The Futures Industry Association (FIA) and the International Swaps and Derivatives Association (ISDA) are calling on European regulators to exempt derivatives from the settlement discipline regime (SDR) of the Central Securities Depositories Regulation (CSDR) because they are already covered in existing rules frameworks.

In a joint position paper, the trade bodies stated that they are concerned that “the CSDR settlement discipline regime was not drafted with derivatives transactions in mind” and that applying these requirements would” overlap with – and undermine the risk-mitigating purpose of – derivatives-specific requirements such as margin rules under the European Market Infrastructure Regulation (EMIR).”

The CSDR, which aims to improve the settlement process, has been postponed until February 2021 from this September. Two of the most contentious issues are the mandatory buy-in regime which will be initiated in the event of a transaction failing and the SDR which introduces fines for settlement fails when securities are not delivered.

The trade bodies state that a buy-in or the imposition of cash penalties where a transfer of “such financial instruments as margin fails to settle would likely increase the receiving party’s exposure to the posting/failing counterparty”.

The paper adds that such situations are “already dealt with effectively in industry-standard documentation” for both cleared and non-cleared derivatives.

They contend the SDR “would have exactly the opposite effect to the risk-mitigating purpose of regulatory margin requirements. The timing of daily margining requirements would also render a buy-in ineffective in this situation.”

Although the trade bodies acknowledge that the terms of CSDR’s SDR have been in place for some time, they argue that “a number of new practical considerations and concerns have come to light in recent months as market participants have turned to consider the detailed practical implications of the regime for derivatives transactions”.

They request EU regulators quickly clarify their position on whether derivatives fall within the jurisdiction of CSDR and if they are unable to, then to alternatively consider an additional delay to allow more time for analysis into the various red flags that have so far been raised by the industry.

TriOptima, an infrastructure service provider, has extended data connectivity between its triResolve platform and the Depository Trust & Clearing Corporation (DTCC) Global Trade Repository (GTR) service.

The aim is to help market participants validate their reported securities financing transactions as they prepare to comply with the Securities Financing Transactions Regulation (SFTR), which is set to come into effect for phase-one and two reporting on 13 July.

The enhanced initiative enables firms to compare and align DTCC GTR trade records with their reported data fields in triResolve, allowing users to quickly identify and address any discrepancies, as well as amend reporting more quickly.

Raf Pritchard, TriOptima

“From margin-lending transactions on a daily basis, to numerous collateral updates and valuations, market participants face a huge task when it comes to reporting,” says Raf Pritchard, Head of triResolve. “This collaboration with DTCC is an important step to ensuring accuracy of data in the repositories for a traditionally under-reported part of the market.”

Val Wotton, Managing Director, Product Development & Strategy of Repository & Derivatives Services at DTCC adds, “As Europe’s largest trade repository, we remain committed to working with third-party providers to help the industry prepare for new regulatory reporting requirements. The extension of our relationship with triResolve to cover securities financing transactions is key to achieving our goal of promoting greater common standards across the market while providing greater value to our clients.”

SFTR is a two-sided reporting requirement, with both borrower and lender required to report their side of the SFT to an approved trade repository on trade date +1 (T+1). Market participants are fully responsible for the accuracy of information when reporting their repo and securities lending transactions to TRs either directly, or through a delegated third party.

TriOptima and the DTCC joined forces in 2014 with a reconciliation service in attempt to resolve a continuing problem of trades being unmatched at Europe’s repositories under the European Market Infrastructure Regulation.

Virginie O’Shea talks to Shanny Basar about branching out on her own, creating engaging research and staying the course

Virginie O’Shea has a Master’s degree in English Literature from the University of Edinburgh which may help in her mission to prove that research does not have to be boring.

She founded her own capital markets research firm this year in order to achieve this aim. O’Shea said: “The name, Firebrand Research, comes from my beliefs in being passionate about supporting change by providing relevant and actionable research.”

Before launching her own company, O’Shea worked at research and advisory firm Aite Group. By the time she left Aite, she was a research director leading the Institutional Securities & Investments practice which involved setting the strategy for the division while managing a team of analysts around the globe. O’Shea commented: “I was at Aite for more than eight years and loved working there but I had moved up as far as I could in the organisation and it was time for a change.”

She believes research should be more digital and easier to access than a 100-page pdf.

“I have listened to consistent client feedback over the years and research really needs to be more interactive and engaging,” O’Shea added. “Research doesn’t have to be boring!”

She highlighted current trends in capital markets that have been caused by the Covid-19 pandemic including the need to meet compliance requirements in a remote environment; to bolster cyber security and to accelerate the move to the cloud.

“Tier-1 banks generally have less than 10% of their total technology stack in the cloud and this makes remote access more challenging,” said O’Shea. “However, regulators are also looking at concentration risk among cloud vendors and there is a real push to ensure that firms aren’t locked into one provider.”

Technology lag

Another trend is that technology progress lags significantly in some areas, especially outside the front office. For example, there are parts of the middle and back office that still use faxes and O’Shea noted that the industry is still having the same year-in, year-out conversations about automation of areas such as corporate actions. “The pandemic has highlighted legacy technology challenges further, but change will take time and investment,” she said.

On the positive side, O’Shea noted that the pandemic has also shown the resilience of financial market infrastructures and that much of the post-financial crisis derivatives reforms have worked relatively well to mitigate counterparty risk.

“However, there have been negative impacts on liquidity. Some collateral strategies have been under pressure and there has been an increase in trade failures due to manual processes,” O’Shea added. “There needs to be a more holistic and joined up approach to treasury functions, repo and securities lending in the future to prevent collateral or liquidity shortages.”

A survey by derivatives trade association ISDA and consultancy Greenwich Associates last month, for example, found that 96% of UK-based swaps market participants experienced a decline in overall interest rate swap liquidity in late February and early March before government intervention. The report said: “Nevertheless, the cause was not one of market functioning, as it was in the credit crisis.”

O’Shea continued that an area of likely concern for the buyside is the European Union’s proposed regulations for environmental, social and governance (ESG) financing.

“The regulations will be onerous and affect even the smallest fund managers, many of which are not focused on ESG at all,” she said.

A final trend is the pushback on rising market data costs in the US and globally.

Career

O’Shea explained that she fell into finance a couple of decades ago after writing about the insurance industry and becoming interested in technology as people were exploring different ways of doing things.

“Research looks at how people and culture affect change which is fascinating and as an advisor/analyst you can often provide a neutral voice to sort out problems, which can be helped by being a woman,” she said.

However, O’Shea has also walked into meetings with a male colleague from sales and been ignored due to the assumption that he was the analyst in the room.

“My advice to women is to stick to your guns, which can be challenging,” she added. “Sometimes you have to work harder as a woman to prove your capabilities but there is a support network out there.”

She also encouraged reaching out to other women, both internally and externally. “We can share war stories and support each other,” said O’Shea.

Diversity

Another impact of the Covid-19 pandemic is that it has shown the importance of flexibility and O’Shea believes more working at home should lead to a more diverse workforce in the future.

“The number of women in finance has not increased far or fast enough,” she said.

She noted that it is positive to see firms such as Fidelity International introducing parental leave as equality has to go both ways.

“All-white, male panels in this century frustrate me, especially as more diversity leads to more interesting events and better business decision making,” added O’Shea.

She remembered being on a panel at Sibos, an industry conference, a few years ago with the first black female US navy admiral who said the only role model she had when she joined the navy was Lieutenant Uhura from Star Trek.

O’Shea concluded: “We need to see more women on stage to demonstrate that there are women leaders in the industry.”

By Christian Schoeppe, Managing Director & Founder, SchoeppeFX

When it comes to Foreign Exchange (FX) trading the Covid19pandemic uncovered that many institutional investors are not positioned at the level they could potentially operate at. At SchoeppeFX International Consulting we have seen an increased demand of asset & wealth management clients to identify and leverage new potential for value creation and cost reduction through innovation and automation in a new work 2.0 environment.

This new remote-working and travel-ban environment has forced institutional investment managers even more to rethink the way they assess internal & external clients, platforms and service providers. Although most FX trading operations have been functioning well since March, amongst buyside end-clients it is still frequently observed that a lot of digitization projects e.g. are carried out ineffectually without exploiting its full potential. Additionally, unlike many other industries financial services have been a latecomer to the paradigm shift towards flexible working structures and working from home.

Areas of Focus

Christian Schoeppe, SchoeppeFX

Therefore, the need for dedicated next level currency consulting has taken center stage. As a result of the pandemic situation clients across the globe are increasingly looking for updated means to ensure excellencein FX trade management across four key service areas: strategic consulting, operational excellence, collaboration, and risk control.

Analyzing the individual FX setup of our clients from scratch is the key primary element in order to subsequently establish technology and processes at a cutting-edge level across the FX value chain, covering all areas of interaction with clients, liquidity providers, portfolio management, operations, and compliance.

Buyside clients want to be able to select an order management system, or a foreign exchange provider, or a trading solution that really fits and improves the way they work, focused on increasing interoperability and performance whilst reducing manual interaction and execution slippage. A detailed holistic look at the FX value chain helps such clients in answering strategic questions right from the beginning.

Strategic Consulting

During and after the Lockdown strategic business reviews across our target client base indicated clearly what has worked and what has not across front, middle and back office functions – e.g. in the areas of: asset & wealth client services, active and passive overlay, treasury & portfolio trading or embedded FX execution. In general, buyside clients tend to benefit from greater flexibility of their underlying FX trading business model if they treat FX as a dedicated asset class instead of a side-product of traditional asset classes like equities, fixed income or real estate.

The decisive question for corporates and investment managers in these times is: do they just want to return to the status quo before the pandemic or are they able to significantly improve their trading set-up and bestexecution framework for FX? Future winners will continuously strive to optimize business results and systematically increase the trading performance of their investment concepts. This includes re-evaluating platform processes and in- & outsourcing decisions for asset & wealth managers as a must.

Mostly affected by this new paradigm shift is the operational set-up of clients. Investment managers are mostly concerned about controlling costs in volatile markets, followed closely by a focus on risk and compliance issues, and support for expansion into new markets.

Operational Excellence

Various analyses of structuresandprocesses in buyside FX trading have shown ongoing deficiencies in terms of system integration, automation and cloud-based solutions. During the pandemic a lot of corporate and investment clients across the industry were able to observe digitization gaps and areas of improvement in technology set-ups, cross- functional workflows and controls.

This necessitates conducting a bottom-up healthcheck of transaction management and cost analyses (TCA) to uncover hidden potential for efficiency gains and cost savings.

Subsequently simplifying and automating FX trade flow allows for reducing execution costs by investing in scalable technology to eliminate inefficient operational processes.

This also includes enhanced remote and mobile access to production and UAT trading, execution and settlement platforms. The pandemic uncovered the systems access gap on the buyside not for the first time: more service, tools and functionality provided only to external clients but not to any similar extend to the internal workforce doesn’t help with achieving better overall results in a next level work 2.0 environment.

Collaboration

Taking the FX trading business to the next level requires new forms of cooperation with innovation leaders. Corporates and investment managers now have to keep up even more with any changes within traditional relationships, and in some cases familiarize themselves with new internal and external developments in a different virtual manner. Proactively identifying this challenge will remain essential in the coming months and even years.

Asset and wealth managers today want true flexibility in choosing the best partners for their investment processes, which contributes significantly to ensuring sustainable cooperation and long-term competitiveness as well. Many clients have realized that now is the time to enrich client experience and performance with the help of innovation leaders in the FX industry in order to expand perception and awareness for their products and services in this dynamic environment.

Increasing recognition and reputation through customized marketing, at industry events and trade conferences requires a different approach across regions, locations and applications in a work 2.0 remote & webcast environment than before. Under these conditions, participation in a large, diverse FX community of dedicated experts enables firms achieving real differentiation from competitors.

Conduct & Controls

Last but not least, reputation is naturally created through compliance. The most prominent treasury conduct & control malfunction just happened after the lockdown in Germany and has shown again: too many customers underestimate the risk potential of non-compliant processes in terms of regulation and financial transparency. While more complex data sets are becoming available, new technological tools are increasingly supporting all three control areas of audit, compliance and business.

Outdated or ineffective foreign exchange transaction and risk controls can have fatal consequences for buy- and sell-side trading organizations. All cases of abuse in the past and present have indicated the importance of ensuring that no matter if retail or institutional business all FX trading policies and procedures must meet national and international requirements covering benchmarking, monitoring and reporting.

Conduct is mission critical – we support clients in continuously improving their FX standards from regulation to practice, and in building and developing organizational proof of compliance in order to avoid costly cases, which could be frequently observed over the past years. For example: more and more corporate clients are looking at embracing the Global Code of Conduct for FX now, which had been watched from the distance in this sector for a long time until recent developments.

FX next Level

In summary, any business planning to shift back to their pre-COVID-19 way of operating foreign exchange trading business once lockdown ends will find it challenging to remain successful for corporates and investment managers. Identifying and exploiting new potential for FX value creation and cost reduction has become crucial in a cloud-based industry environment 2.0 to avoid disruption and secure long-term competitiveness.

Our clients are proactively thinking of how to modernize their operations and are turning to innovative providers who are able to give them access to digital tools that automate workflows and support self-service whilst providing the intra-day data and analytics they need for informed decision making. Process and transaction cost analyses facilitate cross-silo performance management and controlling, and show the extent to which trading and treasury setups and results can be optimized to reach the next level.

The ultimate target in next level currency consulting is a tangible increase in future FX trading & investment performance for clients. We expect that many firms will reprioritize their IT budgets, having seen the extreme conditions that are possible, as they will need to brace themselves for any eventuality. The future winners will be those corporates and investment managers rethinking their operating models from a holistic perspective, seeking sustainable changes that can help them drive profitable growth beyond 2020.

The Time is Now.

Christian Schoeppe founded SchoeppeFX in January 2020 following eight years as head of FX Trading (EMEA) at Deutsche Asset Management.

Nasdaq and London Stock Exchange Group have both taken steps to grow the digital asset ecosystem as institutional interest increases.

Last month Nasdaq launched the Marketplace Services Platform which allows users to build new marketplaces across the trading lifecycle, from execution through to settlement, custody and payment, by using cloud-based plug and play components.

Magnus Haglind, Nasdaq

Magnus Haglind, senior vice president and head of product management, market technology at Nasdaq, told Markets Media that firms have traditionally developed their own infrastructure. This included buying hardware, developing software and installing connectivity which could take at least six to nine months, depending on the complexity.

“We have deployed the whole process in the cloud, so thanks to cloud and automation the time to establish and on-board a ready solution is substantially reduced to a few weeks,” he added.

The Marketplace Services Platform facilitates the frictionless exchange of assets, services and information across various types of market ecosystems and machine-to-machine transactions, including, but not limited, to standard financial assets, tokenized assets, credit card receivables, loyalty points, real estate, insurance contracts, gaming and wagering.

Nasdaq’s already established services, including matching, risk management and market surveillance, will be accessible on the platform.

Haglind said financial services firms are ready for a rapid acceleration in their use of the cloud and software-as-a-service. “Security has the same logic as our best-in-class capital markets capabilities and cloud vendors have a secure set up,” he added.

Brad Bailey, research director at consultancy Celent, said in a statement: “We are at an inflection point in the capital markets. Building one’s own technology stack from application to infrastructure, without leveraging a platform with access to an ecosystem of partners for technology, services, cloud is becoming more difficult to justify.”

The Digital Assets Suite is agnostic to the underlying digital ledger technology, is multi-cloud and will also be accessible for marketplaces in Micorsoft’s Azure. Nasdaq is working with Digital Asset, R3 and Symbiont to deliver technology through the Marketplace Services Platform to meet the diverse needs and unique models of tokenized and digital assets marketplaces.

Haglind said: “We are working with firms such as R3 and the digital asset space has matured as vendors are moving into the next phase. We hope the number of partnerships will grow and create a broader ecosystem.”

He explained that some clients will still want to have infrastructure on their premises and take modules such as surveillance while start-ups, such as LEX, will start with the matching engine.

Leading commercial real estate firm @LEX_Markets has tapped @Nasdaq to power its trading platform. LEX will leverage the cloud matching service via the Nasdaq Marketplace Services Platform.

LEX, a commercial real estate securities marketplace that enables investors to invest in individual properties, last month chose Nasdaq to power its trading platform via the Nasdaq Marketplace Services Platform.

Drew Sterrett, co-founder and chief executive of LEX, said in a statement: “Nasdaq’s market leading technology will allow LEX to scale with the sophistication of a global market and helps us achieve our mission of opening access to the asset class for both retail and institutional investors. Properties have historically traded hands over the course of years. Nasdaq is providing us with the technology to make it happen in under a second.”

Haglind continued that smaller traditional exchanges, who do not have a demand for low latency, may also want to innovate in infrastructure for their local markets using the new platform.

“We are not just providing technology for digital assets to Nasdaq but we are reducing barriers for proven infrastructure for the whole market,” he said.

He added that Nasdaq is creating value as this is a big change in how the industry develops software.

“Firms will have access to continuous upgrades, like consumer services, rather than refreshing their technology every three to five years,” said Haglind.

(Thread): Today, @NasdaqTech reveals the new Marketplace Services Platform, providing next-generation marketplace capabilities spanning the transaction lifecycle.

He added there has been interest from both traditional capital markets and other industries for the new marketplace. Nasdaq has a good pipeline and has also concluded a successful pilot for the Football Index, where clients can buy and sell shares in professional footballers.

London Stock Exchange Group

The UK exchange added 169 digital currencies, digital platforms and security tokens to its SEDOL Masterfile service, a comprehensive global security identifier covering 100 million financial instruments, on 22 June 2020.

LSEG worked with Digital Asset Research to put a robust and transparent vetting process in place to determine which digital assets would be added.

James Nevin, head of data solutions, ISD at London Stock Exchange Group, told Markets Media that 30 years ago SEDOL just covered UK equities but has grown to over 100 million securities across asset classes, with about 20 million currently live.

James Nevin, LSEG

He said: “Institutional clients are beginning to invest in digital assets and the addition to SEDOL ensures they can be integrated into workflows like a traditional security.”

SEDOL security codes are global identifiers for securities allowing market participants to match trades more efficiently and reduce operational risk by enabling straight-through-processing. Other uses include portfolio valuation, processing price feeds and for reference data validation as a cross reference to other identifiers and price validation. Users include asset management, wealth management, insurance firms , custodians, data vendors and fund administrators.

Nevin added that the exchange is talking to digital trading venues and platforms about licensing the SEDOL code.

“This will increase transparency and help institutionalise the market as it develops,” he said.

The exchange makes ongoing additions to SEDOL. In the last few years LSEG has added US municipal bonds and is looking to further increase fixed income coverage taking advantage of data from within the group.”

DTCC

In May the US Depository Trust & Clearing Corporation unveiled plans to explore the benefits of digitalization in the public and private markets and whether new technologies can strengthen post-trade processes and reduce risks and costs through two case studies – Project Whitney and Project Ion.

Project Whitney is a prototype focused on exploring the potential for asset tokenization and digital infrastructure to support private market securities, from issuance through secondary markets.

Jennifer Peve, DTCC

Jennifer Peve, managing director, business innovation at DTCC, said in a statement: “The private markets are ripe for increased levels of automation and lack much of the infrastructure that has supported the public markets for decades.”

Project Ion explores whether the digitalization of assets and application of DLT can accelerate settlement and reduce cost and risk for the industry.

Murray Pozmanter, head of clearing agency services and global operations and client services at DTCC, said in a statement: “Project Ion is about working with the industry to further the value proposition on accelerated settlement leveraging new capabilities such as DLT and tokenized securities, and to learn how DTCC can best deploy these technologies to deliver additional value to clients and the industry.”

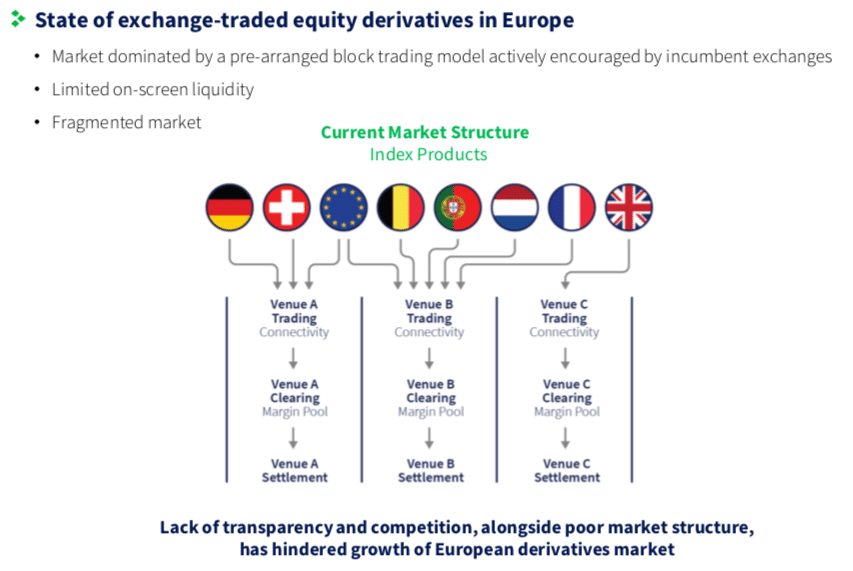

Cboe is bringing US-style market structure for equity futures and options to Europe by launching an exchange with a central order book to provide on-screen liquidity and a single point of access for trading and clearing across the region.

Last week Cboe Global Markets completed its acquisition of EuroCCP, the pan-European equities clearing house. This paves the way for the US group to launch Cboe Europe Derivatives, an Amsterdam-based futures and options market, in the first half of next year subject to regulatory approvals.

David Howson, president of Cboe Europe told Markets Media: “We are discussing competitive pricing and liquidity incentives in the working groups we are running for the derivatives initiative. The sweet spot for the platform is not just about being cost-efficient but offering a single point of access to products, the market model and contract design.”

Cboe's acquisition of EuroCCP marks the beginning of the next chapter for Cboe Europe and, together with EuroCCP, we couldn’t be more excited to further deliver on our pan-European mission by planning the launch of Cboe Europe Derivatives. #DefiningMarketspic.twitter.com/aWrFAS2r7h

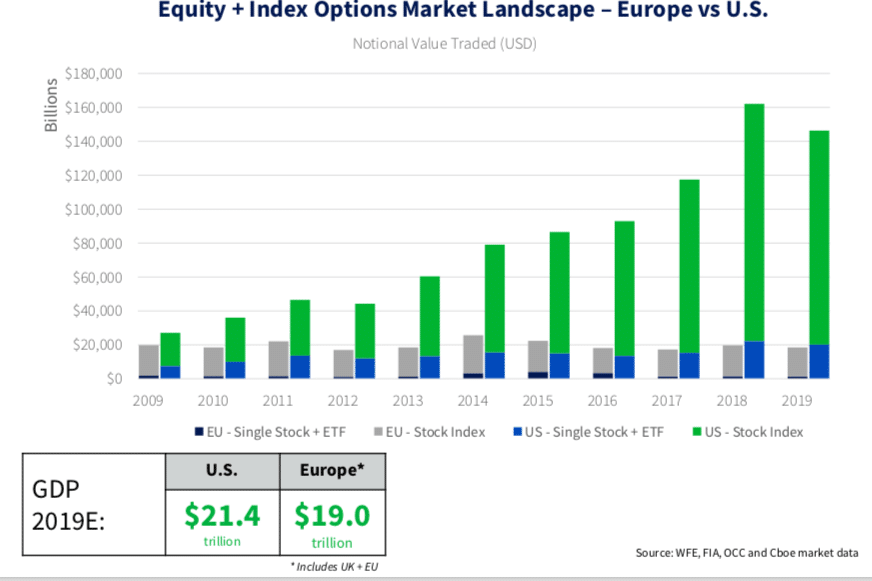

Howson said: “There is a significant difference in size between the US and European equity derivatives markets and significant growth is possible in Europe as there is latent demand from systematic and index funds.”

He said in an investor presentation last week that Cboe Europe is creating a single market for equity futures and options in the region with a market structure that simplifies cross-border trading.

Howson continued that the US and Europe had similar-sized equity futures and options markets in 2009. However since then the US market has grown, while Europe has stagnated due to a lack of competition, transparency and an opaque market structure the favours fragmented over-the-counter trading.

Source: Cboe.

Howson said in the presentation: “There is demand for on-exchange trading such as in the US, which is transparent and quote-driven.”

Kyle Voigt, analyst at financial services broker Keefe, Bruyette & Woods, said in a report that KBW does not believe that Cboe is simply trying to take market share from incumbents.

“Management shared that it had been approached by its customers, including customers in the US, that are looking for more efficient ways to gain country-specific exposure,” Voigt wrote. “So, revenue that Cboe generates from this initiative could possibly be somewhat additive to the overall derivatives pool in Europe, instead of taking market share away from the incumbents.”

Howson continued there are currently three venues for trading equity futures and options in Europe, three clearing houses and three market models with inconsistent contract designs and low liquidity.

Source: Cboe.

Howson added that Cboe Europe can use significant parts of the US trading platform and overlay MiFID II regulatory requirements and specific European functionality.

The new market will initially offer trading in equity futures and options based on six Cboe Europe indices, which will all be calculated using Cboe equities market data.

“The extension of contracts will be customer-led,” Howson said. “We may look to launch single stock futures and options and volatility products are in Cboe’s DNA.”

Ade Cordell, Cboe NL

Ade Cordell, president of Cboe NL, said in the investor presentation that European exchanges had been built as national champions so Cboe is uniquely positioned to launch a pan-European market.

“New market participants want a central order book,” Cordell added. “We are having great conversations with market makers, the sell side and the buy side who have latent demand but cannot deploy capital due to the current market structure.”

Cordell joined Cboe Europe this year to oversee the expansion into European derivatives and leads Cboe’s Netherlands-based exchange which will be the home of the new platform.

Closing the acquisition

Howson continued that it was a fantastic effort from both companies to complete the deal on time as they transitioned to working from home during unprecedented volatility and volumes due to the Covid-19 pandemic.

Cécile Nagel, chief executive of EuroCCP, told Markets Media: “There was no magic to getting the deal completed.”

She said it was down to working even harder, ruthless prioritisation and planning to make sure sufficient resources were dedicated to the deal, as well as good stakeholder management with banks, regulators and former EuroCCP shareholders.

Today, Cboe Global Markets has completed its acquisition of EuroCCP. The acquisition brings together two pan-European organizations that have long championed competition, open access and clearing interoperability in Europe.https://t.co/ucxdvOW8bmpic.twitter.com/zkKZSelLW8

EuroCCP will continue to operate as an independent subsidiary and retain its name and chief executive.

Nagel added that EuroCCP has started building the required derivatives and risk functionality to extend its business from clearing cash equities.

“Our clients are very positive on the benefits of clearing cash equities and equity derivatives on the same platform which could bring efficiencies from a post-trade perspective,” she said. “EuroCCP remains dedicated to clearing equities, which is an attractive business to build on for cash and derivatives.”

The equity central counterparty clears trades from 37 venues, which represent approximately 95% of Europe’s equity landscape according to Cboe. Within this universe, EuroCCP has approximately 40% market share.

The clearing business would have been boosted by the MiFID II regulations mandating open access in the region this year, allowing users to choose where their trades are cleared regardless of the execution venue. However the requirement has been delayed due to impact of Covid-19.

This meeting also allowed 1 year delay of MiFIR Open Access to Clearing requirements. Lets hope this is the last delay colegislators give as otherwise we have #MiFID2 and the #CMU without competition. This misses the set #MIFID2 goals. @EU_Competitionhttps://t.co/VZZummftlK

“The one-year delay to open access is disappointing as both EuroCCP and Cboe are in favour of open and competitive market infrastructures, but there is no short-term impact to our equities business, or plans in derivatives,” Nagel added. “Even when the open access comes into force in July 2021, it will take time and hard work to gain access to venues.”

Revenues

Voigt estimated that the initial new six equity index derivatives could generate revenue of around €424m ($480m), with the majority coming from STOXX 50 trading.

“We think CBOE would need to get to 5% of current equity index average daily volume to break even in this venture, assuming the ongoing expenses related to the trading and clearing platform are near $10m to $15m per year,” he added.

The analyst highlighted OMX Stockholm 30, FTSE MIB in Italy and IBEX 35 in Spain as the next largest equity index derivatives that the exchange could launch.

“We also think Cboe would be interested in launching volatility derivatives on these indices over time if it builds sufficient liquidity in the derivatives market,” he said. “We think this is a long-term strategic play by Cboe, and it will take time to generate revenue.”

Edward Tilly, Cboe Global Markets

Cboe said that as part of the transaction, EuroCCP put in place a committed credit facility of up to €1.5bn. This facility is an important part of a number of new tools and procedures designed to strengthen the firm’s liquidity risk management framework and help ensure EuroCCP continues to meet relevant liquidity requirements under the European Market Infrastructure Regulation (Emir).

Ed Tilly, chairman, president and chief executive of Cboe Global Markets, said in the presentation: “This acquisition is a significant milestone for our European business. Full ownership of a leading equities clearing house not only enhances our current European equities business, but also provides opportunities to diversify our business into trading and clearing derivatives in the region.”

However, capital markets careers can be very long and fruitful despite changing firms. Just ask Brian Fagen, Managing Director Head of Execution Services at BNP Paribas CIB, who now calls BNP Paribas home after almost a decade at Deutsche Bank. At the German Bank he was Head of North American Execution Services Sales.

Last November, Deutsche Bank agreed to transfer BNP Paribas the firm’s global prime brokerage and electronic equities platforms as part of a major restructure. Also, part of the deal was the transition of technology and several key personnel, including Fagen.

Brian Fagen, BNP Paribas

Fagen, in a conversation with Traders Magazine editor John D’Antona Jr., described the ongoing transition from one firm to another.

“The transition started in earnest when the agreement became effective in December of 2019 and will continue through 2021,” Fagen began. “As is typically the case with bringing two franchises together, there are complexities around the integration of technology, platforms and people across a global markets business. While this particular combination includes a wide array of execution and financing products and platforms across multiple regions, our primary focus is maintaining consistency for clients as we progress throughout the transition.”

From a trading perspective, Fagen explained that BNP Paribas is giving clients the optionality of facing itself or Deutsche Bank as their counterparty while still accessing the DB execution platform until it is fully transitioned to BNP Paribas.

And what of the much-publicized Prime Finance business?

“Prime Finance will be a true combination of the strengths of both firms, creating a leading competitor in the industry,’ Fagen said. “BNP Paribas had an existing strength with the highest quality balance sheet and financing capabilities, FX Prime Brokerage, and Cash Prime Brokerage. The DB platform brings a market leading expertise in synthetic prime products including integration with a world class execution platform for our systematic/quantitative client base. We believe this will position BNPP as a ‘go to’ value added provider of Prime Finance capabilities across the complete range of client needs.”

Fagen has been a long-time resident of the trading desk and noted the intricacies of integrating the two separate firm’s groups. He explained that BNP Paribas is focused on building out a truly integrated trading desk model.

“We believe that the next evolution of the trading business will be less defined by the legacy structures of high- versus low-touch or single stock versus portfolio trading, but rather by providers that provide a consistent execution experience regardless of the type of interaction,” Fagen said. “At the core, our clients are either trading a single stock or a portfolio and then decide to execute it themselves or send it to a sales trader for execution.”

BNP Paribas and Fagen are building its new trading business around the concept that execution performance matters, regardless of the way the order is sent by the client, and that they should receive a consistent, high quality execution experience. This includes pre-trade, intra, and post trade analytics, execution consultancy and customization, market color, market structure commentary and other related content. He has a team of senior and experienced execution sales traders who are capable of handling any type of order flow and delivering a differentiated execution experience for our clients.”

“While most sales trading desks are becoming more junior, we have invested in staff that has experience across the legacy high touch, electronic, and portfolio trading products who understand a client’s trading objectives and the execution tools needed to fulfill them,” he said. “The team and execution platform has the ability to add value to the full range of client models including systematic/quantitative trading firms, index and ETF managers, fundamental hedge funds and institutional managers.”

And no trading desk or firm would be complete without technology and a trading platform that is world class. With competition amid the brokers fierce as COVID-19 induced volatility has stimulated trading, it’s a moment BNP Paribas doesn’t want to miss. Fagen explained that the key to all of this is the migration of the Deutsche Bank execution platform over to BNP.

“During the two years prior to the decision to exit equities, Deutsche Bank had renovated the platform from the ground up. This began with new colocation sites at LD4, NY4 and NJ2 and progressed into platform re-writes of DB’s Market Data platform, Smart Order Router, Algorithmic engines, simulation environment, and research frameworks,” Fagen said. “Since the announcement of the transfer of the business to BNP Paribas, Deutsche Bank has continued to invest in the platform and expand upon its reinvigorated architecture.”

To give a few tangible examples, Fagen said Deutsche Bank’s new smart order router combines a large number of variables when it receives an order to determine the most appropriate exchange post at that point in time -when considering the state of those variables- and has proven to reduce the cost to trade for investors dramatically when compared to the old platform. Also, Deutsche Bank DB has re-written its volume forecasting models, an extremely important component to any algorithm, resulting in material improvements in their ability to forecast how much volume will trade on a given day or from the receipt of an order until the close on a single day.

“Finally, Deutsche Bank has deployed innovative research containers which are in the process of iteratively learning how to optimally construct an algorithm based on actions and reactions in the market which are showing quite a bit of promise,” Fagen said. When completed, we believe the combination of these platforms will position BNPP as a unique value proposition for clients in the equity execution and financing business. This will further enhance the existing leadership position the firm holds across the rest of the global Markets franchise.”

With so many extraneous variables affecting the equities markets daily – and even by the minute – traders look for every edge and advantage they can find when routing their orders and searching for liquidity and alpha. Not to mention without giving up their intentions and exposing their order books, traders are often at the mercy of the markets.

But enter OneChronos Markets, a wholly-owned broker-dealer subsidiary of OCX Group. The firm is an independent, venture backed company using cutting edge technological paradigms to enable the next generation of electronic trading. Its new and soon to be opened U.S. equities ATS is designed from the bottom-up to fundamentally address the growing gap between how exchanges & dark pools match trades and how traders think about execution.

According to Kelly Littlepage, Stephen Johnson and Richard Suth, Co-Founders of OneChronos and former Goldman Sachs and Accenture alumni who all spoke to Traders Magazine, said the ATS employs cutting edge artificial intelligence to achieve their common dream of leveraging domain expertise and emergent technologies to make the trading experience more efficient, profitable and clandestine for the buyside.

Most equities market stakeholders agree the “arms race” in today’s market structure creates added frictions, operational risk, and asymmetry in trading opportunities based on speed. Effectively a series of growing “toll-gates” we all pay to trade. Most don’t agree, OneChronos executives said, on the route cause, and ways to address that problem.

“We at OneChronos felt typical “answers” such as speed bumps, special fee structures, and tiering are all small forms of segmentation, basically therapeutics to numb the pain, where addressing the mechanism design of the exchange auction itself is the vaccine,” said Jesse Greif, Chief Operating Officer at OneChronos.

And that is central to OneChronos’ strategy — its point-in-time auction functionality, which attempts to become a “smart market” by using optimization techniques to match counterparties and determine clearing prices. How? The proprietary technology process seeks to maximize price improvement and crossing opportunities while providing traders & broker algorithms “expressive bidding” tools to manage their business-specific execution or risk management objectives directly in the match process.

A smart market? What’s that?

Kelly Littlepage

A smart market, to hear Littlepage and Johnson tell it, is a design for a periodic auction format that uses optimization techniques such as integer programming to solve for a specifically defined objective. Industries like logistics, telecom, airports (think plane gate allocation) as well as government procurement of physical commodities have all in part adopted the smart market concept given their demonstrated ability to address the aforementioned challenges.

To bring the smart market to equities trading could only be accomplished by taking advantage of advancements in computer science and artificial intelligence, and a relentless attention to mitigating information leakage to make “expressive bidding” something that doesn’t introduce an opportunity cost. This is actually where most of our OneChronos’ core IP lies.

In the OneChronos smart market case, Littlepage said his primary objective is to identify and clear the configuration of “winning” orders which would maximize price improvement across all orders and securities in a given auction. The mechanism is also designed in a way that mitigates information leakage, and, true to smart markets, creates unique crossing opportunities that wouldn’t existing otherwise.

The auction process itself is unique. First, the point-in-time auctions occur every 100 milliseconds throughout the trading day – not just once or on demand as other ATS do. Second, the matching engine makes a match priority based on aggregate notional price improvement contributed. All matches are within or at the NBBO spread and at a single clearing price per symbol.

Stephen Johnson

“We offer traders fully customizable constraints, including those spanning multiple orders or securities, directly in the matching engine; such as dollar neutrality, price/quantity indifference and pairs trading,” Johnson said. “Standard order types are welcomed and supported, in addition to those unique to OneChronos.”

In particular, price/time (match priority) continuous markets challenge the goals of execution, and instigate the complex supply chain that now exists to mask execution, breaking orders up, and randomizing their distribution, he added. These are needed given the current infrastructure but come at a cost of diluting the original execution objectives of the investor.

The goal is to put tools in traders’ hands to convey their business specific execution goals, what OneChronos refers to as “expressive bidding,” directly in the matching engine to avoid unintended risks, and hone in on those which are intended.

For example, a trader wants to buy up to $100k of asset ABC only if I can also sell the same notional in DEF at a defined spread (vs. ABC) or greater. Or, expressing indifference between buying 100 shares of asset XYZ at midpoint or 700 shares XYZ at 80% of the spread all within the same auction.

Get it?

OneChronos runs approximately 10 auctions per second throughout the full trading day, or every 100 milliseconds.

Furthermore, Littlepage and Co. have been spending time with the buyside to better understand their use of broker algos, which has immensely assisted in them and their partner discussions with the sell side brokers to complement their algo and routing. This offers them further differentiation of their execution suite.

“Though we’re a broker dealer, OneChronos can only be accessed through (other) Subscriber broker dealers,” Littlepage said. “We designed this very deliberately to partner with the existing ecosystem.”

Richard Suth

OneChronos has already completed its Series A round of financing and has published its form ATS-N with the Securities and Exchange Commission in the first quarter and looks forward to a fourth quarter launch trading US equities.

“Coronavirus pushed out our plans a number of months, like the case with many other businesses, though gave us a great opportunity to further bake our toolset that we’ll provide to users, simplify our API & logistics experience, as well as create more self-service content lowering the barrier to entry for new users to take advantage of the offering,” explained Richard Suth. “We’re less than a month from having test environments ready to put in front of users. “We look forward to introducing the OneChronos ATS to US equities market structure.”

Assets under management at funds that integrate environmental, social and governance criteria have grown at 15.3% each year since 2016 and this is likely to continue.

The overall value of assets using ESG data has increased from $22.9 (€20.5) trillion in 2016 to more than $40 trillion this year according to a report, ESG Data Integration By Asset Managers: Targeting Alpha, Fiduciary Duty & Portfolio Risk Analysis, from consultancy Opimas.

Axel Pierron, Opimas

Axel Pierron, co-founder and managing director of Opimas and analyst Anne-Laure Foubert, authors of the report, wrote: “With ESG data integration becoming prevalent at asset managers, this growth trajectory is unlikely to slow any time soon.”

Growth is likely to be boosted as ESG indices have outperformed their parent indices during volatile markets caused by the COVID-19 pandemic. For example, the report said the Dow Jones Sustainability Index lost “only” 8.4% of its value from 3 March to 16 April this year, while the S&P Global BMI fell 12.4%.

“To meet this evolution of clients’ demand and focus, asset managers, even those operating non-ESG funds, are going through various ESG data integration projects,” said Opimas. “However, considering the nascent nature of the market and the complexity of integrating granular ESG data in investment allocation strategy, the vast majority of buy-side firms are still missing alpha-generation opportunities by not leveraging granular ESG data.”

Factset, the data provider said in a report that as investors adopt more sophisticated strategies, there has been more demand for raw ESG data that comes directly from a company or regulatory body and has not been aggregated or transformed by a vendor, especially as many investors want to build custom ESG metrics in-house.

“In doing so, firms have the flexibility to adjust the weight placed on specific ESG factors in response to the evolving market, geopolitical, and societal context,” said Factset. “The agility offered by in-house ESG analysis is often hard to replicate with vendor-provided top-level scores.”

Other firms are layering more granular information for specific ESG issues on top of vendor-provided ESG scores.

“The demand we have seen thus far has been for vendors that collect this data and deliver it in standardized formats so that firms can avoid collecting the underlying data themselves,” added Factset. “The key advantage of these datasets is the depth of detail and transparency they provide, allowing for customization in the application and ability to tweak aggregation methodology in alignment with investors’ values.”

Staff

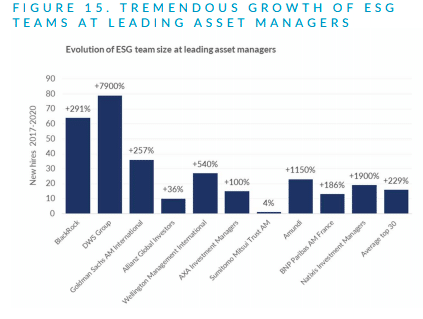

Opimas continued that asset management is gearing up for increased adoption of ESG data within investment strategies through recruitment.

“At the top 30 global asset managers, ESG teams have grown on average by close to 230% between 2017 and 2020,” said the report.

Growth of buy-side ESG teams. Source: Opimas.

In addition, stewardship teams have grown by 67% on average over the same time period.

The increase in engagement is shown by 71 ESG-related proxy proposals being brought to U.S. company meetings in the first half of this year according to FactSet.

“This accounts for 74% of all proxy proposals brought to company meetings in this period and a 6% increase in ESG proxy proposals from the first two quarters of 2019, despite the market downturn,” added Factset. “While this is promising, it likely does not offer a full picture of ongoing shareholder engagement as many investors opt for private discussions with company leadership.”

Passive

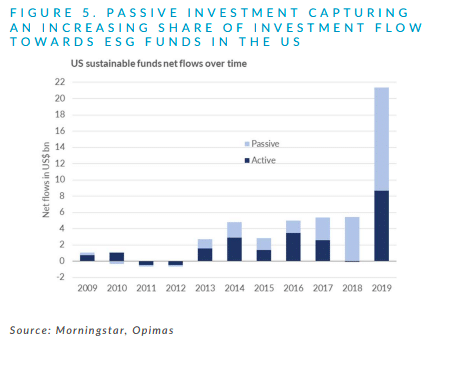

ESG strategies have mainly been used in active strategies, but passive funds are growing in the space.

Opimas said: “The situation is particularly pronounced in the US, where net flows into passive ESG funds have exceeded those into active ones since 2017.”

Last year US ESG passive funds had nearly 60% of the ESG-focused investment net flows according to the consultancy.

ESG fund flows. Source: Opimas.

The growth in passive is shown by assets invested globally in ESG exchange-traded funds reaching a record at the end of May according to ETFGI, an independent research and consultancy firm covering trends in the global ETFs/ETPs ecosystem.

@etfgi reports assets invested in Environmental, Social, and Governance (ESG) #ETFs and #ETPs listed globally reached a new record of US$82 billion at the end of May 2020

Highlights

· Assets invested in ESG ETFs and ETPs listed globally reached a new record of $82 Bn.

Year-to-date net inflows to the end of May were $28.5bn, compared to $7.2bn at the same time last year.

Another passive growth indicator is that Deutsche Borse’s Qontigo has just launched two new families of Climate Indices: the STOXX Paris-Aligned Benchmark Indices and the STOXX Climate Transition Benchmark Indices.

📢 Proud to launch two new families of Climate Indices: #STOXX Paris-Aligned Benchmark (PAB) and #STOXX Climate Transition Benchmark (CTB)! Learn more: https://t.co/3RoB3wWh3V

The climate transition benchmarks are specifically targeted towards decarbonization while the Paris benchmarks have stricter requirements around energy efficiency that coincide with the long-term global warming target of the Paris Climate Agreement. The indices were constructed in collaboration with ISS ESG and Sustainalytics, two providers of sustainability data.

Marija Kramer, head of ISS ESG, the responsible investment arm of Institutional Shareholder Services, said in a statement: “These important new offerings will significantly aid institutional investors seeking to provide beneficiaries greater choice when it comes to climate-conscious portfolios.”

More than half of financial services companies plan to accelerate their move to next generation technology to help navigate the Covid-19 fallout, according to a new global survey from global technology firm Broadridge Financial Solutions.

Canvassing 500 financial services C-Suite executives and their direct reports, the report showed that almost all financial services companies expect the pandemic to affect operating models and strategy toward next-generation technology.

In the next six months, 63% anticipate sharpening their focus on their cybersecurity and risk management while 60% will be looking more intently at enhancing multi-channel client communications.

In addition, 53% want to leverage the new tools to improve customer engagement and experience while 45% are seeking to significantly cut costs.

“Financial services players have shown they can adapt and change during the pandemic,” said Tim Gokey, CEO of Broadridge. “Going forward, they will continue to drive digitisation and mutualisation to improve client experience, resiliency, and cost. Prior investments in digital, cloud, and mutualised technologies have enabled companies to be more resilient during the crisis, and executives are taking careful note as they plan for the future.”

It is not surprising that the current environment is forcing many financial institutions to re-prioritise their investment strategies. The success of interactive digital technologies in managing the pandemic explains why 58% expect to increase their investment in this space while 54% are set to do the same in artificial intelligence (AI). In addition, nearly half intend to enhance their data gathering and analytical skills.

The pandemic has also changed the role of fintech service providers, with 70% of respondents stating that their ability to offer innovative uses of next-generation technology is now more important while around half believe it has been a driver behind the growing shift to mutualise – share or outsource – processing functions to reduce costs and increase resiliency.

These trends were supported more by commercial and investment banks as well as broker-dealers at 54% and 49% respectively, than their buyside counterparts which polled at 42%.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.