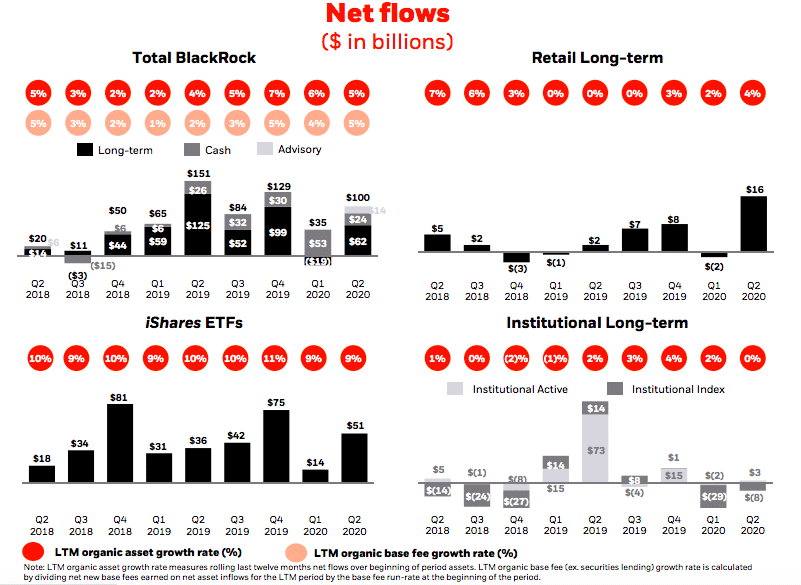

BlackRock had record quarterly inflows of $57bn (€50bn) in fixed income exchange-traded funds which the fund manager said validated its big ambitions for the asset class going forward.

Today BlackRock reported that in the second quarter of this year it had $100bn of total net inflows, representing 10% annualized organic base fee growth.

Larry Fink, chairman and chief executive, said in a statement: “iShares fixed income ETFs and BlackRock’s active equity strategies both saw record inflows, and leadership in cash solutions drove strength in flows as clients sought liquidity. Momentum also continued in sustainable strategies and illiquid alternatives, where we are investing for future growth.”

Net flows. Source: BlackRock.

Fink said during the results call that 60 new institutional clients had started using iShares fixed income ETFs for the first time during the quarter.

“They preferred the technology, lower cost, improved price discovery, transparency and liquidity compared with the underlying market,” he added. “We expect fixed income ETF assets to reach $2 trillion in five years.”

Gary Shedling, BlackRock

Gary Shedlin, chief financial officer, said on the call that the firm’s belief in fixed income ETFs had been validated by their performance during the rise in volatility caused by the Covid-19 pandemic.

Shedling said: “We have big ambitions in fixed income ETFs. The pace of adoption by asset managers, pension funds and insurance companies means the market has reached a turning point.”

He added that Blackrock had more than $634bn in assets in fixed income ETFs compared to $514bn a year ago, and $402bn two years ago.

Sustainable ETFs

In addition to fixed income, another area of focus for iShares is environmental, social and governance ETFs.

Fink said ESG ETFs had inflows of $17bn in the first half of this year, which is more than the whole of 2019.

Larry Fink, BlackRock

“We are more than three quarters through the process of having 150 ESG ETF offerings in three years,” he added.

In addition, BlackRock launched an ESG money market fund last year which Fink said has gathered $13bn.

“We expect sustainable assets to reach $1 trillion by the end of the decade,” Fink said.

Active equities

In the second quarter active equities had $8bn of inflows. Shedlin said this was the fifth quarter in a row of net inflows for active equities.

“In active equities we have arrived,” said Shedlin. “It has been a long journey. We have invested in the team and research and we will continue to invest in data and technology.”

Aladdin Provider

Shedling added that the firm is also going to continue to invest in Aladdin Provider, an end-to-end investment management platform across the trade lifecycle.

Citi said this week that it will connect directly with clients on Aladdin Provider. The bank will provide outsourced middle office services that seamlessly integrate with the front office and from trade confirmation to post-settlement reconciliation.

“Aladdin Provider is used by more than 90 clients,” Shedlin added. ‘We want to increase standardization across the ecosystem and increase straight-through-processing in the industry.”

The start of reporting under the European Union’s securities financing transactions regulation began smoothly last week but the buy-side needs to ensure it is prepared for being included from October.

Catherine Talks, UnaVista

Catherine Talks, product manager, SFTR at UnaVista, the London Stock Exchange’s regulatory reporting business, said in an email that whilst it is still early days, SFTR go-live has been relatively successful.

“There are always some things to iron out in the first few weeks of a regulation going live, but we have been pleased at the quality of the data that our clients have been reporting, we have seen 98% reports pass validation,” said Talks. “This is testament to the work done the industry has done to prepare.”

SFTR reporting started on 13 July with the aim of increasing transparency in repos, securities lending and margin lending markets. Reporting was due to go live in April but was postponed due to the global COVID-19 pandemic.

Banks, investment firms, central central clearing counterparties and central securities depositories have to report executed SFTs to authorised trade repositories. The data, consisting of approximately 150 fields, should allow supervisors to monitor market developments such as the build-up of leverage in the financial system. In addition, there are new disclosure obligations and collateral reuse obligations.

Talks added that Unavista is keeping a close eye on the situation and having daily calls with clients to keep them updated.

— Regulatory Reporting (formerly UnaVista) (@LSEG_Reporting) July 20, 2020

The European Securities and Markets Authority said last week that the first day of SFTR reporting had gone smoothly.

The European regulator added it will continue to engage with market participants to clarify any remaining issues and will assess the need for further supervisory convergence measures to facilitate compliance with the new reporting requirements.

❗️ [Update] 🎬 And it's a wrap! First day of reporting has gone smoothly.

All 4 Trade Repositories (TRs) opened their systems and started receiving and processing securitised financing transaction data submitted by reporting firms ➡️ no disruptions 👏https://t.co/4djSgznCPXpic.twitter.com/FNJPhmmUGx

— ESMA – EU Securities Markets Regulator 🇪🇺 (@ESMAComms) July 13, 2020

Julian Eyre, commercial manager at Delta Capita, which provides managed services, fintech solutions, and consulting, said in an email that the feedback from banks reporting under SFTR has been quietly encouraging.

“Albeit with the caveat of low report volumes, there have been no material issues or concerns so far,” he added. “However, it’s worth noting that the volumes are expected to rise exponentially as the number of lifecycle events that need to be reported increases.”

He continued that Regis TR, a joint venture between Deutsche Börse’s CSD Clearstream and the Spanish CSD Iberclear, confirmed a 95% average report acceptance rate last week. In addition, the US DTCC confirmed a 94% average report acceptance rate with a third of clients achieving 100% acceptance.

“Delta Capita is delighted with the first week given the role we played in facilitating and enabling industry testing through our test pack,” added Eyre. “This approach mutualised costs and converged on industry standards.”

Buy-side reporting

Heiko Stuber, senior product manager at SIX, the Swiss financial infrastructure group, said in an email that it was ‘so far so good’ with SFTR reporting.

Heiko Stuber, SIX

“From what we can see the trade repositories were not reporting any issues in the first week,” he added. “This was to be expected, though, as the banks have taken the extra time provided to them to get prepared.”

However, he warned that one potential problem which will not be illuminated in the initial go-live is that market participants need to have approval from ratings agencies and the main index providers on security and collateral data before they can use this in their reporting process.

“The costs of not doing so will only become clear over the coming weeks and months,” he said.

Buy-side firms will be included in the next phase of SFTR reporting in October this year.

“There is still a lot of work to do be done in this part of the market,” said Stuber. “However, they will be able to see how things have played out and what works, so they can learn the lessons from the first months. But they will have to do it quickly.”

Sunil Daswani, head of securities finance solutions at MarketAxess, the electronic fixed income trading and reporting firm, said in an email that it has been an exciting and positive start to the SFTR regulation implementation for phase one and two firms. However, he also warned that phase three firms need to ready for reporting later this year.

We are one week into #SFTR implementation for phase 1 and 2 firms! Core processing is in good shape so far with millions of transactions received and processed on the UTI portal. Thanks to our clients and partners for a smooth start – @EquiLend, @ICMAgroup & @__islapic.twitter.com/39CzN5Rcsl

— MarketAxess Post-Trade (Trax) (@MarketAxessPT) July 20, 2020

“This is a significant change to the industry landscape and there may still be challenges to iron out over the coming weeks,” he said. “It is important that phase three firms, that have their compliance date later this year, are aware of the full requirements of the regulation.”

Daswani continued that collaborative work with industry bodies, clients and partners has meant a smooth transition over the go-live date and core processing is in good shape.

Sunil Daswani, MarketAxess

“One week in and we’ve seen millions of transactions received and processed on our SFTR Insight reporting hub and the MarketAxess UTI portal – the industry wide, community sharing tool for exchanging of UTIs and related data,” he added.

Securities financing trades have to be reported to an authorised trade repository the day after a trade using a unique transaction identifier.

Changes to SFTR

Matt Smith, chief executive at the compliance technology and data analytics firm SteelEye, said in an email that he expects potential amendments to SFTR, but it is too early to estimate when changes will happen.

“However, whilst regulatory change would normally take years, as we have seen with MiFID II and other regimes, SFTR is looking quite different,” he added. “The industry has been very vocal as to differences between the legislative text and the published guidelines, with many firms and industry bodies lobbying the regulator for adjustments.”

As a result, he said that it is not a case of “if” but “when” the regulator will publish an update.

Last month SteelEye partnered with UnaVista to provide reporting services for Emir, the European Union regulation covering central clearing and derivatives, and MiFID II. They expect clients to migrate from CME’s European trade repository and NEX Abide regulatory reporting services, which will close in November this year.

Mark Husler, UnaVista

Mark Husler, chief executive of UnaVista, said in a statement: “Hundreds of firms face the challenge of migrating their reporting processes away from CME, and need to do so quickly.”

SteelEye and UnaVista have developed a data convertor so firms can use their existing reporting input files and also use the same data for both reporting requirements.

It’s that time of year. Many of you, like us, have interns and new hires joining the desk and needing to learn all about markets for the first time. So we decided to put together an “Intern’s Guide to the Galaxy” to help explain some of the core concepts about how markets work (virtually).

For those who have worked in the market for years, relax and enjoy the recap. You never know when an intern will ask a question on this stuff.

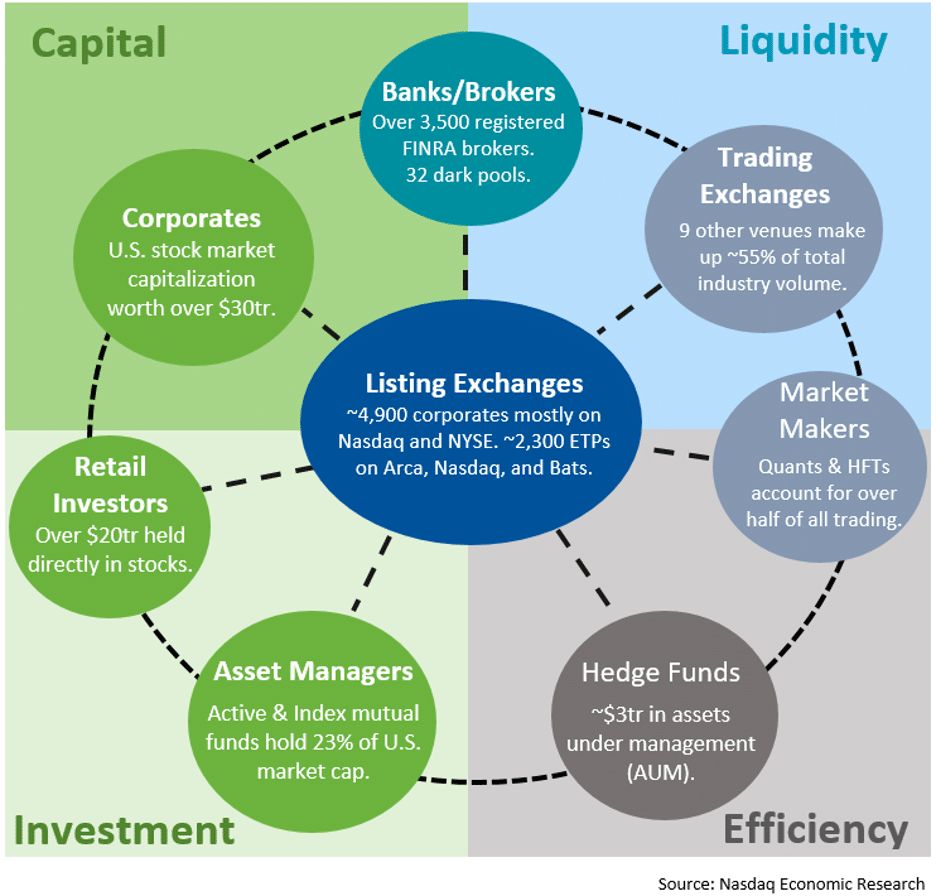

The markets are an ecosystem

Stock (and bond) markets have a pretty simple underlying purpose. They help join those who need capital with those who are looking to invest.

Modern markets have evolved into an ecosystem of specialized participants. Each playing a different but important role in primary (IPO) and secondary (trading) markets.

Chart 1: The market ecosystem

Issuers are critical to public markets. Without issuers joining public markets, there would be fewer companies to invest in and fewer dividends for investors and less securities to hedge and trade. To learn more about the trends in public listings see We Need a Constant Focus on Bringing IPOs to Market.

U.S. Equity markets aren’t alone though. Public markets have to compete with private markets, and U.S. markets also compete with international stock markets for listings. Having said that, the U.S. stock market is the largest source of equity capital in the world with $35 trillion of market cap.

Exchanges play a central role in stock markets, literally. They are (by law) open to everyone. Creating a “single market” for issuers, investors and liquidity providers allows companies, investors and traders to all interact at the same prices despite their different time horizons and trading signals. Exchanges, by making prices public, also create competition to be the best buyer or seller. That creates tighter spreads that not only reduce transaction costsbut also forms prices that everyone can use for portfolio valuation and to find new assets to buy or sell.

In contrast, bond markets don’t have exchanges. In those markets, banks provide different quotes to different customers and traded prices and volumes are often never disclosed. That makes it harder for any participant to know if their bond trade was at a good price (or not).

Investors come in two main flavors: mutual funds (also called “institutional investors”) and retail investors. Data suggests they both have around the same amount of capital to invest (approximately $15 trillion each). Other smaller owners of stocks include hedge funds, banks, market makers, arbitrageurs and foreign investors who hold U.S. stocks for investment, risk management or trading purposes. Although each of these participants have different objectives, they all play a critical role in keeping markets efficient and liquidity cheap.

Banks have many direct relationships with issuers and mutual funds. They research and often lend to companies. They also execute trades for mutual funds. Many also sell structured products that then need to be hedged in the market too. So they contribute to both capital formation and liquidity. Many of them also run their own ATS’s (Alternative Trading Systems, such as dark pools) which allow them to match trades off-exchange.

Market makers don’t hold stocks for long as their specialty is being both a buyer and seller at the same time. Creating a “two sided market” in each stock ensures investors can trade regardless of whether they are looking to buy or sell.

Hedge funds and arbitrageurs, in contrast, tend to hold long and short positions at the same time. Their strategies often also keep stock pairs or ETFs and futures efficiently priced. That helps reduce costs when investors try to buy a single ticker, helping make relative valuations more efficient.

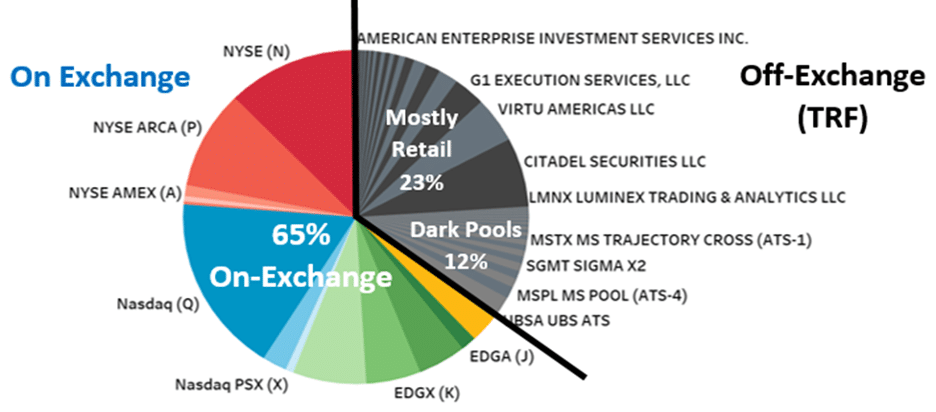

Where do stocks trade?

Decades ago UTP (Unlisted Trading Privileges) allowed trading exchanges to compete with listing exchanges for trading revenues. Brokers are also able match trades off-exchange, using an ATS (e.g. dark pools) or facilitating (trading directly with) clients trades, usually for profit.

This results in a very fragmented market. Over one-third of trading occurs off-exchange, and on-exchange trading is spread across more than a dozen venues (Chart 2). For more on how different markets attract liquidity, see Slicing the Liquidity Pie.

Chart 2: Where and how do stocks trade

Source: Nasdaq Economic Research

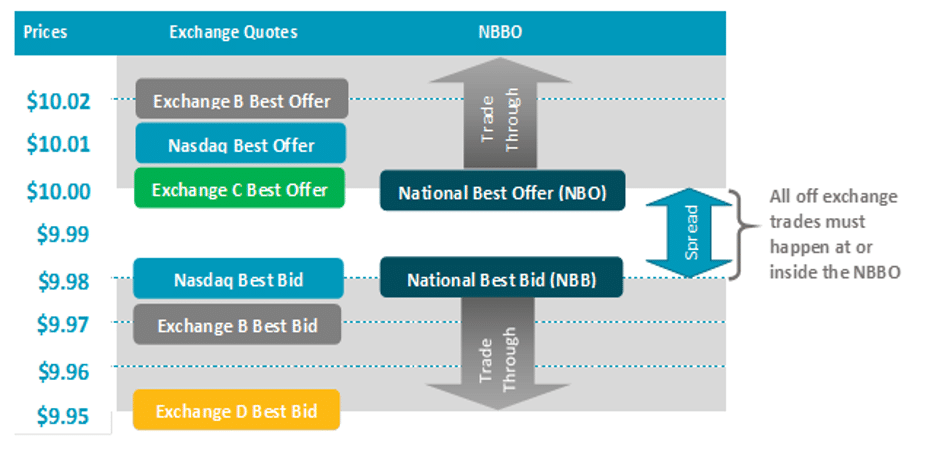

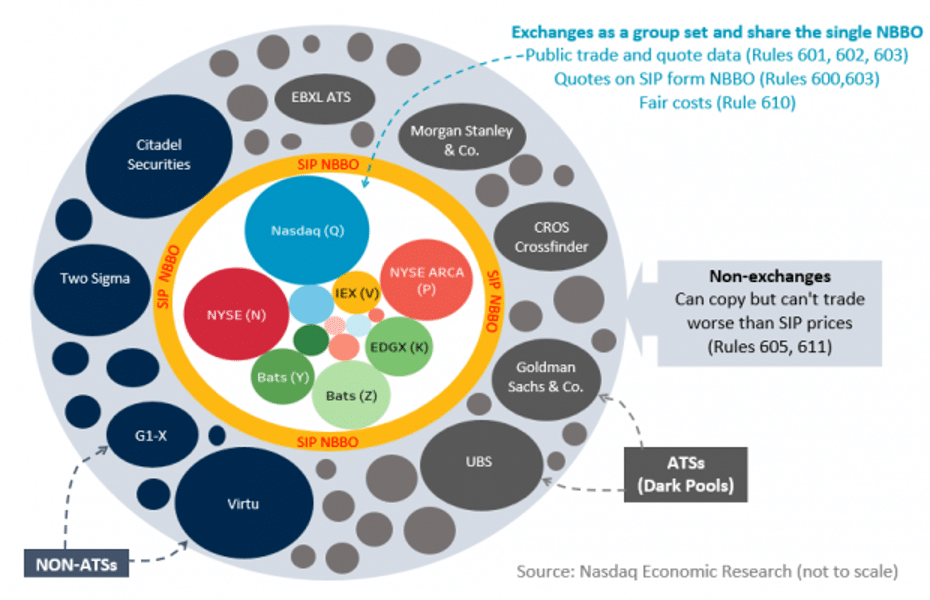

Where do prices come from?

Despite this complexity and fragmentation, regulators in 2005 created a consolidated national best bid and offer (NBBO). Think of it like Priceline (Nasdaq: BKNG) for stocks. Even if the best bid and best offer were on different markets, the NBBO shows investors the combined best prices (Chart 3). To learn more see Reg NMS for Dummies.

Chart 3: Where do prices come from?

Source: Nasdaq Economic Research

Those best prices are shared with investors and the public through a consolidated data feed called the SIP (Securities Information Processor). Not all investors need the instantaneous market-wide best quote – some need more data some need less. So exchanges also issue their own BBOs, some of which compete with SIP data (e.g. Nasdaq Basic has saved users more than $270 million over the SIP feed since its launch in 2009).

But the SIP, and exchanges quotes, are very important as those prices also protect investors trading off exchanges. That’s because off-exchange trades (Charts 3 and 4) must occur at prices no worse than those available on exchanges. For more on the SIP and NBBO and ATS’s read ABCs of U.S. Stock Market Acronyms.

Chart 4: Reg NMS creates a single NBBO out of a network of competitors

What is the trade desk talking about?

Sometimes things on a trade desk happen really fast. Quotes change, prices disappear, and opportunities are missed and misunderstandings can cost a lot of money. So traders have developed jargon to pass on a lot of information in a consistent and unambiguous way.

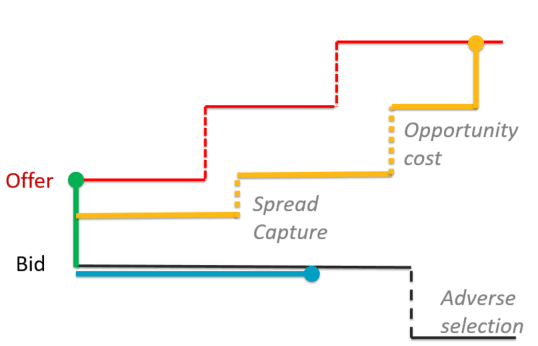

For example, you bid to buy and offer to sell.

The difference between the bid and offer is called the spread (Chart 3 and Chart 5).

That also means every trader has a choice to make and consequences to deal with (Chart 5):

If you want to buy “right now,” you’ll have to pay the higher offer price (lift the offer). Sometimes this is called a “market order” as it will trade at whatever the market price is.

But if you prefer to save some money, you’ll need to use a “limit order,” probably at the bid (which is a “marketable limit”) as lower prices will not attract sellers. Then you need to wait for sellers to cross the spread (and “hit the bid”) to get to the top of the queue and eventually a fill (trade).

The problem with being patient is sometimes the price goes up before you get to trade (red line). That can mean you’ll end up paying (even) more than the offer, something known as “opportunity cost.”

Of course the opposite can happen too, and prices can fall. Although that means you get your fill (trade) and save the spread, it also would have been cheaper to wait for prices to fall. That’s called “adverse selection.”

There are also midpoint orders. Paying half the spread can seem like a good compromise between the costs of market (price taker) and delay of limit (price maker) orders. However midpoint orders are also “hidden,” meaning they are not publicly displayed on the SIP. That means sellers won’t know you’re there, which signals less, but hiding also means you might wait even longer for a fill.

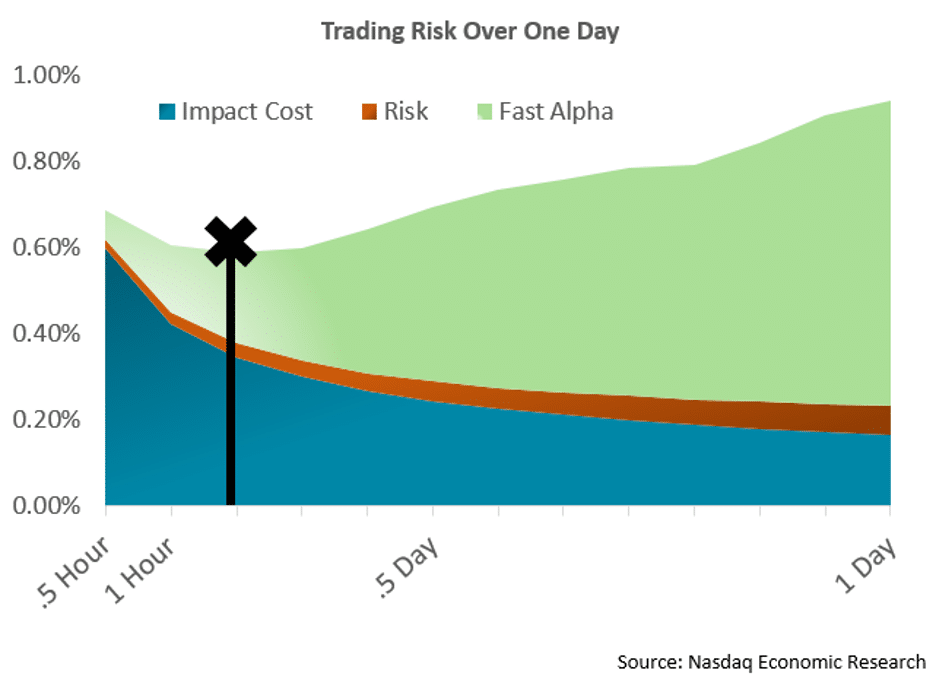

Although this all sounds complicated, the reality is that computers (trading algorithms) are able to handle much of this for human traders. The key input from the trader is to tell the algorithm how fast you need to trade.

The problem for the trader is that:

The faster you trade, the more you will cause market impact (a buyer will add to demand, which makes prices go up).

The slower you trade, the more others will take all the good prices (opportunity cost when other traders make prices go up anyway).

As we discuss in How Fast Should You Trade?, the right speed depends on assessing how many other traders are likely competing for your order, as well as how large your order is compared to typical daily supply.

Chart 6: Optimal speed to trade-off impact and opportunity cost can be mathematically determined

Do all stocks trade the same way?

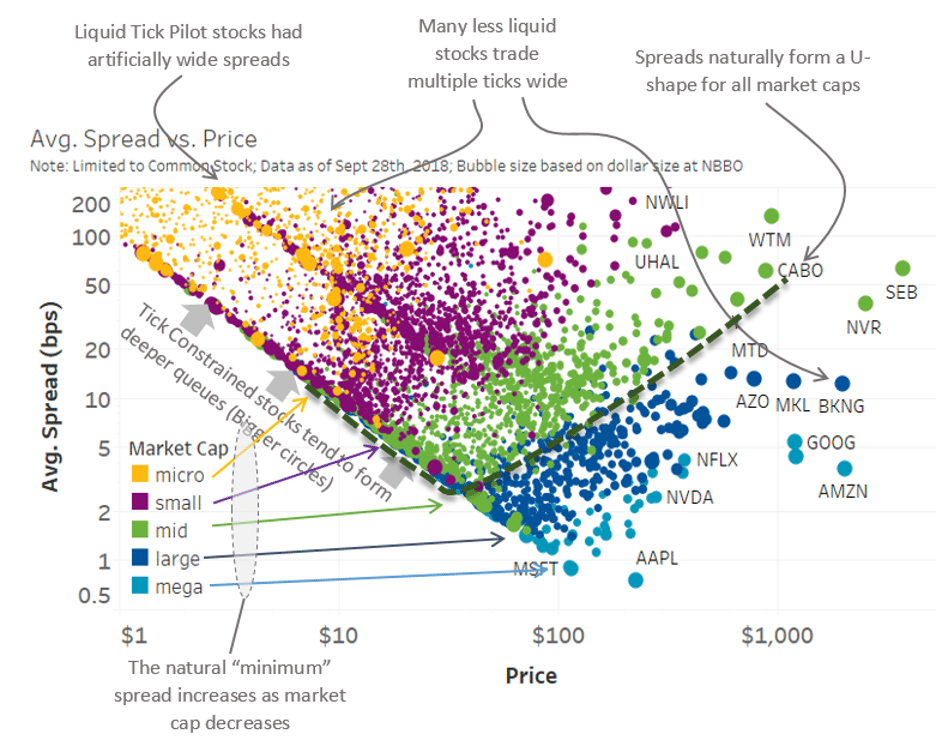

No. In fact experienced traders (and algos) will modify their strategies to suit different stocks characteristics.

A combination of liquidity, spread and volatility affect the returns market makers earn for providing liquidity. Because each stock can quote no better than a one-cent spread, that spread is worth more on a $1 stock than on a $1,000 stock. That changes the attraction of limit vs market orders, which in turn affects the length of queues which in turn leads to other ways to buy queue priority.

But liquidity itself is mostly driven by the size (market cap) of a company (with a little boost from periods of volatility).

Chart 7: Liquidity (in $) is a key driver of spreads, but so is the one-cent tick

Source: Nasdaq Economic Research

How fast do stocks trade?

Almost all large investors will “work” their large orders, in many smaller pieces, over a long timeframe; sometimes days.

However, almost all orders that enter the market these days are worked by computers. That means orders will be entered, or trades will be filled, and prices will be updated in less than one-thousandth of a second (a millisecond). In fact, the actual matching of trades happens in microseconds (millionths of a second), most of the rest of the delay is due to the speed of light. Learn more about that in Time is Relativity: What Physics Has to Say About Market Infrastructure.

Where to next?

U.S. equity markets are fragmented and complex. That’s for sure.

But they are also the largest and most efficient markets in the world. That’s thanks to all of the participants in the ecosystem competing and playing their part in capital formation, liquidity provision, risk transfer and price efficiency.

When done right, all participants benefit from lower trade costs, higher valuations and deeper liquidity.

There is data to prove it. If you’re interested, you can see more of what we’ve learned from the data here.

COVID-19 wreaked some degree of havoc on the exchanges and business of trading.

While some operators were able to maintain status quo operations others, such as the New York Stock Exchange and Cboe Global Markets had to shut their physical trading floors and shift gears away from voice trading and open outcry amid the COVID-19 pandemic.

Temporarily.

The Cboe’s historic open outcry C1 trading floor was shuttered on March 13 and then amid new precautions and safeguards oon June 15. Bryan Harkins, Executive Vice President and Head of Markets at Cboe Global Markets, spoke with Traders Magazine Editor John D’Antona Jr. about the reopen process.

TRADERS MAGAZINE: How did the re-open go?

Bryan Harkins: The Cboe team worked tirelessly to prepare for a safe and seamless reopening of our trading floor. After a tremendous lift involving nearly all departments across our company, we accomplished what could only be described as an extremely successful reopening of the floor. Turnout on Day 1 was outstanding. Although not at the capacity of a typical day prior to the closure, all the designated market maker and broker spots were occupied, and nearly all TPHs (Trading Permit Holders) who had committed to returning on Day 1 were present. The safety protocols we’ve implemented – separate north/south entrances, medical screening at entry points of the building, required face coverings, and assigned spots on the trading floor – worked as designed and traders adhered to our guidelines.

To provide further context around the success of our first day returning to the floor, approximately two million combined contracts were traded in SPX and VIX options – of which about 717,000 contracts were executed via open outcry – on what was a relatively slower market day. Additionally, Cboe Options Exchange had the highest market share of any venue in the multi-listed options space. Notably, this was all achieved at just half of our traditional capacity – with just over half the usual number of traders allowed on the floor due to capacity limits to ensure social distancing.

TM: How will open outcry work with social distancing?

Harkins: Despite any initial apprehensions from the trading floor community with the new floor reconfiguration, open outcry trading is working just as well in our new floor environment – even with social distancing requirements. While we acknowledge the new layout could be an adjustment for some, feedback has been overwhelmingly positive. We’ve heard the ability to hear is better than expected, and multiple TPHs remarked that the new floor layout with enhanced safety provisions was “surprisingly good,” and “working much better than expected.” Brokers have also told us they are getting busier and have access to a good number of market makers.

This is testament to the work that the Cboe team did to prepare for a smooth reopen – beginning with discussions in April, followed by three virtual Town Halls with our floor trading community. We developed a “TPH Playbook” detailing standards of conduct in the new trading environment, and rigorously tested equipment with our TPH members, brokers and market makers on the newly reconfigured floor prior to reopen. We’re pleased to have restored the benefits of our hybrid exchange with both open outcry and electronic trading, while putting the health and safety of our trading floor community first.

TM: Are there any order types or tools unavailable to traders?

Harkins: Trading floor personnel on our redesigned floor have access to all the tools and functionality that they had prior to the temporary floor closure – and in certain cases, plus some. Brokers, for example, are able to have more equipment, such as laptops, than before given the larger space in the newly reconfigured trading floor layout. Several trading features were disabled when we transitioned Cboe Options Exchange from hybrid to all-electronic trading mode. Upon the reopening of the trading floor, those features have been reimplemented. These changes have brought the trading system back in line with functionality prior to the floor closure in March.

Conversely, when Cboe moved to fully electronic trading with the closure of our floor, we delivered some electronic solutions to replicate the benefits of floor trading. As a result, our markets continued to function well and allowed investors to express their views and manage risk throughout this period of extreme market conditions.

TM: Is there a ban on public transportation for those seeking to come back?

Harkins: At this time, we recommend that all trading floor personnel – including Cboe associates and TPHs – find alternatives to public transportation. This recommendation is a part of our health and safety protocols, consistent with guidelines provided by public health agencies to encourage social distancing and to protect against the risk of exposure to COVID-19 in public spaces. Out of the gate, we have taken an abundance of caution approach, but may modify our TPH Playbook to keep current with the latest guidelines from public health officials. Our commitment is to continually inform our TPH members of any updates.

TM: Who was allowed back? Floor brokers? Specialists? Those firms in dire financial need? Who did Cboe invite? Or is it up to the member firms themselves? How did Cboe approach firms about returning?

Harkins: During the temporary trading floor closure, many TPHs eagerly awaited a return to hybrid trading at Cboe and expressed interest for the floor reopening. The decision to return to the floor was ultimately with the TPH firms, who also determined which staff they would send back. On the other hand, there may have been firms who chose to have their employees continue working from home, and not return to the floor immediately upon reopening. Accordingly, any market-maker spots in the SPX trading pit that remained vacant were placed in a lottery for firms interested in having a larger presence on the floor. Winners of the lottery are entitled to temporarily occupy the trading spot, until staff from the TPH organization originally assigned to that spot returns to the floor.

TM: How has the re-open gone so far?

Harkins: We kept the reopening of our trading floor low-profile, instead focusing on our internal operations – both in terms of the trading day and the extensive safety protocols – to ensure a smooth reopen. I’m pleased to report that the reopen, and the weeks since then, have gone extremely well and as planned. The work of the Cboe team has been incredible in getting us to this point.

We continue to monitor trading activity. As expected, floor-based volume returned slightly below pre-closure averages, but has trended upward since we reopened on June 15th. We remain vigilant in monitoring the latest developments of the evolving COVID-19 crisis. The health and safety of our trading floor community – and all Cboe associates – remain our highest priority and will continue to guide our decision-making going forward.

Since their inception in the early 2000s, fixed income exchange traded funds (ETFs) have always sparked debate among financial markets professionals. Advocates point to the ability to gain instant exposure to a broad range of securities with lower transaction costs and, in some cases, better overall liquidity than the underlying bonds themselves. Detractors warn that the potential for a liquidity mismatch between the ETF and its underlying products could create a recipe for trouble during periods of heightened volatility.

Who’s right? Tradeweb recently assembled a panel of experts on the topic to examine the performance of fixed income ETFs over the last several months of COVID-19-inspired volatility, taking a close look at how the asset class performed throughout some of the most challenging conditions we’ve seen since the Global Financial Crisis. Their consensus: fixed-income ETFs have passed the test.

By-the-Numbers: Weathering the Crisis

Steve Laipply, U.S. Head of iShares Fixed Income ETFs at BlackRock kicked things off by explaining that the asset class has become an integral part of the fixed income ecosystem. Breaking it down a bit further with hard data, fund flows throughout the COVID-19 crisis were significant.

“As of February of this year, we had about $31 billion in net inflows into fixed income ETFs. In March, during the height of the COVID-19 crisis, we saw $18 billion in net outflows,” Laipply explained. “Then, as stimulus measures were announced, we saw a turnaround of $20 billion in inflows in April and $30 billion in May. All told, we’re roughly $60 billion net positive inflows for the whole period.”

He added that fixed income ETFs functioned as a strategic tool for institutional investors during the crisis – particularly in credit markets – with broker dealers, electronic trading platforms and market makers routinely using fixed income ETFs to manage inventory, facilitate large client trades and hedge risk.

Tradeweb’s Iseult Conlin, U.S. Institutional Credit Product Manager, added more context on how market participants have been tapping into multiple asset classes to find liquidity during the crisis: “One of the advantages of Tradeweb is the fact that we are a multi-asset fixed income platform operating in forty different markets. So, traders using our platform can simultaneously send a request for quote (RFQ) list of corporate bonds while also trading an ETF. That seamless flexibility has been important, particularly in periods of heightened volatility, where we see traders becoming well-versed in many different products and trading across asset classes to find liquidity.”

A Bright Spot in Stressed Markets

Looking beyond fund flows to actual fixed income ETF performance during the crisis, the panel focused on the critical role the asset class played in providing liquidity.

BlackRock’s Laipply provided context: “During the height of volatility in March, where we saw spreads blow out from 100 basis points to 375 basis points in investment grade credit and from 300 to 1,100 basis points in high yield, fixed income ETFs stepped into the gap in liquidity in the underlying bond market.”

To put this in perspective, BlackRock traded roughly $1.3 trillion in fixed income ETF volume in the first quarter of 2020. That compares with $2.6 trillion for all of 2019.

“We saw roughly 50% of all of 2019’s volume trade in the first quarter of 2020 alone. The fact that all of this trading activity was occurring against a backdrop of very stressed underlying markets shows that investors were able to turn to fixed income ETFs at a time when they were having real difficulty moving trades in the underlying over the counter markets,” Laipply added.

Matheus Lara M. Pereira, Head of Trading at Flow Traders echoed this sentiment, sharing examples of trades that were stalling in the underlying bond markets, but moving freely in the ETF market: “We were seeing clients unable to execute a $100 million inflation TIPS basket on the underlying product and then turning to get pricing on similarly sized blocks of TIPS ETFs that were able to be executed immediately so they knew exactly what price they were getting and then executing via the Tradeweb platform to get the best price. It was much more efficient and easy to price by accessing that risk in the ETF market than in the underlying bond market.”

Tradeweb’s Conlin added that the velocity of trading increased significantly during this crisis, thanks largely to improved transparency offered by the ETF market: “Liquidity was very challenged in March in underlying cash bonds, particularly on the front end. Corporate traders on Tradeweb leveraged fixed income ETFs to gain insight into pricing and liquidity and as a diversified trading strategy – other than RFQ or voice protocol – to move risk in the underlying corporate cash market.”

Conlin added that newer trading technologies also played a role in helping to spur liquidity when markets were severely stressed at the height of the pandemic. Specifically, Tradeweb saw a large uptick in usage of its portfolio trading protocol – which allows investors to price hundreds of bonds in one basket, negotiate a price at a portfolio level with multiple dealers and execute the trade in a single transaction. “That was a real departure from previous crises, where traders would typically revert back to ‘conventional methods of trading’ via voice. With this crisis, traders doubled-down on technology as the most effective means of finding liquidity.”

“If you think about how the bond market is modernizing, it’s really all about technology. We tend to think about fixed income ETFs as a technology, but the infrastructure that’s being built to either support or make trading itself in single names or portfolio trading is a very key component of this,” Laipply added. “This was a very powerful stress test. We have strong conviction that fixed income ETFs will pass this test.”

Click here to access a recording of the full panel discussion.

Javier Hernani Burzako, CEO, Bolsas y Mercados Españoles (BME)

Bolsas y Mercados Españoles (BME) has joined forces with Barcelona Tech City to create a new fintech hub for start-ups, investors, venture capital, traditional banking and insurance companies.

The hub, located in the Barcelona Stock Exchange building, aims to provide fledgling companies with access to financing opportunities via the close relationship with BME. The exchange will advise firms on their growth path through its market infrastructures, such as the Stock Exchange, its SME Growth Market MAB or its Pre-Market Environment.

MAB is a market for small companies looking to expand, with a special set of regulations, designed specifically for them with costs and processes tailored to their particular characteristics.

The aim is to create an optimal environment to make the sector more dynamic and create synergies throughout its value chain.

Javier Hernani, CEO of BME, states: “This alliance allows BME to be closer to companies deeply-rooted in trends and disruptive value-added services. This reality broadens BME’s options to increase the number of companies in its markets, participate in technological solutions useful for its business purposes and evaluate technologies that can be incorporated into its range of services.”

Due to the Covid-19 health crisis, the incorporation of the new space to the Urban Tech Campus is expected to go live in 2021.

Miguel Vicente, president of Barcelona Tech City

Miguel Vicente, president of Barcelona Tech City, states: “The agreement with BME offers us the opportunity to explore new financing alternatives for our start-ups. The Pre-Market Environment and the MAB are growth opportunities to be considered for the ecosystem companies.”

The European Securities and Markets Authority (ESMA) has published its first two review reports on MiFID II’s transparency regime.

The first report reviewed MiFIR implementation for equity instruments and recommended amendments to pre-trade transparency regimes to reduce the use of reference price waivers, and a more clarified scope of the trading obligations for third-country shares.

The regulator also proposed an increase of minimum quoting obligations and an amended methodology for determining standard market sizes, as well as transforming the double volume cap mechanism into a single volume cap by removing the current trading venue threshold of four percent.

ESMA’s second report assessed the pre-trade transparency obligations applicable to systematic internalisers in non-equity instruments.

In relation to the qualitative assessment of Article 18, it advised continuing publishing liquid instrument quotes, but removing the requirement for illiquid instruments to provide better harmonisation.

Both reports aim to simplify the current transparency regime while also improving its availability based on market participants’ feedback.

Steven Maijoor, chair of ESMA

Steven Maijoor, chair of ESMA, commented: “The reports shed light on existing limitations to transparency and, at the same time, clearly demonstrate ESMA’s ability to deliver concrete recommendations based on the data following the implementation of MiFIR.”

“The proposals aim to simplify the transparency regime and increase transparency available to market participants. These important reports provide a solid foundation for any review of the MiFIR transparency regime in the future”.

ESMA noted that considering the current developments concerning COVID-19, it has agreed to extend the consultations and questionnaires on the delivery of MiFID II review reports.

The House of Lords EU Services Sub-Committee has written to the City Minister John Glen MP about UK-EU equivalence decisions, future UK-EU regulatory co-operation and the role for Parliament in the UK’s future regulatory framework for financial services.

The letter asks several questions such as – When will the Government’s own equivalence decisions be announced? Will these only be published alongside the EU’s decisions? How would the voluntary regulatory framework mooted by chief EU negotiator Michel Barnier differ from the structured dialogue being proposed by the Government?

It further wants answers to – “What further reassurances can be given that such a structured dialogue would not “severely limit the EU’s regulatory and decision-taking autonomy”, as suggested by Mr Barnier?

The UK and European Union are trying to hammer out an equivalence deal, but to date there has been little movement and there are fears in the City of London that the UK will leave the EU without a deal. This would mean that UK based financial service firms could lose access to the European markets overnight and find themselves unable to serve their EU clients from London.

Michel Barnier, Chief EU negotiator

The European Commission (EC) has said that at the end of the Brexit transition period on 31 December 2020, the MiFID framework for investment services and activities will no longer be applicable to the UK.

The announcement was made in a notice to stakeholders regarding the withdrawal of the UK and EU rules in the field of markets in financial instruments. It states that if an agreement were in place, it would create a relationship that will be quite different from the UK’s participation in the internal market.

The commission said at the end of the transition period, UK investment firms will lose their EU passports and will become third-country firms, which means they will no longer be allowed to provide services in the EU on the basis of their current authorisations.

It also confirmed that UK market operators/investment firms operating a trading venue or execution venue will no longer benefit from the MiFID authorisation/licence. In other words, UK-based regulated markets (RMs), MTFs or systematic internalisers (SI) will no longer be eligible venues for trading shares subject to the MiFID II share trading obligation (STO).

EU counterparts will also not be able to undertake trades in shares subject to the STO on such platforms, according to the Commission.

The same restrictions will apply to UK-based RMs, MTFs or organised trading facilities who will no longer be eligible venues for the MiFIR derivatives trading obligation and EU counterparts will no longer be able to undertake trades on these platforms.

Jannah Patchay of Markets Evolution advises firms to keep their eye on the ball and not let Covid divert their attention from the job at hand.

In light of the current global Covid-19 pandemic, with the UK and much of Europe in varying forms of lockdown, and very much focussed on preserving national economies and interests in the short term, one might reasonably expect that the UK’s impending departure from the EU might be delayed once again. Yet this is clearly not the case, at least from the UK’s perspective: the current government, elected on its pledge to “get Brexit done”, appears to remain entirely committed to delivering on this commitment come hell or high water. From the EU’s perspective, member states are looking inward, and lack the will or capacity to deal with complex and often-tedious Brexit negotiations at present. This poses an existential challenge to any potential Brexit deal – with one side increasingly gung-ho, and the other unable to commit fully to the negotiating table, are we once again headed for a hard Brexit?

Many financial institutions, perhaps encouraged by the last-minute sprint on both sides to a successful negotiation of the Withdrawal Agreement in 2019, have quietly paused their Brexit plans and programmes. Others, particularly those whose business models rely on access to European markets and clients, but which also lack the size and scale to commit the resources required for a full Brexit contingency plan, may never have kicked off these programmes in the first place. Some firms may even be hoping that an equivalence agreement for financial services will still be possible, given it is a process enshrined in MiFID, applicable to any third country, and therefore, in theory at least, separate to any other Brexit negotiations.

Whilst the general public might be forgiven for not fully understanding the impact of a hard Brexit on financial services, it is still surprising that many participants in the space do not fully appreciate the consequences for their firms and business models. It’s worth taking a look at what “equivalence”, from a financial services perspective, actually means, and clearing up some of the misconceptions associated with it.

An equivalence determination can only be made where there is a legislative provision for it. Financial instruments, including equities, bonds and derivatives, are governed by the EU’s Markets in Financial Instruments Directive (MiFID), in which equivalence is a concept that is clearly defined and provided for. However, the core banking activities of deposit-taking and cross-border lending are governed by the Capital Requirements Directive (CRD), which has no provisions for an equivalence framework.

Similarly for payments and e-money, governed by the Payment Services Directive (PSD) and the E-Money Directive (EMD) – there is simply no concept of equivalence for these activities. Firms providing services under these frameworks must either abandon their EU operations, or establish a local EU base.

Without the legislative provision for an equivalence framework, there is no ability to undertake regulated activity on a cross-border basis into the EU, unless it is subject to the specific exemptions available from individual member states. These must, however, be examined and applied for each member state individually, and there are usually conditions attached – creating a high compliance and operational burden for any UK firm wishing to leverage these as a means of carrying on cross-border business into the EU.

The only other option available for firms is to have a local establishment and authorisation in an EU member state. There are no quick wins here.

Equivalence is a political consideration – the EU has explicitly stated that political motivations can be taken into account when making an equivalence determination for another jurisdiction. Brexit is a political motivation; it’s simply not the case, from the EU’s perspective, that equivalence should be granted to the UK just because the regulatory regimes on both sides are currently identical. Think about it this way: if North Korea copied and pasted all of MiFID into their national law, neither the UK nor the EU would be much inclined to grant them equivalence – not based on the technical assessment, but on the political considerations.

Equivalence is not permanent – it can be subject to review and revoked with only 30 days’ warning. Again, this is not entirely unreasonable, given that both national regimes and political relationships can change.

Even MiFID equivalence is not a free passport into the EU. It is subject to restrictions around the types of clients to which services can be provided – Per Se Professionals and Eligible Counterparties only. MiFID equivalence also doesn’t solve such challenges as trading venue equivalence for the Derivative Trading Obligation (DTO), in which both the UK and the EU require execution of trades in certain derivatives on UK / EU authorised platforms respectively. This creates a Catch-22 situation for counterparties to these trades, and remains the subject of ongoing (again, highly politicised) negotiations.

It’s all going to change anyway. In February 2020, the European Commission launched a long-awaited public consultation on proposed revisions to MiFID II and its accompanying regulation, MiFIR. Amongst the proposals were included a number of changes to the equivalence regime. If finalised, then not only must equivalence determinations be made at the jurisdictional level, but individual firms from equivalent jurisdictions must also register with the European Securities and Markets Commission (ESMA) when they wish to provide cross-border services into the EU. Registration will be subject to the provision of substantial and detailed data on the firm, the nature of its business, its clients and transactions, governance and compliance mechanisms, and much more. Furthermore, this data must be provided on an annual basis for review by ESMA – a huge burden for any firm (not just in the UK, but US and APAC as well) wishing to provide services into the EU.

Once we accept that equivalence is political, it also becomes clear that the current political situation has multiple dimensions, of which Covid-19 is a significant one. Though it’s so far unclear as to the extent to which the EU will take into account the impact of the Covid-19 crisis and lockdowns on factors such as access to foreign capital by European firms and market access for European investors. These may all have repercussions for both the final version of the revised MiFID, as well as for the UK’s equivalence discussions.

Maria Netley, EMEA Secretariat, FIX Trading Community

Covid-19 sent shockwaves across financial markets. All of us have been forced to adapt to the new normal, which for the most part has been successful. However further regulatory change is emerging as policy makers need to adapt to longer term structural changes facing capital markets globally. Here’s how you can help.

Over the past few months the FIX Trading Community has come together several times to consider responses to the recent consultations. Working in co-operation with the industry associations, one of the underlying strengths of the FIX Trading Community is the depth of participation from all areas within the electronic trading industry. This enables FIX to support or recommend changes to regulation that meet the primary goal of supporting free, open and unambiguous standards for electronic trading in the best way possible.

The importance of responding to these consultations cannot be underestimated and for FIX, the involvement of our members is vital. Each consultation will always reflect on thinking about how the market structure proposals relate to all aspects of trading with the ultimate aim of providing free, open and unambiguous standards to the industry, with all the cost benefits that brings to your firm. While providing feedback to regulators on commercial aspects is one for our members to do in their firm capacity, the creation of free and open standards is where FIX can deliver for the industry. If we as an industry fail to address the regulatory changes necessary for data standards, further regulatory change will be inevitable, requiring yet more implementation or risk of potential fines as individual market participants – on repeat until we get this right.

In contrast, if workable and reliable data standards are put in place, the market structure debate will be better equipped for policy makers to formulate future regulation on the back of accurate data, implementing regulatory changes that are truly in the best interests of the end investor.

Without free, open and unambiguous standards and without FIX this industry would be a poorer, more expensive and less innovative place. However, it must not be left to a few individuals to take on this challenge alone and we all have a responsibility to ensure that our firms are represented to contribute to the debate thoroughly and globally. Some working groups can focus on quite technical aspects of the implementation of the protocol, but without this attention to detail the protocol would not be as effective, particularly when taking into consideration the increase in regulatory conflicts.

Failure to participate and the failure to share your specialist knowledge risks sub-optimal regulation which impacts us all. In the 25 years since FIX was first established it is good to note that this is continually improving, but we cannot rest on our laurels and we need to work with all segments of the industry and with the regulators to ensure that this continues to be the case.

As we move into the next round of consultation, the FIX Trading Community is making a significant drive to really focus on the needs of the buyside, in helping them to come together as a community and focus on the elements of their business impacted by regulation.

In an era of extensive scrutiny of the markets and its participants, the obligations upon buyside firms increase almost daily, with client and regulatory reporting often cited as one of their biggest challenges. It is now that these firms need to really understand the immense amount of data that they are receiving and how they can analyse and use that data to provide the best service for their end clients.

Thanks to the work of the EMEA Governance team, FIX Trading is able to have more open debate with the regulators, but it is important to remember that those conversations are only valuable when informed by our membership.

The Investment Management Working Group in Europe is now working through a systematic list of challenges that give buyside firms the opportunity to discuss data in a safe, confidential environment looking into the detail in a way that few other associations are able to focus on.

For the buyside this represents one of the best opportunities for you to help to drive the debate and make your voice heard.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.

Bryan Harkins: The Cboe team worked tirelessly to prepare for a safe and seamless reopening of our trading floor. After a tremendous lift involving nearly all departments across our company, we accomplished what could only be described as an extremely successful reopening of the floor. Turnout on Day 1 was outstanding. Although not at the capacity of a typical day prior to the closure, all the designated market maker and broker spots were occupied, and nearly all TPHs (Trading Permit Holders) who had committed to returning on Day 1 were present. The safety protocols we’ve implemented – separate north/south entrances, medical screening at entry points of the building, required face coverings, and assigned spots on the trading floor – worked as designed and traders adhered to our guidelines.

Bryan Harkins: The Cboe team worked tirelessly to prepare for a safe and seamless reopening of our trading floor. After a tremendous lift involving nearly all departments across our company, we accomplished what could only be described as an extremely successful reopening of the floor. Turnout on Day 1 was outstanding. Although not at the capacity of a typical day prior to the closure, all the designated market maker and broker spots were occupied, and nearly all TPHs (Trading Permit Holders) who had committed to returning on Day 1 were present. The safety protocols we’ve implemented – separate north/south entrances, medical screening at entry points of the building, required face coverings, and assigned spots on the trading floor – worked as designed and traders adhered to our guidelines.

The European Securities and Markets Authority (ESMA) has published its first two review reports on MiFID II’s transparency regime.

The European Securities and Markets Authority (ESMA) has published its first two review reports on MiFID II’s transparency regime.