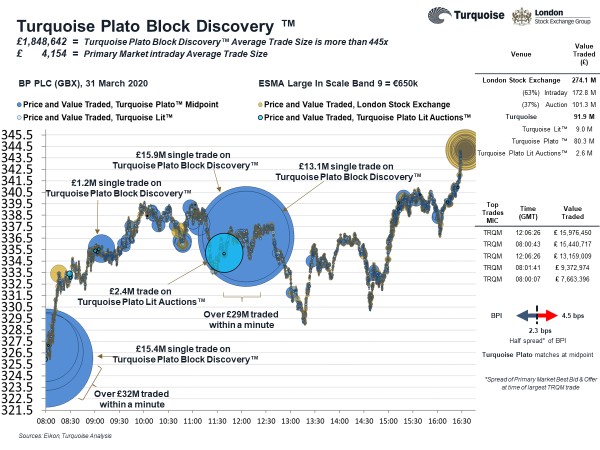

Figure 5. shows BP plc trades of London Stock Exchange and Turquoise, including Turquoise Lit™, Turquoise Plato™ dark pool, and frequent batch auction mechanism Turquoise Plato Lit Auctions™.

The £1,848,642 average trade size of Turquoise Plato Block Discovery™ is more than 445x that of the exchange’s £4,154 on 31 March 2020. The largest sizes measured were more than £15 million per trade, multiple blocks recording more than £32 million early morning plus £29 million at midday – rising above £31m if one also includes the adjacent £2.4 million via Turquoise Plato Lit Auctions™.

With Jessica Morrison, CEO and Head of Execution Services APAC, Virtu Financial

Briefly discuss the career path that led you into finance?

Jessica Morrison, Virtu

I never intended to get into finance; fine art and sculpture was the original plan. Becoming a single mum at 21 was the driving force behind going back to school first to take ‘A levels’ (UK) and subsequently securing a place to read Law at the University of Cambridge. Once there, I went to the standard ‘magic circle’ law firm recruitment drives, with the idea of getting a training contract in London. In 2002 there were few senior women in law; trainees worked 70+ hour weeks and slept in beds in the basement. When I raised that I needed to be home to care for my daughter, I was told that a career in top-tier law firm was not going to work, and I should try academia or teaching.

However, the careers office at Cambridge was excellent. When I asked them how I could earn money, they suggested banking to which I replied that being a cashier sounded dull, sitting behind a glass counter all day. That was about as much as I knew about finance. The careers office explained there was a bit more to it and helped arrange two days on a spot FX trading floor to see for myself. The first day was September 10, 2001 and I was asking “What’s a bid? What’s an offer?”. Day two was September 11.

Horrific as the events were, the connection between the real world and the markets really hit me. The pace at which things change makes it one of the most dynamic industries. The markets are ultimately a reflection of collective psychology as much as statistics and probabilities. There is blind optimism, fear, panic and stubbornness — particularly where there is high retail participation.

My first job was in Equity Compliance at Morgan Stanley, and then I moved to Deutsche Bank in 2009. In 2011 I moved to Hong Kong to set up the market structure product within equity trading before returning to MS in 2017 as Head of Execution Services Sales, crystalizing the link between content and revenues.

In June this year, I started as CEO for Virtu Asia Pacific with primary responsibility for Virtu Execution Services. Although still early days, it is exciting to join a firm that puts data and technology at its core to create scale and efficiency. There is huge potential to perform meaningful analysis on microstructure and externalise it for the benefit of clients through the algo strategies and explicit content. I am excited to see what the future brings.

What has been your experience as a woman in an often a male-dominated field?

I don’t know one senior female who has not been called emotional, sharp-elbowed or told they talk too much. I remember one heated discussion when a man told me – in a pretty emotional way — that I was getting emotional. My boss said “She’s passionate, at least she cares. You could learn something from that.” Men can both try to put you in a box but equally can be your best back-up.

A female spot FX dealer gave me some sound advice in the early days, saying something to this effect:

If you want to be known for your professional reputation rather than your love life, be sensible about the situations you put yourself in. Breakfast and lunch can be better for one-to-one meets, for evenings (where there will likely be alcohol and inhibitions are lowered), have group events. Similarly, the way you dress. While we should all have freedom of expression, think about the image you want to project. Are you in a nightclub or on a trading floor? Are you coming to the office to find a boyfriend or to work?

Who has been the most influential for you in your career?

Having a strong network of female friends in the industry, be it clients, competitors or colleagues, has been a great inspiration, support and comfort. We share experiences and challenges which friends outside the industry may not understand. This network is essential and has seen me through life’s challenges.

To date all my managers have been male and I’ve been fortunate to work for men who have a strong interest in equal opportunities. I’ve noticed they all have daughters and they have made comments about wanting to create an environment where their daughters could thrive. Finding the right personalities to work for and with can make or break your role as much as your technical ability and work ethic.

Are there notable differences in being a woman in finance at the senior level compared with at the junior/middle level?

At entry level the statistics are now approximately equal between men and women. However, women seem to leave the industry before they reach management. So, as I started to attend management meetings in banks I would regularly be the only woman in the room.

To that end, there are more than 230 women at Virtu. This count is growing in terms of numbers and representation in senior management positions which span the firm’s global footprint and business segments — Virtu’s Board of Directors, through to product development and management, sales, strategic operations, support, infrastructure, networking and more.

What are the challenges/opportunities for women in finance in Asia?

As an expat, being far from home can be isolating. Having a strong network helps with this as others will be feeling similar issues. On the home front, Hong Kong has a great system of domestic care where child-carers live with you. I am not sure I would have been able to work the way I do if not for the two wonderful ladies who have lived with me and helped care for my two boys who are now seven and five.

How is Virtu in terms of supporting and encouraging women employees?

Ahead of this interview, we realised I may be the first female CEO of an agency broker in APAC – although the combination of the agency broker with one of the most successful liquidity providers globally is unique proposition in itself. This to me is a tangible show of their understanding that diversity makes for a strong business. In one of my early conversations with Virtu CEO Doug Cifu, he asked me what support I needed to reach my potential. That was also a first.

One of the more notable programmes that supports women and families, especially during this time of COVID-19, is the childcare subsidy that Virtu provides to all staff globally. Essentially the firm pays for employees’ childcare, and as a working mother I’ve found this benefit to be extremely helpful and reflects the character of our firm. The Virtu maternity policy in the US is four months’ paid leave, longer than many companies in our industry. We also have a partnership with Milk Stork, a service that helps nursing mothers with milk delivery when they are not with their young ones.

From a recruitment standpoint, the firm has put together a Women’s ‘Winternship’ which is becoming a great driver of female talent to the firm. We’ve also launched a Diversity and Inclusion committee to help attract and retain a more diverse workforce. I’m excited to see the initiatives ahead.

How do you strike a work/life balance?

Tough one. It is a demanding industry and I think mothers have a natural tendency to worry that they are not doing a good enough job with their children. I do also believe the example you set for your children as someone who gets up and works day in and day out is very valuable particularly as they get older and have their own life goals to achieve. Show them that anything is possible.

Of course, not everyone has children, and being disciplined in your routine is key to making sure you fit everything in. Making time for down time, regular exercise and some plain old fun is so important for everyone. Work-life balance is not just for parents. I would encourage everyone to take their mental health as seriously as they do their physical health and try to manage stress appropriately.

What is your advice for young women just starting out in finance?

Be open-minded to new opportunities that arise; don’t have too rigid a career plan as you could cut yourself off from something you never expected. Be confident in your views, because you are well-researched and open-minded. Seek out constructive criticism to find areas of personal growth, and don’t take feedback personally.

Two excellent TED talks: Brene Brown’s The Power of Vulnerability to motivate you to be brave enough to get in the ring; and Caroline Casey’s Looking Past Limits, a hugely inspirational story of a girl whose parents decided not to tell their daughter she was legally blind so as not to limit her.

What is the future of women in finance?

The statistics at the top are still hugely skewed towards men. It’s a tricky topic, as having a senior career in finance comes with buckets of hard work and a sacrifice of the time you could spend on other things like caring for small children. Personally, I would love to see talented women retained in any capacity when they have such life choices to make (maybe part-time or a different role) as coming back after a long break seems very hard despite the efforts made in re-entry programmes.

Hopefully with modern technology and the new work-from-home environment, more women will stay in the industry. We shall see!

When Covid-19 was pronounced as a pandemic FIS, the financial services technology provider, had 700 guests attending two events and had to get them back home immediately. Ellyn Raftery, chief marketing and communications officer, and the executive team had to devise a strategy for communicating with clients and also the firm’s employees around the globe.

Raftery told Markets Media that Gary Norcross, chairman, president and chief executive, communicated on a weekly basis including by video from his home and through letters.

Ellen Raftery, FIS

“Transparency was very important as our employees’ personal lives were changing dramatically so we sought to be a source of truth for them with updates from the company with consideration for local government requirements and a global view,” she added.

FIS has held table-top exercises on a regular basis, run drills and devised playbooks for potential business interruptions as the firm provides critical infrastructure to financial services.

“We had tested shifting systems between locations such as India, Manila and Milwaukee,” Raftery added. “Our performance was remarkable despite trading volumes increasing nearly fivefold.”

For example, she described FIS making an ‘extraordinary effort’ in India to get critical employees into the office to operate secure systems. The employees had to be cleared by the Indian government and FIS had to liaise with hotels and restaurants to arrange food and housing despite the lockdown.

One result of the pandemic has been the rise in remote working, which has led to increased demand for technology. For example, FIS’ own employees can work from home until the first quarter of next year.

Raftery said: “There has been a massive uptick from large institutions for outsourcing solutions going forward so we are helping clients implement the technology they need to move to the next generation environment including increasing automation.”

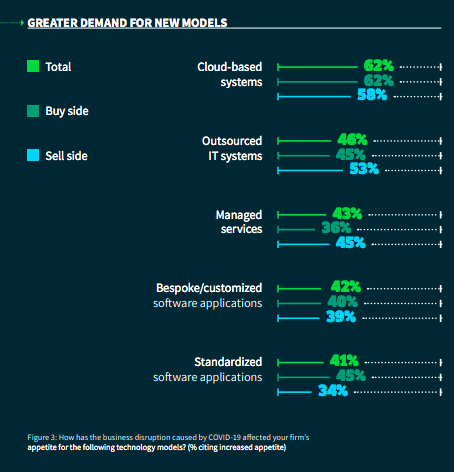

FIS carried out a global survey of 250 capital markets executives in June and found that the majority, 62%, said the disruption from Covid-19 has increased their appetite for cloud systems.

Half of the respondents, 52%, said they were prioritizing cybersecurity tools and 49% upgrades to trading systems, while only 40% were prioritizing client-facing systems.

Tony Warren, head of strategy at FIS Capital Markets, said in the report “We are seeing sustained demand for accelerating managed services, including business process as a service (BPaaS) and cloud deployments, reflecting the industry need for greater resilience, scalability and performance assurances going forward.”

Source: FIS

Warren continued in a blog this month that firms are turning to virtual and remote data delivery.

“By leveraging SaaS environments, the distribution of data becomes virtual rather than actual and eliminates the risk of a centralized workforce,” wrote Warren.

He added that with most employees still working from home, firms need a bigger commitment to compliance and risk.

“So, it’s not surprising to see that 46% of respondents are more interested in leveraging cloud-based solutions in this area, and 43% will prioritize investment and modernization around regtech in the next 12 months,” Warren said.

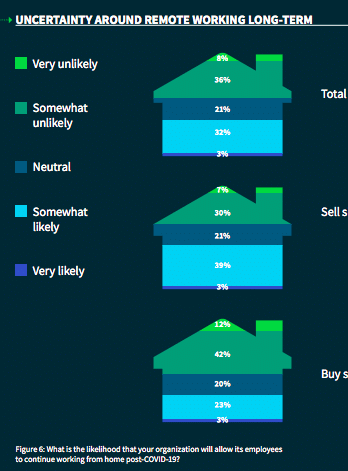

The survey also found that 26% of buy-side firms plan to let employees continue working from home after Covid-19, while this was higher for sell-side firms at 42%.

Source: FIS

Career route

Raftery joined FIS in 2012 from CA Technologies, the enterprise information technology software and service company, where she had been senior vice president of marketing. Prior to CA Technologies, Raftery had been chief marketing officer of Unisys and vice president of global strategic marketing at MarchFIRST.

“FIS is a high integrity company with a dynamic leadership that is focussed on client needs so it was also a great cultural fit for me,” said Raftery.

She continued that in the last eight years marketing has transformed from events and communication only into a full scale marketing organization including strategy and business intelligence, research, thought leadership and more – including a demand generation center that uses artificial intelligence.

“In my role I am also responsible for commercialisation of solutions and bringing forward the voice of customer,” Raftery added. “There is an art and science of marketing. There is a narrow view that the function is just about how things look and feel.”

She explained there is a a strategic opportunity in the role such as during the pandemic where marketing defined the voice of the company to the market and employees, helping to create and cultivate the culture.

Diversity

Raftery said it is hard for women to survive at the top level given the male-dominated nature of finance and technology.

“The fast-paced environment combined with personal responsibilities like being a mother too, makes trade-offs choices complicated,” she added. “You need a strong partner who supports your profession and the family.”

Today we celebrate Women’s Equality Day. We need to continue to push for change. By empowering ourselves to speak out, have our voices heard and owning our own abilities, collectively we will change the landscape of the future. #womensequalityday2020

She continued that FIS is focused on continuing to drive a diverse environment and recruiting more diverse candidates. The firm has programs such as unconscious bias training and is also reviewing it’s university scholarship programs and ensuring more scholarships go to black universities.

“Our chief executive has done a good job at appointing multiple women to the board and executive team,” she said.

Raftery’s advice to women is to own your destiny, make sure you always have a voice, to not be afraid to challenge and put ideas on the table and to never let someone block you.

“If you always act with high integrity and have the best interest of the company at heart then you will never do the wrong thing,” she said.

On a personal level Raftery would like to return to her art and is hoping that travel comes back.

She concluded: “On a professional level I am on a journey to expand the role and voice of marketing to evolve our strategic role as a part of commercialisation and innovation.”

By Chris Hall, Senior Correspondent, Traders Magazine

The list of topics ‘on the ballot’ is growing longer as political rhetoric ramps up ahead November’s presidential and congressional elections. One item of particular interest to traders – the financial transaction tax (FTT) – has been firmly on the ballot since all leading candidates for the Democratic Party nomination included it in their policy platforms. But the FTT could slip down the legislative agenda, even if Joe Biden can translate his poll lead over Donald Trump into electoral success in eight weeks’ time.

Prospects for an FTT have grown over the past decade, initially as a way to temper the rise of high-frequency trading (HFT) and its perceived risks. Electronic market-making is slightly less controversial today, as market participants accept its role in liquidity provision. But the economic impact of the Covid-19 pandemic has maintained momentum behind FTT. Rising inequality and unemployment, not to mention faltering government finances, are fueling the search for new sources of revenue.

Jim Toes, STA

“There is now a real threat to the industry,” said Jim Toes, President and CEO of the Security Traders Association.

Some proposals are modest, typically levying a 0.1% per-transaction charge, which the Congressional Budget Office says would generate $777 billion over a decade, or 0.5% of GDP. Others are more punitive; Vermont Senator Bernie Sanders called for a 0.5% FTT on stocks, less on bonds and derivatives. Most proposals are national, but some have been made at state level. New Jersey’s Democratic Governor has made headlines with favorable comments about FTT bills introduced to his state’s legislature in July.

This proposal would place a ¼ penny tax on every transaction executed within data centers located in the state, operated by the three major exchange groups, NYSE, Nasdaq and Cboe Global Markets. Critics argue the revenue raised would be diminished over time by reduced trading volumes or even relocation of the data centers.

A national tax would circumvent the latter risk but not prevent the former. According to Toes, a tax that targets HFT would reduce trading activity by electronic market-makers. “It could drive some market-makers out of the market. And the barriers to entry are now so high that they would not be replaced. Initially, these firms would first look to offset the costs of the FTT through wider spreads, offering less opportunity for price improvement, which would result in higher implicit trading costs to end-investors.”

The Futures Industry Association’s Proprietary Trading Group does not have an official position on FTT, but is understood to be less concerned about the direct impact on intermediaries than market quality. David Lewis, Head of Global Equity Group Trading at Franklin Templeton, said there could be serious knock-on impacts on prevailing business models and costs, even at low rates.

“With FTT proposals, the devil’s always in the detail. But even an FTT of 10 bps will add 20 bps to the cost of a round trip for an HTF firm, which would eat into their margins. One would expect their volumes to drop off and / or spreads to widen to make up for that margin loss. Ultimately those could get passed to the end-investor,” said Lewis. “Active investors have different time horizons, so the impact of an FTT on explicit trading costs is unlikely to make a significant difference to their daily turnover, but there may be challenges to business models in the retail brokerage and passive investment sectors.”

Transaction taxes are not new. Many other countries have adopted them, only to regret and repeal, notably Sweden. There are certainly not alien to the US. Some will recall Nobel-prize winning US economist James Tobin proposing a tax on currency payments in 1972 to curb destabilizing flows. Fewer will be aware that a small tax is already levied by the Securities and Exchange Commission.

Proponents point out the tax is progressive, in that the rich are hit hardest. But Keith Lawson, senior counsel for tax law at the Investment Company Institute, argues it is all but impossible to protect middle-class savers.

“Prior experience suggests the problems created by the negative impacts on retail investors are not solvable, partly due to the high administrative costs of any system of exemptions,” said Lawson. “These exemptions also significantly reduce revenue taken in, which tend to make FTTs less attractive to policymakers who fully examine the issue.”

This observation is supported by an analysis published last year by Vanguard, which estimated that even a 0.1% FTT would generate a substantial drag on investment returns, requiring the typical long-term investor to work an extra 2.5 years to achieve the level of retirements savings achieved absent the tax. Although the tax is small and most savers do not transact regularly, its compound impact across multiple investment activities soon mounts, with users of mutual funds and money market funds particularly vulnerable. An ICI analysis found that a 25 bps FTT could increase the cost of buying and selling stocks by 25-60%.

Evidence from other countries also includes wider bid-ask spreads, poorer liquidity levels and market quality, leading to increased price volatility and costs of capital. Recent French and Italian initiatives immediately undershot revenue expectations, as market activity shifted.

As well as the practical problems, the political barriers are also steep. Joe Biden has put forward no detailed proposals for an FTT, suggesting his backing is lukewarm at best. Nor would Democratic electoral success in the Senate boost its chances, as it is hard to envisage strong backing from likely Senate majority leader and senior New York senator Chuck Schumer.

At a time when growth and recovery are much higher up the ballot, a tax that touches so many ordinary Americans may have to wait.

Swiss exchange operator SIX is to establish its fintech incubator and accelerator F10 in Spain, following on from its acquisition of Bolsas y Mercados Españoles (BME) this summer.

The plan is to set up locations in Barcelona and Madrid as well as operations in Bilbao and Valencia, with the first cohort of startups expected to move to the programme in March 2021.

The aim is to enhance mobility of high-quality start-ups between Spain, Switzerland and Singapore and further support the long-term fintech strategy of these countries. It is looking for local corporations and investors to participate.

According to SIX, F10 offers established banks and insurers the opportunity to future-proof their technology by working with startups in fintech, regtech, insurtech and deeptech.

Since 2016, more than 100 banking and insurance tech startups from around the globe have completed the F10 incubation programme.

F10 already supports a Spanish firm iBlackGull, a fintech startup for small to medium sized entreprisres in internationak trade.

Jos Dijsselhof, SIX CEO and Chairman of BME, said, “We are here to deliver on our promises. The installation of F10 shows our commitment to strengthen the Spanish market and to enable startups with strong potential to gain access to our organization and global network.”

He added, “This is only the first step to become more ambitious and innovative as a combined group, investing in opportunities that would have been unavailable to the separate entities.”

F10 co-founder commented, “We see great potential in the Spanish financial sector due to the recent growth in tech startup investment, an abundance of highly skilled game changers, and the innovation-oriented mindset of its established businesses. The progression of the Agenda España Digital and the increasing importance of digital business models in Spain offer ideal conditions for fintech innovation.”

SIX became Europe’s third largest stock exchange operator by revenues after completing a €2.57 bn takoever of BME, setting the scene for further expansion across its different business divisions.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.