CME Group is introducing options on its Micro E-mini equity futures, which started trading last year, and have been the derivatives exchange’s most successful new product launch.

Tim McCourt, CME Group global head of equity index and alternative investment products, told Markets Media that there was a clearly articulated customer demand to launch options on its Micro E-mini S&P 500 and Micro E-mini Nasdaq-100 futures contracts.

He said: “The customer demand for Micro E-mini options is palpable and the reaction has been uniformly positive.”

CME launched four Micro E-mini equity futures in May last year.

McCourt explained that when CME launched E-mini equity index futures in the late 90s they had a notional value of about $50,000, but the price of the indexes has since tripled.

“As a result, the risk taken and capital requirements increased so we launched Micro E-mini contracts,” he added. “At one tenth the size they are more approachable and users have more precision.”

When the four Micro E-mini futures started trading in May last year aggregate volume grew to more than one million contracts in less than three full days of trading, which McCourt said exceeded expectations.

In order to increase the velocity of trading CME designed the Micro E-mini contracts so they are similar to the original larger contracts. This means that liquidity providers and market participants can easily trade both contracts side by side and use the same straight-through-processing for settlement.

Tim McCourt, CME Group

“They have been our most successful new product launch as more than 300 million contracts have been traded,” he added. “More than 150,000 customers have used the contracts and about half were new to CME.”

He continued that the Micro E-mini futures have been popular around the globe with 28% traded internationally, compared to an average of 23% for CME’s equity products overall.

CME reported that in the second quarter of this year equity index contracts had an average daily volume of 5.6 million contracts, including a record ADV of 1.9 million for Micro E-mini equity futures.

In June equity index ADV grew 64% from a year ago, with Russell 2000 futures increasing 49% and E-mini S&P 500 futures rising 32%.

McCourt said: “There was a significant spike in the volume of Micro E-mini futures during the increase in volatility in late February and March. Volumes have held up due to intra-day volatility as users react to earnings and other news.”

Adena Friedman, Nasdaq

Nasdaq reported yesterday that combined U.S. equities and options markets set a record for trading volume in the second quarter of this year.

Adena Friedman, president and chief executive of Nasdaq, said on the results call: “The current backdrop of the pandemic, the economy and the election should support elevated volumes in the second half of this year.”

Bill Bierds, President and CBDO for BCC Group, and Bill Fenick, VP Enterprise at Interxion, discuss market data in the cloud: its evolution, how companies are currently using the cloud for market data and how COVID-19 has accelerated this shift, and what the future holds. The webinar is moderated by Markets Media Editor Terry Flanagan.

Tomorrow the U.S. Treasury will conduct the final reopening of the recently reintroduced 20-year bond. With some semblance of a track record under its belt, albeit early days, we thought now was a good time to examine how the 20-year’s been received and why it matters.

In May, for the first time in over a decade, the market prepared for a new (old) nominal security: the first issuance of a 20-year bond since 1986. Given that U.S. Treasury issuance tends to have regular intervals and relatively predictable and consistent sizes, the addition of more duration to the market is significant.

Not unlike the 2006 reintroduction of the 30-year bond, the new 20-year auction became a focal point for the market. In some respects, the backdrop of the rates landscape was similar when both bonds were reintroduced, with generally low yields. Although only one of them launched in the midst of a global pandemic.

When the U.S. Treasury reintroduced the 30-year, it auctioned off bonds worth $14bn with a then record low yield of 4.53% in February 2006, which compared to closing levels of 4.54% on the 10Y and 4.65% on the 2Y on that day. This made for relatively cheap funding, especially given the duration. Looking at May 2020 when the new 20Y was auctioned off at 1.22%, the U.S. Treasury market closed with levels of 1.40% on the 30Y, 0.68% on the 10Y, and 0.16% on the 2Y – again remarkably cheap funding given the duration! Even the initial issuance size for the new 20Y was noteworthy: at $20bn, it was well above expectations.

The 20Y auction results were pretty in line with other recent long-term issuance. Further, investor participation by class was roughly in line with a typical 10Y or 30Y auction, although there was relatively strong demand from pension, retirement and insurance funds, who bought more in this 20Y auction in May than any 10Y or 30Y nominal bond auction since October 2015, and continued to show demand in the June reopening.[1]

Moreover, during the June reopenings of the three securities, the 20Y saw relatively strong demand, with a relatively high bid-to-cover compared to May’s auction and an auction yield through the 1pm WI level. Meanwhile both the 10Y and 30Y auctions saw bid-to-covers flat to lower compared to May, and yields that saw some concession relative to 1pm WI levels. Following one of the strongest 30Y auctions in years, we will see how the final reopening of the 20Y goes on Wednesday.

The Buyers of the 20Y Look to be in Line with Other Long-Term Debt in May and June[2][3]

Auction date

Security type

Depository institutions

Individuals

Dealers and brokers

Pension and Retirement funds and Ins. Co.

Investment funds

Foreign and international

Others

12-May-2020

10-Year Note

9.44%

0.04%

22.49%

0.00%

42.82%

25.22%

0.00%

13-May-2020

30-Year Bond

0.05%

0.03%

36.29%

0.00%

54.97%

8.65%

0.01%

20-May-2020

20-Year Bond

0.10%

0.01%

28.07%

0.90%

57.77%

13.14%

0.00%

09-Jun-2020

10-Year Note

0.00%

0.00%

33.96%

0.00%

53.71%

12.32%

0.00%

11-Jun-2020

30-Year Bond

0.00%

0.00%

29.24%

0.00%

62.51%

8.25%

0.00%

17-Jun-2020

20-Year Bond

0.00%

0.01%

26.11%

0.06%

57.42%

16.41%

0.00%

Still, there are other interesting things about the reintroduction of the 20Y that we think merit further examination. We wanted to examine both the evolution of trading in the new issue as well as historically how activity in new benchmarks has progressed.

We’ve found:

Evolution of price formation of the new 20Y was consistent with typical When-Issued trading

As we’ve seen historically, this new benchmark has been additive to on-the-run trading activity

Over time, the market has seen a relative rise in long tenor trading coincident to an increase in back-end issuance.

Price Makers

Like other new U.S. Treasury securities, the When-Issued (WI) 20Y became active for Tradeweb institutional clients on its announcement date – in this case May 14th, 2020. The WI market for this security generally developed like that of the other long-term securities (i.e, 10Y note, 30Y bond) with virtually the same number of liquidity providers prior to the auction.

As with other Treasury securities, the auction acted as the liquidity event. The numbers of liquidity providers sending indicative quotes on the first day following the auction (i.e., the first day the security was an “on-the-run”) grew in line with typical participation for an on-the-run. Moreover, actual pricing updates during U.S. trading hours[4] were in-line with pricing updates for the long bond.

Evolution of Trading Activity

Given the extraordinary times that the new 20Y was launched in, we are hesitant to draw too many conclusions from early trading activity in the new security. However, in both institutional and wholesale client sectors, the new security activity has shown no signs of cannibalizing trading activity in on-the-run (OTR) trading of either the 10Y or 30Y securities. Moreover, in the last two month’s OTR 10Y and 30Y institutional trading activity is up 13% and 47%, respectively, compared to May and June of 2019.

As Tradeweb has been facilitating electronic trading of U.S. Treasuries since our foundation in 1997, we can look at how trading activity evolved in previous episodes when the Treasury launched a new maturity. We think that the two most instructive comparisons are what happened to daily volumes when the Treasury reintroduced the 30Y bond in 2006 and the 7Y note in 2009.[5] In both instances, the new maturity had limited impact on other benchmark securities and resulted in additive trading volume.

For simplicity, we focused on on-the-run trading of our institutional clients during the launch of these securities over a decade ago.

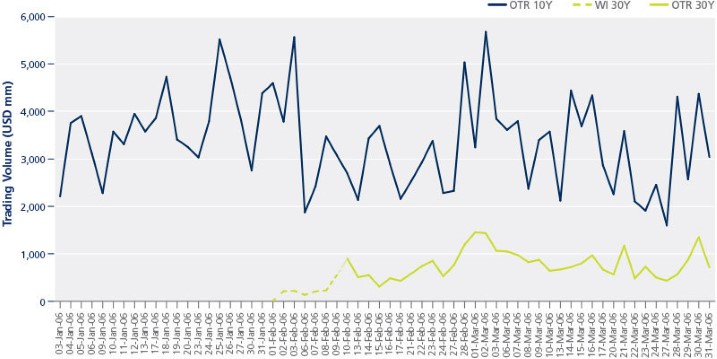

Reintroduction of the 30Y Bond

In January and February 2006, up until the February auction on the 8th, the on-the-run 10Y (912828EN6) had an average daily volume of $3.7bn on Tradeweb. The new 10Y issue (912828EW6) finished February with an ADV of $3.0bn[6], which then rose to $3.3bn in March. Meanwhile, the new 30Y bond (912810FT0) had an ADV of $650mm in February and $847mm in March. When taking into account duration, the introduction of the new long bond was accretive to on-the-run trading when it was launched.

The Reissuance of the 30Y did not materially impact 10Y On-The-Run Note Trading

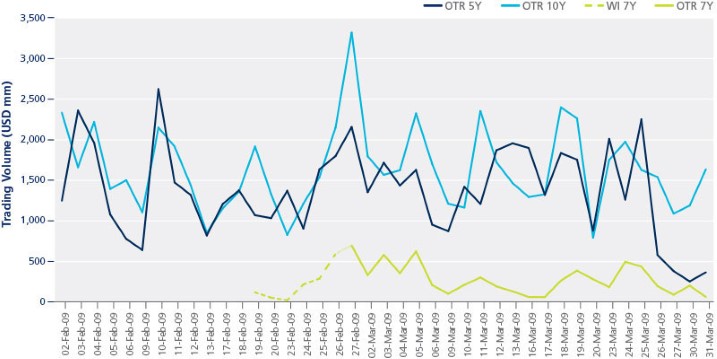

Reintroduction of the 7Y Note

In February 2009, up until the February auction on the 11th, the on-the-run 10Y (912828JR2) had an average daily volume of $1.8bn on Tradeweb. The new 10Y issue (912828KD1) finished February with an ADV of $1.6bn[7], which remained around that level in March. Meanwhile, the on-the-run 5Y (912828JZ4) had an ADV of $1.3bn in February, while the new OTR (912828KF6), auctioned on February 25th, saw a slight uptick to $1.5bn in March. While it was the on-the-run, the newly issued 7Y (912828KS8) had an ADV of $0.3bn. Again, the new 7Y was accretive to overall on-the-run trading activity.

The Reissuance of the 7Y did not materially impact 5Y nor 7Y On-The-Run Note Trading

Adding Duration

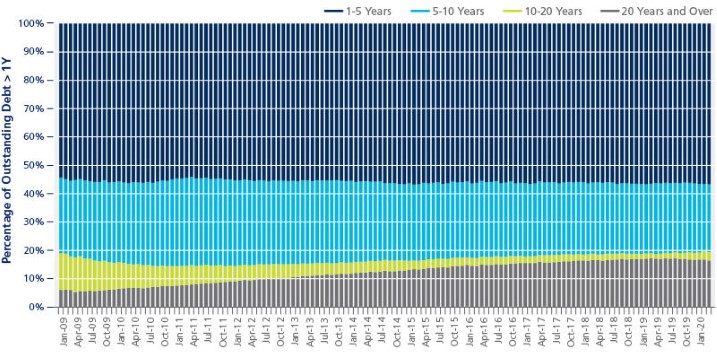

In 2009, and among other actions, the U.S. Treasury began a long-term campaign to increase the maturity profile of its overall debt by increasing issuance in long-dated securities. This has extended the average maturity of government securities outstanding from ~50 months to its current levels ~70 months.[8] Long dated issuance has now grown from ~5% of total nominal coupon issuance to ~9% of an ever growing total issuance in the first calendar quarter of 2020.[9]With this shift, we have seen the bond sector become an increasing percentage of Treasuries notes and bonds outstanding[10]. Treasury Bonds that have a maturity of 20 years and over currently comprise more than 16% of the total, a doubling from 2011.

At Tradeweb, this has had an impact on the makeup of trading activity in the government bond market, with trading in longer term securities becoming an increasing proportion of trading activity. This is obvious on the Tradeweb institutional platform, where steady growth in long-term debt issuance means ≥20 year bonds now represents 12.0% of nominal coupon volume vs 7.3% in 2014.

Bonds have become an Increasing Proportion of U.S. Treasury Debt Outstanding

Conclusion

In the end, one of the most interesting outcomes of the new 20Y auction is how uneventful the event itself actually was. One could chalk this up, in part, to the benefits of the “regular and predictable” auction strategy that the U.S. Treasury adopted for all marketable securities after observing issues with auctions in 1975, during another period of rapid expansion of the federal deficit.[11] It also helps that the Treasury works with market participants to ensure orderly trading of its debt – and indeed it appeared market participants were well-prepared. With the continued growth in the issuance of long-term bonds, the power of a well-functioning electronic market built with its customers in mind, like Tradeweb, is essential to ensuring transparent and robust liquidity in one of the most important markets in the world.

Etrading Software has made three new hires in its London office, and developed a new operational layer in Asia.

In Europe, Etrading Software has built up its outsourced services delivery capability through the hiring of James Haskell as business operations officer (BOO), David Lane as technical operations officer (TOO) and the appointment of Will Palmer as chief information security officer (CISO). These senior appointments are charged with overseeing the day to day operations of ETS’ existing and new managed services offerings.

James Haskell

Etrading Software designs, builds and operates technology solutions, framing, facilitating and navigating complex decision-making structures – from incubation to execution – that provide financial institutions and industry initiatives with technology designed for over-the-counter (OTC) markets. Examples include its work with Neptune Networks, the Derivatives Service Bureau (DSB) and most recently the Loan Desktop platform.

David Lane

With over 20 years’ experience working in financial services and operations in London, New York and Hong-Kong, including more than 13 years in Goldman Sachs, Haskell joined Etrading Software in May 2020, in the newly created role of BOO, with oversight for the day-to-day operational running of Etrading Software’s existing and new managed service products.

Lane has over 20 years’ experience in tier one investment banking and derivatives exchange trading environments. His more recent engagements have involved supporting financial institutions in technology strategy, governance, and risk frameworks primarily in association with cloud migrations.

Will Palmer

As the new CISO, with over 25 years’ experience in IT within the financial services sector in both London and Asia, Palmer will be using his prior knowledge of service stability, client on-boarding, continual service improvement and team delivery to build a company-wide security strategy for the firm.

In Asia, Etrading Software has expanded its offering to include a design, build, operate model for Etrading Software clients, incorporating a 24 x 7 operations capability for services.

Sassan Danesh

Sassan Danesh, managing partner said, “Our offices in Manilla have been long established as a centre for excellence, and we are seeing increased interest from the marketplace to utilise our outsourced services model.”

Lynn Strongin Dodds looks at how the industry has coped and what tools and strategies they will need for the future.

Despite advanced technology and sophisticated modelling no one predicted a black swan event such as Covid-19. This explains why business continuity or disaster recovery plans were not fit for purpose. Navigating the future will be challenging but many of the issues facing the buyside are deep rooted.

There is no doubt though that the volatility in the first quarter took its toll. Data from Refinitiv showed that assets under management in the European fund industry slid from €12.3trn to €10.6trn mainly due to the performance of the underlying markets and estimated net outflows of €125.9bn. However, the buyside had been buckling from lower returns due to the historically low interest rate environment, the ongoing shift to passive and alternative asset classes and slowing organic growth. This is not even mentioning continued fee pressure and aggressive competition from within and outside the industry.

In many ways, Covid-19 accelerated trends that were already there,” says Octavio Marenzi, CEO and co-founder of consultancy Opimas. “There have been cost pressures and the shift to passive from active are long-term trends. This will not change, although we may see a shift to performance-based compensation from management fees. I also think that the environment will accentuate consolidation as firms look for scale.”

The first wave saw significant tie-ups with the £11bn merger between Standard Life and Aberdeen Asset Management, the $6bn union between Janus Capital and Henderson Global Investors, and Amundi’s €3.5bn takeover of Pioneer Investments. More recently, the activity has been on the smaller to mid-size end of the scale such as Liontrust’s purchase of Neptune and Merian Global Investors, the £26.4bn boutique spun off from Old Mutual, acquiring Kestrel Investment Partners’ multi-asset business.

M&A will only be one part of the equation going forward. On the big picture level, firms that want to survive will need to refocus their product portfolio, transform cost structures and invest in innovative technologies that will drive the business forward over the long term, according to the report from Boston Consulting Group (BCG) – Protect Adapt and Innovate. Information will continue to be key and firms can carve out an edge by building data science capabilities that gather, clean, synthesise, and visualise vast amounts of client information.

A different kind of crisis

“The pandemic has only intensified the industry’s challenges,” says Lubasha Heredia, a New York–based BCG managing director & partner, and co-author of the report. “After the financial crash in 2008, the asset management industry benefited from a market rebound that produced the longest bull market in history and prompted the rise of passive assets and winner-take-all phenomenon. We expect this phenomenon to continue in response to the early 2020 crisis.

She adds, “firms are focused on recovering flows and profitability and we expect to see accelerated digitisation, increased M&A activity and product innovation. I think firms that will suffer the most will be those in the middle because they do not have the scale or products that can consistently outperform the market.”

Not surprisingly, those that do not embrace greater automation and cutting-edge technology such as artificial intelligence and cloud-based systems will be left behind. This does not only mean developing innovative more client focused products but also strengthening the back and middle office backbone to ensure there is the operational resiliency that is needed for current and future shocks.

As Matt Stauffer, Managing Director, head of institutional trade processing at DTCC, notes, “The buyside is focusing on the challenges ahead leading them to reallocate their resources to ensure that they are prepared for a potential second wave of disruption,” says “We will likely see more attention paid to operational efficiency and a greater push towards automation as a result.”

Dan Shepherd, chief executive of BTON Financial, the independent outsourced dealing desk for asset managers, adds, “Covid focused the mind in terms of business continuity planning and the impact of the failure to plan. I think this will lead to an increase in automation and leveraging technology in general to improve processes and workflows. I also expect to see an increase in outsourcing especially in trading. In the past, fund managers may have had to justify a reason to outsource the function but now they may need a reason to keep it in-house.”

Buyside firms will also have to up their game, for example, in their usage of cloud-based systems as well as artificial intelligence (AI) that can capture more complex, non-linear patterns in asset behaviour and real time algorithms which adapt to changing market conditions. Data, of course, will be key. However, the latest Data Operating Models Study by Alpha FMC showed that low staffing levels, lack of senior oversight and budget constraints are holding back asset managers from developing comprehensive data strategies that can help sharpen their edge.

Canvassing 33 asset managers with a combined AUM of £6.9trn, the report found that they see big data analytics and artificial intelligence (AI) as critical to improving investment returns, as well as helping them differentiate against competition by enhancing customer experience, ensuring customer retention and, crucially, cutting costs. Structural barriers, legacy technology and lack of commitment though are preventing the industry from leveraging data to improve their processes.

“The most important thing is that firms have an infrastructure that has the ability to scale quickly, deal with market disruptions, a lack of liquidity and increased credit & counterparty risk,” says Brad Foster, global head of enterprise content at Bloomberg. “In terms of data, fund managers need to take a more holistic view and look at ways to better use and extract the value of from the data they can have access to.”

WFH (working from home)

The buyside will also have to be more adaptable in their working practices. Traditionally, the industry has been wedded to the tried and tested pyramid structure with the portfolio managers or the investment decision makers at the top supported by banks of sales and distribution people in the middle with a host of administrators at the base. The old model was broken when Covid struck and seemingly overnight, firms were forced to transition and equip employees to a working from home environment.

Although lockdown is easing, the picture is mixed in the UK and Europe with some fund managers opting to return to the office albeit not in full capacity while others are more reluctant for fear of a second wave. For example, Standard Life Aberdeen, has told its 4,900 UK workforce that the majority of them should continue to work from home for the rest of 2020 while, M&G Investments, Jupiter, Janus Henderson and Invesco have said that their UK offices would remain closed for the time being. Amundi Asset Management, on the other hand, is expecting to have half its staff return between July and September, while LGIM, the UK’s largest asset manager, said most of its staff will continued to work from home, with limited reoccupation in London, Cardiff and Hove.

Those firms that had tightly integrated systems and cloud-based technology were best placed to have made the transition from the office to working from home, according to Chris Hollands, head of European sales and account management at OEMS provider TradingScreen. “In general, there also needs to be good communication between the execution traders and portfolio managers, as well as a strong audit trail.”

Looking ahead, it is hard to predict the long-lasting impact of Covid-19 on office life but market participants expect there to be a fundamental mind shift especially as productivity has not suffered and in some cases has risen. The most likely scenario will be a hybrid model whereby the week is split between working from home and the office. This is because although people have adjusted, there is still no replacement for human contact.

As Chris Dyer, Direct of Global Equity and Portfolio Manager at Eaton Vance and Calvert notes, “Although the industry has managed to adapt to working from home, it is difficult to replicate office life, employee communication and collaboration. We have daily calls throughout the day with teams and individuals but it is not the same as in person. What is important is to be proactive and ensure that you have the right investment philosophy and culture.”

This week, Dan Barnes speaks with Global Trading’s Shanny Basar about fixed income ETFs. In these uncertain times, why are they proving so popular (in light of BlackRock’s record inflows), and are there any initiatives in the mechanics of trading ETFs?

James Binny, Global Head of Currency at State Street Global Advisors talks about how regulation, technology and now Covid‑19 is leaving its mark on the FX market.

James Binny is global head of currency and head of investments Ireland. He joined the company in January 2016 as head of currency for EMEA. Binny has worked in the industry since 1990, predominantly in investment management of global fixed income and currency. He has worked on or led teams at firms including Brevan Howard, Gartmore and County NatWest. He also managed a currency manager of managers product at ABN AMRO Bank. He is well known as an industry innovator, and was one of the first individuals to work on Currency Factor processes over a decade ago.

What has been the impact of Covid-19 on FX?

We trade spot and forwards and in general, spot trading has increasingly become more electronic and when volatility blew out as economies shut down because of Covid, it remained an efficient market. Spreads widened but that reflected the overall market. The systems have become more sophisticated and we were able to get prices from our counterparties throughout. This is in contrast to 2015 when the Swiss National Bank let go of the three-year cap on the Swiss franc.

By contrast, forwards are more dislocated and in mid-March when volatility was high, the spread in cable (referring to the sterling/dollar pair) widened five times while it was 50 times in the forward points. The problem is that forwards are related to short term interest rate movements which were suffering from a dollar funding crisis but also, they are also more bespoke and difficult to commoditise. People want different dates and credit requirements depending on their own requirements. This mean there is more manual intervention which makes it difficult to get streaming prices.

How did you manage from an operational perspective in terms of traders working from home?

Automation and communication. In Sydney we have portfolio managers who instruct traders in Hong Kong through automated systems and processes. In London, the portfolio manager would sit on one side of the room and traders on the other so there is a closer proximity but they use the same systems, so that part was already in place. However, now that everyone is working from home, we have made sure that they had the technology they needed. Traders were the most reluctant to work from home but the transition has gone smoothly for them and they were still able to get the best price for our clients. We also had tested the surveillance systems and were recording phone calls because before lockdown we had a trader who lived in Brighton and wanted to work from home occasionally. So fortunately, we already had the systems in place.

What about communication?

Maintaining the same level of communication is also a main priority. We have always had a morning call with traders and portfolio managers and that call is more important than ever. Also, because many people are not commuting, you can spend more time on videos which helps with human interaction and in making sure that everyone is doing ok because it can be difficult living and working from home when you are on your own.

One slight concern though is while teams are working well together, we are seeing less communication between teams. For example, the fixed income desk sits next to the currency team and the danger is that they become more siloed. We also have to make sure there is greater communication between portfolio managers and sales and distribution teams – there is a danger that they can operate in parallel universes and so we have instigated increased calls and market updates.

Looking ahead, what long term impact will Covid have on FX trading desks?

It is still early days and people in the industry have been surprised by how efficiently things have worked. In many ways it has given us more resilience but has also shown us the value of automation. If this had happened five to ten years ago, the market would have seized up and the industry would have had difficulty coping with the volatility and volumes.

What technologies, algos and strategies will help teams navigate the current and potential landscape?

There is a lot of talk about algos and TCA (transaction cost analysis) but that is all about the spot market. Of course, we use them. However, forwards have the biggest impact in terms of hedging cost and as I mentioned earlier, they are the most challenging. For example, we can demonstrate best execution to clients more easily in the spot market but it is more difficult in the forward market, as it can be harder to define the benchmark price, and that is why I think there needs to be a greater push towards automation.

In general, pre Covid how has MiFID and other regulations changed FX trading and investing?

The general trend has been to increase transparency which suits us because we have always explained the costs of the transaction to clients. We have also always sought best execution for our clients but now we also have to demonstrate it. TCA has become more important and we have become more sophisticated in our calculations.

One of the biggest impacts for us of MiFID II was unbundling research from execution. It was easier to define the cost in equities where there are commissions, than in spread markets such as FX and fixed income. I see the justification for the change; for instance, we are managing $112 billion in currency and $100 billion of that is in passive. The rest is active which is where most of the research is focused. Like most of the big firms, we are paying for the research ourselves.

What changes have you made since joining at the end of 2017?

In general, the market has become more automated and so have we. As index managers, for example, we get very busy at the end of the month with index rebalancing. This leads to a huge number of transactions but technology has made the process much more efficient and cost effective. The same is true with TCA in the way we measure it and the cost savings we can achieve for our clients.

We increased our focus to become more resilient whatever the time zones our clients were in. We are a global organisation with Currency portfolio managers in Sydney, Boston and London, and we wanted to ensure that we were able to manage our clients’ portfolios and maximise their opportunities, regardless of their location or asset classes they were investing in while at the same time complying with the different legal constraints.

What skillsets do you need today in FX and how do you see AI machine learning being applied to help portfolio managers and traders?

When I started 30 years ago, there was less computing power so you had more time to think about the opportunities. Today, you have to be able to process information quickly and analytical skills have to be much tighter. I think artificial intelligence can help accelerate the decision-making process but it is hard to let it control the process completely. From a fiduciary responsibility perspective, it is very important to understand what exactly is driving the AI model that you are using to take positions for your clients.

What other challenges and opportunities do you foresee in the future?

Looking at forward markets, I think we will see more opportunities in peer to peer or buyside to buyside trading. We have some of this kind of non-bank activity in the spot market and it has the potential to grow further. There are firms who are considering how we can develop this in the forward market.

In terms of challenges, we are looking at going back to the office and the issues involved with maintaining social distancing. We will learn from what our Sydney office has done and how we can reconfigure our space in our other offices. We plan to gradually increase the number of people back in the office during the rest of the year and that will depend on the country and particular government restrictions. However, we are inviting, not ordering, people back and we can continue to do what we have been doing because we have not come across any serious operational difficulties.

Shanny Basar talks to Stephanie Clarke, senior vice president of global market intelligence within Broadridge Financial Solutions’ about the power of data, technology and diversity.

When Stephanie Clarke began her career in finance she had to use reference books for her research, or visit libraries across the City of London.

In contrast, her role as senior vice president of global market intelligence within Broadridge Financial Solutions’ mutual fund and retirement solutions business means she can take advantage of automation and the huge volume of electronic data being generated on a daily basis. She is based in London for the US company which provides investor communications and technology for broker-dealers, banks, mutual funds and corporate issuers globally.

Clarke said: “When I worked in asset management I pieced together data from many places so my firm could get a holistic view of the industry. However, every asset manager was doing this – there was no data provider providing this service for the whole industry, each firm had to do it by themselves.”

Broadridge provides financial services firms with information to support distribution, product development, sales and marketing through the use of advanced analytics and data visualisation. Distribution Insight products provide a view of the whole landscape for asset managers using consistent and granular data.

“They have the tools to understand the whole universe they operate in and so can understand the dynamics behind their firm’s position in geographies, client segments, products and their competition,” Clarke added.

She gave another example of the change in technology and data since the start of her career. When she worked for an asset manager they had to send prices for their unit trusts to Jersey by plane – and if it could not land they had to fax a page of the Financial Times.

“Data has grown exponentially to the point that now the issue is separating the signal from the noise, knowing what action to take,” she said.

For example, investors can now predict retail sales from satellite images of car parks rather than waiting for estimates from brokers or governmental statistics agencies.

Clarke added: “We would have struggled to scale to the massive increases in data volumes in the past four years if we had not employed complex data automation methods.”

Impact of Covid-19 She continued that the pandemic has brought environmental, social and governance considerations to the fore and changed the investment landscape.

“We have partnered with MSCI for ESG data and we are continuing to develop relevant ways of measuring ESG for our clients,” she added.

Clarke is a member of a return to work task force redefining how Broadridge works. She said: “In our connected workplace, we can use offices as collaboration and innovation hubs to meet with colleagues and clients, rather than a place where you come and do spreadsheets.”

The firm is also exploring new models of client engagement such as webinars, podcasts, virtual user groups and communities rather than the traditional in-person conferences.

Clarke said: “There will be more digital engagement as we move towards a Netflix model.”

She is optimistic about changes that the requirement to work from home has made to the industry by forcing recognition of staff having an existence outside the office and the need for more flexibility.

“This flexibility has not come at any cost or detriment to the business,” Clarke added. “We can come out of this crisis with less distance bias and more focus on outcomes rather than presenteeism.”

Partnerships When Broadridge hired Clarke in 2016 the firm said it underlined the commitment to grow its competitive intelligence business following the acquisition of the Fiduciary Services and Competitive Intelligence Business from Thomson Reuters in the previous year.

After she joined, Broadridge bought Spence Johnson Limited in 2017. Spence Johnson provides global institutional data and intelligence to the asset management industry and its Money in Motion product tracks institutional flows.

In 2018 Broadridge purchased MackayWilliams, a specialist European fund market and research firm.

“The purchase of Spence Johnson added the institutional part of the landscape to our platform,” added Clarke. “MackayWilliams was a European specialist who understand brands through interviewing thousands of fund selectors each year.”

In addition to making acquisitions, Broadridge also look to partner with firms who provide new data sources or are best in class providers for certain niches, such as Preqin for alternative assets.

Career path Prior to Broadridge, Clarke had been global head of market intelligence at BlackRock. She also had previous research and intelligence leadership roles at Merrill Lynch Investment Managers, Mercury Asset Management and Sanwa Bank. She has an economics degree which suited her capability in both maths and English, skills which led her to looking for a career in research.

“My advice to women entering finance is that it is a great place if you have problem solving skills,” she said. “You have to find your skill-set and build your career around it by finding new adventures.”

Clarke works in a technology-driven branch of finance, which she believes needs, and wants, more diversity – not just in gender, but also in thought and perspective. “It is now a recognised fact that diverse teams bring about better outcomes” she added.

She continued that women bring a different perspective, so it is important that their voices are heard. “We have a responsibility to grow women under us and continually make sure our biases, conscious or not, are broken down,” she said.

Clarke co-sponsors Broadridge’s Women Lead program to inspire the next generation to take their careers to the next level and think really big.

She concluded: “We all have imposter syndrome but you have to shake it off and take small steps every day to travel towards your goal.”

Bloomberg Index Services Limited (BISL) has begun calculating and publishing fallbacks that will help facilitate the withdrawal of certain key interbank offered rates ahead of the LIBOR transition set for end of next year.

Last November, the International Swaps and Derivatives Association (ISDA) published a report summarising market feedback on the final parameters of adjustments that will apply to derivatives fallbacks for certain IBORs

Scott O’Malia, CEO, ISDA

The trade group is implementing adjusted versions of the RFRs (risk-free rates) to serve as IBOR fallbacks, to account for the differences between RFRs and IBORs. RFRs are overnight rates without a credit component, whereas IBORs have term structures and credit sensitive elements.

In July 2019, Bloomberg was selected to calculate and publish the adjusted RFRs, following an in-depth selection process. BISL is authorised by the Financial Conduct Authority as a regulated UK benchmark administrator and has conducted index administration since 2014.

The calculations include the adjusted RFR (compounded in arrears), the spread adjustment and the ‘all in’ IBOR fallback rates across various tenors for the BBSW (Australia), CDOR (Canada), Swiss franc LIBOR, EURIBOR, euro LIBOR, sterling LIBOR, HIBOR, euroyen TIBOR, yen LIBOR, TIBOR and US dollar LIBOR.

Industry participants will be able to access the information through various distribution channels, including the Bloomberg Terminal, the desktop API, Bloomberg Data License and authorised redistributors.

“The introduction of robust new fallbacks for derivatives contracts will significantly reduce the systemic risk posed by a permanent cessation of a key IBOR,” said ISDA chief Scott O’Malia. “Publishing indicative spread adjustments and all-in fallback rates now will help firms as they prepare to implement the new fallback methodology.”

Umesh Gajria, Global Head of Index Linked Products at Bloomberg

Umesh Gajria, Global Head of Index Linked Products at Bloomberg, adds, “We are pleased to partner with ISDA to support the markets through the calculation and distribution of IBOR fallbacks. This is an important move forward as we continue to help our clients with their IBOR transition efforts.”

ISDA will publish the amendments to the 2006 ISDA Definitions and a related protocol in late July 2020, subject to receiving a positive business review letter from the US Department of Justice as well reassurances from other relevant competition law authorities.

The contractual changes to embed the fallbacks are due to take effect in ISDA’s derivatives documentation in November, or four months after publication.

Women in Trading: Challenges, Opportunities and the Road Ahead

This webinar will focus on senior women in institutional trading: the career paths to their current roles, their achievements and aspirations, and their unique experiences as a woman in an often male-dominated industry. The webinar will blend content about current challenges and opportunities for traders in capital markets, with a ‘personal touch’ that draws out the stories of the webinar guests.

When: July 30, 8am HKT (July 29, 8pm EST)

Participants:

Azila Abdul Aziz, CEO/Executive Director & Head of Listed Derivatives, Kenanga Futures

Susan Chan, Head of Asia and Head of EII and TLL Asia Pacific, BlackRock

Emma Quinn, Global Co-head of Equity Trading, AllianceBernstein

Jessica Morrison (MODERATOR), Co-Regional Head APAC, Head of Execution Services APAC, Virtu Financial

Topics to be discussed:

Corporate initiatives that effectively promote the cause of women in finance

Challenges and opportunities brought to professional women by COVID-19

Skillset for a leadership position on the trading desk

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.

Lynn Strongin Dodds looks at how the industry has coped and what tools and strategies they will need for the future.

Lynn Strongin Dodds looks at how the industry has coped and what tools and strategies they will need for the future.

Shanny Basar talks to Stephanie Clarke, senior vice president of global market intelligence within Broadridge Financial Solutions’ about the power of data, technology and diversity.

Shanny Basar talks to Stephanie Clarke, senior vice president of global market intelligence within Broadridge Financial Solutions’ about the power of data, technology and diversity.