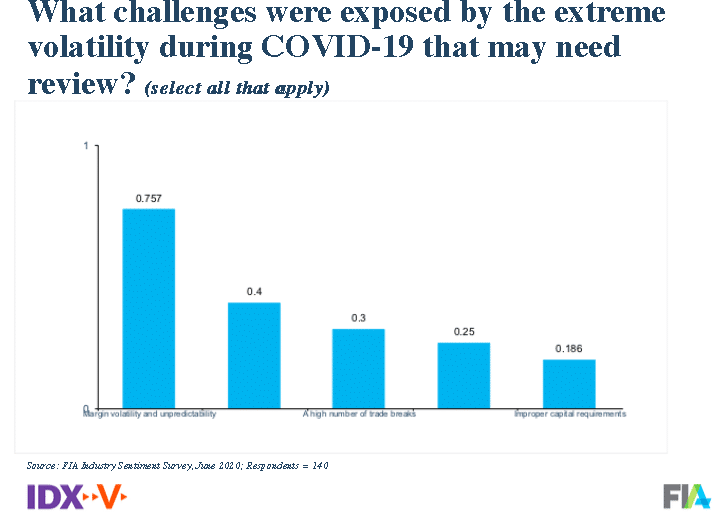

Margin volatility and unpredictability was the biggest challenge from the increased volatility caused by the Covid-19 pandemic according to a survey of derivatives market participants.

More than 75% of respondents to a poll at the virtual IDX conference yesterday cited margin volatility and unpredictability as their biggest concern.

Source: IDX Poll.

Hester Serafini, president of ICE Clear Europe, said on a panel at the virtual conference yesterday that the majority of the increase was from variation margin as positions were marked to market.

Hester Serafini, ICE Clear

For example, on Monday March 9, when the oil price dropped, ICE Clear Europe called $10bn in variation margin, compared to $2bn in initial margin.

Serafini said: “We are very supportive of having a volatility floor and higher margins in peacetime but that would need to be applied consistently across all regimes to avoid arbitrage.”

She continued that users can run stress tests which will give a good indication of likely margin calls.

However, she also said central counterparty clearers need to maintain some flexibility to prevent defaults. “Margin calls cannot be totally formulaic,” added Serafini.

Daniel Maguire, chief executive of LCH Group and group director, post trade division at London Stock Exchange Group, said on the panel that the UK CCP saw small increases in margin on a daily basis as volatility increased.

“Margins increased in incremental daily steps to between 18% to 19% but half of that increase was also due to new business,” he said. “Different asset classes also behaved differently so we need more precision in the analysis.”

Maguire said LCH calls margin three times a day, which is different from other CCPs, because it clears asset classes globally in multiple currencies and netting portfolios decreases risk.

“There was no change in our behaviour and it is good not to change during a crisis,” he added. “The aggregate size of the calls was also less than 10% of the initial margin being held.”

Jan Bart de Boer, chief commercial officer at ABN Amro Clearing Bank, said there will be a discussion this year between CCPs and their clearing members on margins when he was interviewed at the Eurex Digital Derivatives Forum this month.

de Boer continued there has been a slow-burning discussion between market participants and CCPs on the distribution of risk and reward which has become more urgent since Covid-19.

“Margins increased over a very short time so maybe they are too low in normal markets ?” he added. “The performance of CCPs has been stellar but clearing members have lost a year of income.”

Bank of England research

The Bank of England said in a research report that daily variation margin calls by UK CCP in derivatives markets in March were around five times the average daily margin calls for January and February. Variation margin calls also increased for uncleared derivatives.

Recent market turbulence highlighted the importance of margin as a safeguard against counterparty credit risk. Prudent margining is not a trade-off with liquidity risk, and liquidity strategies should account for potential margin calls. https://t.co/aUS76b4qFG#BankOvergroundpic.twitter.com/Zqn7CNosTK

The UK central bank said margin helped to ensure derivatives markets remained resilient throughout the recent market shock but also resulted in a large movement of liquidity around the financial system.

“This contributed to a ‘dash for cash’ in March 2020, as some market participants appeared to have insufficient buffers of cash-like assets to meet actual or anticipated margin calls,” said the study.

The report said prudent margining is an important part of risk management in the system and is not a trade-off with liquidity risk.

“Participants in derivatives markets should ensure their liquidity management strategies take account of the possibility that margin calls and requirements may rise significantly during periods of market turbulence,” added the Bank of England.

The Singapore Stock Exchange (SGX) acquired the remaining 80% stake in BidFX, a provider of electronic forex trading solutions for $128m as part of its strategy to expand into the global FX over the counter (OTC) market.

BidFX is a cloud-based FX trading platform for institutional investors. It was previously a subsidiary of TradingScreen, which had been incubating BidFX and spun it off in 2017. Since then, average daily volumes have grown at a compounded annual growth rate (CAGR) of 57 % to $31 bn as of May 2020. It has over 100 of the world’s largest banks, hedge funds and asset managers currently connected to its platform.

Loh Boon Chye, Chief Executive Officer of SGX

SGX, which is the largest foreign exchange (forex) derivatives exchange in Asia, first acquired a 20% holding last March for $25m with the intention to combine FX futures with OTC markets.

The main drivers to buy the rest of the company are the synergies between the two groups as well as the opportunity to support international FX participants from pre-trade data and analytics, trade execution to post-trade clearing, according to the exchange.

The exchange has continued to grow its FX futures franchise since it was launched seven years ago and has generated $3.8 trn in traded volumes. It recently introduced FlexC FX Futures which allows market participants to trade customisable FX futures as OTC and clear transactions on the exchange.

The acquisition comes at a time when the SGX along with the Monetary Authority of Singapore (MAS) have been actively bolstering the city-state to become the FX hub of Asia.

Loh Boon Chye, Chief Executive Officer of SGX, said in the statement: “The future of FX lies in the ability for market participants to benefit from price discovery, liquidity and transparency for both OTC and listed futures trading, in a single unified venue. BidFX is ahead of the curve in developing sophisticated electronic FX trading and workflow solutions.

He adds, “With BidFX as part of the SGX Group, we can now serve a wider FX community with more comprehensive solutions and enhanced distribution capabilities, while bringing together the two growing and mutually-reinforcing pools of liquidity.”

The European Council and the European Parliament have reached a deal on a common set of rules for central counterparties (CCPs) and their authorities to prepare for and deal with financial challenges.

The proposed rules aim at providing national authorities with resources to manage crises and to handle situations involving failures of key financial market infrastructures in a cohesive and coordinated manner.

The main objectives of the reform include reducing the probability of CCP failure by introducing effective incentives for proper risk management. This would enable CCPs to preserve their critical functions, to maintain financial stability, and to prevent taxpayers from bearing the costs associated with their restructuring or resolution.

The European Council said while they have built on the same principles as the recovery and resolution framework applying to banks, they have considered the specific global and systemic nature of CCPs.

The current COVID-19 pandemic was also taken into account with the co-legislators agreeing to give one additional year for trading venues and CCPs offering trading and clearing of exchange-traded derivatives to start applying open access rules under MiFID II.

Zdravko Maric, Deputy Prime Minister and Minister of finance of Croatia, said, “The current context, characterised by important volatility and uncertainty, reminds us of the vital function clearing houses play to make our financial markets safer. By putting EU rules in place to deal with their potential failure, we are adding an essential piece of legislation to secure confidence in our financial system.”

The European Association of CCP Clearing Houses (EACH) said it welcomes the political agreement. It stated, “an EU framework for CCP Recovery and Resolution plays an important role in ensuring an ex-ante definition of an efficient cooperation and coordination between authorities to address situations that would highly likely be cross-border per nature.”

It added that it was “particularly pleased that the political agreement achieves a balanced incentive structure that ensures the robustness of the clearing ecosystem, thus limiting the potential impact on taxpayers. The text provides a clear and certain path for Authorities and stakeholders in the unlikely scenario of CCP Recovery and Resolution.”

European Women in Finance: Taking on the tech mantle

Shanny Basar speaks to the new CEO of Finantix, Christine Ciriani about her many firsts in the tech and financial world…

This month Christine Ciriani became chief executive of Finantix, a technology provider to the wealth management, insurance and banking industries. Only 6% of CEOs in major financial services firms globally are women according to consultancy Oliver Wyman but Ciriani is used to leading the way. She was the first female student president at Claremont McKenna College and one of the few female partners at Capco, the management consultancy.

Ciriani took on the role of CEO at Finantix alongside her existing position as chief commercial officer, which she started in October last year.

She said: “Finantix is obsessed with data and using technology to help banks better engage with clients, understand customer behaviour and increase productivity. We help make relationship management more intelligent and scalable.”

The company recently opened a Serbia based office which has extended its reach to 11 offices around the continent. The aim is to not only develop and maintain support for the growing business but also to expand its group of industry experts.

When she was chief commercial officer, Ciriani played a key role in Finantix’s purchase of InCube Group in March this year. The Zurich-based fintech has artificial intelligence specialists, quant and software engineers and finance experts that provide data-driven, AI-enabled products to wealth management and insurance companies.

Ciriani explained that the acquisition of InCube allows Finantix to help portfolio managers identify the right investment opportunities for the right clients, and automate the chief investment officer process.

“We can provide relevant financial recommendations like Netflix does for movies and Amazon does for books,” she added.

In May Finantix launched CIO Cockpit, the first product that combined the capabilities from InCube. Chief investment officers can distribute personalised market updates and investment ideas to clients more quickly, using digital and collaboration channels.

Dr. Boris Rankov, co-founder and head of product at InCube, said in a statement: “Imagine an investment committee meeting where the members want to see the impact of the recent market turmoil due to Covid-19 on the bank’s model portfolios. Our CIO Cockpit offers exactly this.”

Last month Finantix also launched the latest version of its Digital Collaboration Hub.

Ciriani said: “Our Digital Collaboration Hub allows high net worth clients to have a concierge-type service with rich information in a compliant and auditable environment. For example, proposals that used to be sent via pdf are now digital and executable.”

During her time as chief commercial officer, Ciriani also opened new Finantix offices in Switzerland, Japan and Australia, where she said the firm is growing.

“There is a lot of interest in the US and we are looking at partnerships,” Ciriani added. “Our expansion in Asia shows the flexibility of our offering which has been tested globally, especially as the region has been quicker to move to digital.”

Ciriani had originally joined the Finantix board as a non-executive director in February last year because she is an industry partner at Motive Partners, the venture capital firm specialising in financial technology, which had made an investment. She is also on the board of directors of Barclays Private Bank Switzerland.

Venture capital has historically given far less money to female entrepreneurs and founders but Ciriani said Motive Partners is very diverse and different backgrounds are critical when discussing company valuations.

“Another Motive investment, LMRKTS, has a female CEO, Hilary Park, and Tegra118 is led by Cheryl Nash,” she added.

Career development

Ciriani has been successful in two fields, finance and technology, where senior women have been rare.

“Fintech reminds me of banking in the 1980s in terms of the number of women. It is encouraging to see an increasing number of women,” she said. “At Finantix, we have 34% women and an international team with more than 20 nationalities, which is not an accident.”

Ciriani is American but has also lived in Singapore and is now in Switzerland. She holds a degree in Economics and Accounting from Claremont McKenna College, and joined J.P. Morgan after graduation.

“I was the first female student president at Claremont McKenna College which at the time was 30% women,” she added. “I was a careers counsellor at university and wanted to join J.P Morgan because of the high calibre of individuals and because the firm was very international.”

She explained that she moved through departments at the bank, which was unusual, and gave her a good understanding of many businesses, including private banking. After four years at J.P. Morgan she left to study an MBA at the Haas School of Business at UC Berkeley.

“After my MBA I wanted to combine entrepreneurship and was employee number 20 at a consultancy, m.a.partners,” said Ciriani. “I helped grow the firm to 150 employees, and opened offices in Amsterdam and Geneva, before we sold the firm to Detica.”

She subsequently joined Capco where she was one of the few female partners.

“I was Capco’s first employee in Switzerland and grew the wealth management business across 10 countries including opening offices in Geneva, Zurich and Singapore,” she said.

Her advice to women is to be yourself.

Ciriani said: “For example, when I started in banking I was told not to wear trouser suits by female colleagues and not to put pictures of my children in my office. I have learnt to be more comfortable with myself and to speak my mind.”

She also said she has been fortunate to have both male and female role models who taught her to be herself and play on her individual strengths.

Ciriani added that it is also important to identify role models who support a way of living that can combine both family and professional commitments. She had her oldest son, who is now 14, when she first started at m.a.partners in Geneva, and her youngest son, who is now 12, when she started at Capco.

She said: “When I was doing my MBA at Berkeley, I remember advice from successful entrepreneurs telling us that we should not try to do it all and the importance of a good network and support system.”

In this week’s discussions Dan Barnes and John D’Antona focus on potential changes at the SEC and how the resurgence of retail trading has added liquidity and volatility to the markets.

The UK has halted compliance with the settlement regime of the European Central Securities Depository (CSDR) rules, which traders had fought hard against, due to its punitive policy for failed trades.

Rishi Sunak, the United Kingdom’s Chancellor of the Exchequer, has set out the first steps the UK will take that will differ from European regulation, new regulatory framework. In a statement he said, “Leaving the EU means the UK has taken back control of the rules governing our world-leading financial services sector.”

While there are regulatory reforms currently in progress any EU legislation that does not come into force before the end of the Transition Period in December 2020, is not obligatory for the UK to comply with. Her Majesty’s (HM) Treasury has considered how to take forward this legislation in the way that is to the benefit of the UK sector, while maintaining high regulatory standards.

As a result the UK will not be implementing the EU’s new settlement discipline regime, set out in the Central Securities Depositories Regulation (CSDR), which is due to apply in February 2021. These rules required firms to pay affine for failed trades and mandated an obligatory ‘buy-in’ which market makers said could prevent them from trading in assets that were hard to acquire. This was noted as being particularly difficult for fixed income markets.

“Any future legislative changes will be developed through dialogue with the financial services industry, and sufficient time will be provided to prepare for the implementation of any new future regime,” he said.

Additionally, the UK will not be taking action to incorporate into UK law the reporting obligation of the EU’s Securities Financing Transactions Regulation for non-financial counterparties (NFCs), which is due to apply in the EU from January 2021.

“Given that systemically important NFC trading activity will be captured sufficiently through the other reporting obligations that are due to apply to financial counterparties, it is appropriate for the UK not to impose this further obligation on UK firms,” said Sunak.

HM Treasury will set out further detail on upcoming legislation in due course, which will include:

• Amendments to the Benchmarks Regulation to ensure continued market access to third country benchmarks until end-2025. HM Treasury will publish a policy statement in July 2020;

• Amendments to the Market Abuse Regulation to confirm and clarify that both issuers and those acting on their behalf must maintain their own insider lists and to change the timeline issuers have to comply with when disclosing certain transaction undertaken by their senior managers (‘Persons Discharging Managerial Responsibilities’);

• Legislation to improve the functioning of the PRIIPs regime in the UK and address potential risks of consumer harm in response to industry and regulator feedback. HMT will publish a policy statement July 2020; and

• Legislation to complete the implementation of the European Market Infrastructure Regulation (REFIT) to improve trade repository data and ensure that smaller firms are able to access clearing on fair and reasonable terms.

The Treasury has also published a ministerial statement relating to LIBOR transition. The statement sets out detail on the Government’s approach to legislative steps that could help deal with ‘tough legacy’ contracts that cannot transition from LIBOR before end-2021. In particular the Government will use the Financial Services Bill to introduce amendments to the Benchmarks Regulation 2016/1011 as amended by the Benchmarks (Amendment) (EU Exit) Regulations 2018 (the ‘UK BMR’), to ensure that FCA powers are sufficient to manage an orderly transition from LIBOR.

Drew Miyawaki, Head of Global Equity Trading at Legal & General Investment Management America, Irina Sonich-Bright, Head of Product Management and EMEA Market Structure at Credit Suisse, and Adam Steinhaus, Global Head of Sales & Relationship Management at FactSet, discuss the ‘new normal’ of institutional trading desks operating on a decentralized and remote basis amid COVID-19.

The podcast is moderated by GlobalTrading Editor Terry Flanagan.

By Drew Miyawaki, Head of Global Equity Trading, Legal & General Investment Management America

Drew Miyawaki, LGIMA

The trading desk: a term in our industry where an object is used to describe many different things at once within an investment management organization. Literally (another oft-misused term these days), the trading desk refers to the furniture – a collection of desks, monitor displays, cables and telephones–- and in most firms, a random assortment of sports equipment, toys and games strewn among a smorgasbord of snacks. Figuratively, though, the trading desk represents a collection of characters responsible for the implementation of the firm’s strategies, where investment ideas become reality with each execution. The trading desk is a team, a source of information and activity where profits and losses are realized and conversation occurs at all levels of volume where no topic seems off limits. The trading desk in many ways is a monitor on the pulse of a firm’s activity level; it is not difficult to deduce when traders are busy or when they have idle time on their hands. Obviously, the trading desk is far more than the furniture, the hardware and even the software and systems. Ultimately, the trading desk is about the people, the ideas, the energy, and these vital aspects can flourish, regardless of their location.

Throughout my entire 20+ year career I have operated under the belief that there was a correlation between physical proximity to the desk and optimal trading outcomes: as one moved further away from the desk, their effectiveness as a trader declined. As technology proliferated through our industry, the focus of trading became functionality and connectivity – the closer to the source of the information, the better the advantage. Terms like co-location and direct access became measuring sticks for prominence, productivity, and ultimately profit. Whilst other areas of the organization embraced remote working conditions, traders stayed put, firmly based within the office walls. The conventional thinking was that traders needed to be together, to be able to see and hear each other constantly. Unencumbered physical access to portfolio managers was preferable, but first priority was trader proximity. Information was shared and indirectly absorbed by being together at the trading desk. The term ‘Work From Home’ became part of the industry’s lexicon but the phrase ‘Trade From Home’ was never taken seriously, I for one being a staunch opponent.

Practically, supporting Trade From Home was a technology problem. The concerns were not of short supply: reliance on non-uniform personal hardware, unreliable residential internet connections, lack of power redundancy, an insufficient number of monitors and phone systems, and the risk that an action taken during the trading process went unrecorded were all legitimate obstacles. Personally, there was a collective reluctance to be away from the information hub as well as an ego component: traders are generally allowed to jump the queue when it comes to internal corporate IT resources and support to make sure their systems function before all others.

(Click here to listen to a GlobalTrading podcast about trading from home.)

The global reaction to the COVID-19 quarantine situation changed the way we look at many aspects of personal and professional life. When it was clear that traditional business continuity plans and disaster recovery contingencies were not going to be suitable for a pandemic-induced shelter-in-place, suddenly Trade From Home needed to be taken seriously.

Legal & General Investment Management America (LGIMA) was an early adopter of Trade From Home. Within days in early March, LGIMA provisioned new laptops, monitors and docking stations and delivered them to trader residences globally. In some cases,we upgraded residential modems and routers and installed hard line internet connections to home office space to reduce reliance on strained family Wi-Fi bandwidth being shared by eLearning offspring. Virtual phones were downloaded to trader profiles and traditional morning meetings were replaced with video conferencing. Communication has evolved from shouting over desks to collective chat rooms, conference calls and group messaging – all of which is recorded both for compliance and for reference.

LGIMA is in week 17 of Trade from Home as of June 22, and we have managed to mitigate the challenges that the new process has presented along with the volatility and confusion the markets have offered. The end of March saw an intense index rebalance followed by an extreme quarter-end valuation, resulting in two of the busiest equity trading days in our history, all handled by a global trading team working remotely. Additionally, we have found ancillary effects have created a more efficient work environment: new virtual meetings have become quicker; a previous reliance on lengthy email conversations have been replaced with real-time document sharing and editing, and a general openness among colleagues to consider more innovative, alternative methods of work streams and engaging with others. Historically, traders have been compelled to congregate within an office regardless of conditions. Power outages, terrorist attacks, elections, sovereign referendums, polar vortexes and hurricanes have all presented hurdles in getting trading personnel physically together to ensure business remains uninterrupted. Disaster recovery and business continuity plans are built and funded around a specific location for key staff. The uninhibited vocal sharing of information is difficult to replicate remotely. Training new or younger traders is difficult to perform virtually. The support, banter and camaraderie that are built through the trading desk’s entertaining wagers, contests and games are some of the important things lost from this new reality that we are all adjusting to.

Times have changed and will continue to be fluid as we navigate through this situation. Countries,cities and businesses will vary their responses to relocating personnel back into office spaces and we will have to try to solve for new scenarios where some coworkers are located in the office whilst others remain at home. Longer term, this situation has shown that Trade From Home can add sustainable flexibilities to allow not only for catastrophic contingencies but also improved work-life balances without disruption to productivity or performance.

This recent situation has opened our eyes to new possibilities along with some challenges. Trading in a COVID-19 environment has effectively stress-tested the Trade From Home concept that will help move our industry forward. In a business of measuring risk and reward, Trade From Home is clearly an investment worth executing as a long-term position.

By Eric Boess, Global Head of Trading, Allianz Global Investors

Eric Boess, Allianz

Over the last year the hype around the use of technology in asset management has grown exponentially. Clearly the use of data and modern analytics based on artificial intelligence or machine learning are here to stay and will transform the way asset managers design their decision and implementation processes, but as are other parts of the value chain like client servicing, Know Your Customer and collateral management, just to name some.

With regard to execution, trading technology has become an incremental part of the daily routine: almost 100% of orders, irrespective of asset class, are routed electronically to brokers and platforms, and telephone conversations have moved to chats. The price discovery process increasingly refers to wider data sets from related assets or even other asset classes, and as a result productivity gains allowed trading teams to keep their headcount while assets grew.

This wave of technology evolution is comparable to the ‘rise of the spreadsheet’ that swept through fund management in the 1990s. Back then long, printed lists of holdings and trades retrieved from a mainframe computer were replaced with more nimble, small spreadsheets and simple but flexible database solutions. Those opened the door to much faster analytics and visualisation, and for many years Excel became the Swiss army knife of our industry.

Déjà Vu

Trading in 2020 shows a similar pattern: sheets being replaced by small, and once again more flexible R and Python code. Scattered data sources are aggregated and made accessible. Standardised business intelligence software and libraries ease analytical processes. For fellow traders in the same age cohort as the author of this text, a feeling of déjà vu creeps in. Knowing spreadsheets and basic database tools was an edge and became almost a basic requirement in the 90s, and the same holds true for what forms the new fertile ground of IT infrastructure now: basic coding, data handling and manipulation and analytics.

Put more bluntly: would we still hire a trader without those tech skills? Absolutely, but it would be the exception to the norm now. Like in pop culture, the geeks and quants are the new mainstream, not the fringe minority they sometimes were perceived as thirty years ago.

This evolution did not start yesterday, and it is in full swing now. Most trading desks have reached a high level of technology penetration. Algorithmic trade execution is commoditized in equity and parts of derivatives trading and quickly making inroads into

FX. Automated execution is a large part of fixed income trading today, moving from government bonds into credit. The technology applied is usually standardised, using FIX as a backbone and various household names of order management systems in combination with add-on analytics which can be bought or built. It is this latter part in which asset managers can differentiate their alpha generation capabilities: how can you seamlessly implement a unique investment process into efficient execution, preferably with real-time feedback loops between pre-trade cost analytics and investment decisions?

But much of this has already been done by market-leading firms, and while portfolio managers still have a lot of potential insights hidden in non-public, non-structured and other alternative data sources, low-hanging fruit in trade execution seem to be rather scarce now.

There are obviously differences between asset classes, some of which are driven by history, the regulation of marketplaces and the ecosystem of actors in the market.

Equities have been trading via electronic channels for decades, while fixed income markets have only been pushed there by regulation like MiFID II in the recent years. As a result, the use of technology in the asset classes has evolved along very different paths. Equity traders apply lots of statistics on a large amount of tick data available, aggregating price information which is fragmented across exchanges, MTFs, dark pools and other venues.

Bond traders on the other hand do not have that amount of data per instrument, very limited numbers of price points and literally no exchange data, nor a consolidated tape for aggregated price information. As a result the focus of technology in fixed income is more about automating manual execution and a better pre-trade price discovery process, using other assets and correlated instruments.

Siloed ‘Know-How’

The technology applied in each of those asset class silos is fairly advanced, but in many cases the know-how is stuck in silos as well. Sometimes overlooked is the fact that applying technology is to some part a creative process, similar to what the arts and craft movement of the late Victorian age concluded. So breaking down know- how silos to allow for ‘cross fertilisation’ is something we work on at Allianz Global Investors. This includes meetings between different trading teams in which the

use of algorithms, price discovery protocols or workflow enhancements are shared, contrasted and in some cases ported to other teams. The key point is that once a firm has good technology in each asset class, the role of lateral know-how and the possibility to share ideas between teams which in some cases barely speak the same (trading) language becomes critical. ‘Translating’ between bonds, equities, currencies, commodities and derivatives is a difficult task, but vital to get the best out of a modern multi-asset trading team.

Depending on the setup of the trading team, this ‘translation’ needs to take place between IT and Trading: not all Execution desks have the resources to do most of their coding themselves and maintain tools and data, and north of a certain threshold simple governance requires more IT involvement.

Another area where cross-asset requirements become an important success factor is the increased use of industry standards like FIX and open source code.

When I started writing this article I had a piece about technology in mind, like the headline suggests, but in the process it morphed into something about what the real challenge in trading (and frankly the entire asset management industry) actually is: marrying people, technology and process in one firm into something that follows Paul Tudor Jones words of wisdom: “No man is better than a machine, and no machine is better than a man with a machine.”

Ultimately financial markets are very much driven by human psychology (yes, the ‘greed and fear’ model applies), and I personally doubt software will be able to holistically handle them on their own for now. But machines clearly will dominate spaces where large quantities of data are available, speed is of essence and patterns are not too volatile. I leave it to the reader to conclude if trading falls in this category.

When she was a young girl Lynn Martin did not think that a woman could make a career on Wall Street but she has defied her own expectations. In July 2015 she became president and chief operating officer of ICE Data Services.

Her responsibilities cover managing global data operations including exchange data, pricing and analytics, reference data, desktops and connectivity services across all major asset classes.

Lynn Martin, ICE

Martin told Markets Media: “The biggest change in five years has been the type of data produced and how it is used in markets. For example, developments in artificial intelligence and machine learning and more recently, environmental, social and governance data to power alpha generation.”

She continued that in 2015 ICE Data Services focused on connectivity and delivery linked to the exchange business.

“Now we are continuing to provide transparency into less liquid markets, such as fixed income, and expand the customer base we target to front, middle and back office users by providing real-time data and other high quality content,” Martin added.

The exchange has invested in APIs and the distribution of content so delivery is not tied to a single workflow. “Data should be available as a feed that can easily integrate into whatever system a user chooses,” she said.

Remote working

Martin compared the shift in the data business model to changes in cable television where the focus has moved from distribution to content providers such as Netflix and Hulu. This flexibility proved critical when the industry was forced to work from home due to the Covid-19 pandemic.

She explained that as ICE runs systemically important market infrastructure, such as the New York Stock Exchange and clearing houses, the business continuity plan was very sound and actionable. In addition, ICE had already invested in tools such as video conferencing and enabling remote capabilities.

“It is ingrained throughout the firm to provide highly reliable business infrastructure to our customer base and as a result we did not miss a beat despite customer dislocation, the need for our own teams to work from home, record volatility, and fractured liquidity,” Martin added.

The rise in volatility in March meant there was a significant increase in demand for data and queries rose by more than 30% during this period.

“I look back with a sense of pride at how my team responded and held the hands of our clients through a challenging time,” said Martin.

Jeff Sprecher, ICE

Jeffrey Sprecher, chairman and chief executive of ICE, said at the Piper Sandler Global Exchange & Brokerage conference at the start of this month that New York Stock Exchange had more than 100 billion messages on March 16 this year, compared to the previous daily high of 35 billion messages.

Sprecher said: “We handled that seamlessly and with no latency, no particularly outlying latency. So, our whole system, our whole platform had to scale, and it did so really well, and outperformed many of our competitive peers. So that has helped improved our sales cycle.”

He added that being distribution agnostic was also an advantage.

“We have desktops, but one of the things that we saw our customers doing was trying to take data in different ways to get their employees set up the work from home or other locations,” he said. “We were very, very flexible so that helped our sales cycle. And our employees adapted really well.”

Sprecher continued that as as market participants try to make sense of the global macroeconomic backdrop there has been a fight to quality for Data Services businesses, particularly Pricing and Analytics. “Over the last few weeks, customers are increasingly, and in many cases, proactively engaging with us,” he added.

Growth prospects

ICE Data Services made up more than 20% of the company’s consolidated revenues when Martin took on her role, having grown from 11% in the previous five years.

In the first quarter of this year Data Services had revenues of $564m (€500m), which was the 41st consecutive quarter of year-over-year growth and just over a third of total group revenues of $1.6bn.

Our CFO Scott Hill on generating record revenues, record operating income, and double-digit earnings per share growth#ICEearningspic.twitter.com/LAs1Dc1OPM

Scott Hill, chief financial officer at ICE, said on the results call that record Data Services revenues were driven by growth in the Pricing and Reference Data business, as well as continued strong trends in fixed income indexes. Hill said: “We expect growth in Pricing and Analytics to be stable in the second quarter and accelerate through the balance of the year.”

Martin explained that ICE acquired the Bank of America Merrill Lynch global research index platform at the end of 2017 and that assets tracking the indices had more than doubled in the eighteen months that immediately followed that acquisition.

She said the next frontier is ESG data and to provide additional metrics that help make investment decisions.

“We launched ICE Climate Risk to provide actionable analytics on the US municipal bond market for individual securities and increase transparency around the climate driven risks in this market,” Martin added. “Separately, we have partnered with Bank of America research to provide 500 ESG metrics on US and international companies so investors can make their own decisions on the values which matter most to them.”

https://t.co/F0bTz332Fb New tool for measuring climate risk in municipal bonds emerges from stealth.

ICE Data Services and risQ plan to launch the municipal climate package by the end of the first quarter of 2020. #ClimateChange#muniland

In January this year ICE announced a partnership with risQ, a US start-up providing climate risk analytics that uses climate science, catastrophe modelling and geospatial machine learning technology to increase transparency in the US municipal bond market. For example, two municipal bonds in Florida may be trading at the same price but ICE Climate Risk can show the risk of flooding for each security, and one may be much higher than the other.

In April this year Breckinridge Capital Advisors, an independent asset management specializing in investment grade fixed income portfolios, said it had selected ICE Climate Risk.

Breckinridge Capital Advisors selected ICE Climate Risk, Powered by risQ to provide data and analytics for the municipal bond market https://t.co/Q6hVRERlET

Michael Bonanno, vice president, analyst and municipal sustainability lead at Breckinridge Capital Advisors, said in a statement: “The level of granularity that risQ and ICE provides is of value and adds a new component to evaluating a security for potential risk, while also matching the requirements that we’re seeing from clients to include ESG as a factor in investments.”

There are also opportunities to grow in alternative data, and Martin said ICE looks to provide data that is complementary to its existing businesses.

“For example, ICE Connect Weather Data is tied to our commodities complex and our cryptocurrency data feed is the broadest in the market,” she added.

Sprecher said at the Piper Sandler Global Exchange & Brokerage conference that the data business will benefit from the network being created by ICE ETF Hub. The industry-wide, open architecture, primary market platform for exchange-traded funds was launched in October last year to create a more standardized process for ETF creation and redemption.

ICE ETF Hub processed more than $136bn in notional value in the first quarter of this year. Authorized Participants processed a record $87bn in notional value in March, up from $27bn in February, with the growth mainly coming from fixed income.

“BlackRock was our flagship launch partner there – the other big issuers are all working around us, talking to us, trying to figure out how to work it into their workflow,” Sprecher added. “And most interesting that you’ll see in our next earnings call, and commentary is the number of new market participants that have been moving to connect to that platform. We’re really building a network.”

He continued that ICE is positioning itself to be the reference data, index provider and analytic provider for the ETF market with the Bond Hub and ETF Hub providing some execution capability.

Career path

Martin said: “I fell in love with New York and Wall Street at a young age although I did not think then that a woman could make a career there.”

She holds a degree in Computer Science from Manhattan College and a master in Statistics from Columbia University, where she developed her deep interest in financial engineering.

Martin believes it is very important to educate girls in science, technology, engineering, and mathematics at a young age.

“External organisations such as Girls who Code have been doing a great job in teaching coding as a skill,’” she added.

Shoutout to @Fiserv for showing our Summer Immersion Program girls what their future could like—in finance and tech!

Thanks for always supporting our girls and our mission 💪 #PartnerOfTheDay

The ability to code was essential for Martin when she joined LIFFE in 2001 as the derivatives trading exchange was transitioning from floor to electronic trading.

“There were opportunities for women who could code and speak with a coder as machines tend to be an equalizer,” she added.

Martin rose to become chief executive of NYSE Liffe U.S and oversaw the introduction of several new fixed income and equity index futures.

“I have been fortunate to have had bosses who have taken a chance on me and given me opportunities even when I wasn’t the perfect fit for the job description,” she said.

She joined ICE when the group acquired NYSE Euronext in 2013 and oversaw the integration of its contracts onto ICE’s trading platform. She then became chief operating officer of ICE Clear U.S. until being promoted to her current role.

“My advice is to work hard, not to pretend to know the answer to everything and to voice an opinion when you feel strongly about a topic,” she added.

Martin also said women should not underestimate the diverse perspective they can bring to an organisation.

She added: “There has been progress in the number of women in financial services and in 5 to 10 years I am optimistic that we will have a much stronger mix of diversity.”

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.

")

_872x600")