David Braga, CEO, BNP Paribas Securities Services Australia & New Zealand, and Luc Renard, Head of Financial Intermediaries & Digital Transformation, Asia-Pacific for BNP Paribas Securities Services, discuss the evolution and the future of securities services with Markets Media Editor Terry Flanagan.

Ep. 1: Securities Services: Past, Present and Future

Ep. 2: DLT in Securities Services

Ep. 3: Evolving Business Models for Institutional Custodians

Northern Trust has implemented machine learning models within its FX currency management solutions business, to provide greater oversight of thoughts of daily data points. The solution, which has been developed in partnership with Lumint, an outsourced FX execution services provider, aims to help buyside firms reduce risk in the currency management lifecycle.

The technology utilised by the Robotic Oversight System (ROSY) for the US based custodian systematically scans newly arriving, anonymised data to identify anomalies across multi-dimensional data sets. It is built on machine learning models developed by Lumint using a cloud platform that allows for highly efficient data processing.

Andy Lemon, Northern Trust

Andy Lemon, head of currency management, Northern Trust, said, “In a data-intensive business, ROSY acts like an additional member of the team working around the clock to find and flag anomalies. The use of machine learning to detect data outliers enables us to provide increasingly robust and intuitive solutions to enhance our oversight and risk management, which can be particularly important in volatile markets.”

Northern Trust and Lumint formed a strategic partnership in 2018 to deliver currency management services with portfolio, share class and look–through hedging solutions alongside transparency and analytics tools for asset owners and asset managers.

Alex Dunegan, Lumint

“Northern Trust’s deployment of ROSY amplifies the scalability of its already highly automated currency hedging operation; especially for the more sophisticated products such as look-through hedging offered to its global clients,” added Alex Dunegan, CEO, Lumint.

The solution is the latest rollout of machine learning technology by Northern Trust, as the it continues to leverage new technologies across its businesses. In August last year, the custodian developed a new pricing engine within its securities lending business employing machine learning and advanced statistical technology forecast lending rates for 34 global markets.

Built on a hybrid-cloud platform, the algorithm leverages numerous strategic market data points from multiple asset classes and regions to project the demand for equities in the securities lending market.

Market surveillance has come into its own during the current pandemic. Trade alerts skyrocketed but there was also a huge number of “false positive” readings as volatility took hold of the markets. This underscored the need for surveillance technology to be more than fit for purpose especially in these unprecedented, turbulent times, according to Greenwich Associate’s report – Protecting Market Integrity During High-Risk Conditions.

According to the report, trade surveillance alert volumes soared by 874% during the month of March from January in some Americas-based sellside firms, and 636% and 675% across samples from Europe Middle East Africa and Asia Pacific, respectively. Market conditions in March alone broke normal routines and created abnormal trading patterns that, in many cases, were marked as red flags by surveillance and compliance systems.

Danielle Tierney, Greenwich Associates

Although markets have climbed up since, the Dow plummeted 23.2% in the first quarter, its lowest point since the fourth quarter of 1987 while the UK’s FTSE 100 shed 24.8% of its value in the first three months, its second-worst quarter since being created in 1984 – only beaten by Black Monday – the crash in the autumn of 1987.

“The combination of exploding volumes, spiking volatility and rapid transitions to working from home converged into a perfect storm,” says Danielle Tierney, senior advisor for market structure and technology practice at Greenwich Associates and author of the report. “For market surveillance and trade compliance infrastructures, these conditions quickly proved and are still proving to be the ultimate stress test.”

It is not surprising that firms that had proactively invested in surveillance technology were better placed to weather the storm. In fact, at the highest level, the key differentiators contributing to success in maintaining effective surveillance operations are the implementation of high-quality surveillance technology and adoption of a holistic approach to data source inputs, according to Tierney. Equally as important is ensuring the internal resources are robust and can efficiently handle these tools.

However, as the report points out, surveillance issues such as reducing false positives are not always high on the IT budgets even though they are often cited as main concerns. “Despite consistently surpassing 10% annual spending growth during the last decade, market surveillance solutions have been generally considered less critical components of financial market structure than areas such as trading and order execution systems,” says Tierney.

As a result, without the proper resources and investment, issues such as the number of false positives will “remains challenging for some firms, due largely to budgetary resource restrictions on both personnel and compliance spending.”

The rampant growth of data thanks to new technologies, more onerous regulatory reporting and increased electronic trading needs to be better balanced with a more effective data governance framework and centralised strategy, according to the FMSB’s (FICC Markets Standards Board) second Spotlight Review

The report, which examines the role of data management in the financial ecosystem, warns that the greater volumes and sophistication in the way data is handled, manipulated and acted on by financial markets participants has introduced “high degrees of complexity and inconsistency.” This not only increases the risks of market misconduct and market instability but could also lead to the improper access to, or use of, data.

Martin Pluves, CEO, FMSB,

Gareth Ramsay, Bank of England

The report acknowledges that different industry initiatives such as the Financial Information eXchange (FIX) Protocol and Legal Entity Identifiers (LEIs) have made progress in standardising data and mitigating problems. However more work is needed and to that end it explores eight key components to promote effective data governance, covering the data lifecycle, policies, taxonomy, source mapping, movement and lineage as well as data classification, leakage detection and quality.

The Spotlight Review also highlights the advantages of moving to a more centralised approach to enterprise data architecture, depending on a firm’s size, complexity and business models. For large firms, an alternative ‘hybrid’ approach may be preferable as full centralisation can be expensive and unnecessarily cumbersome.

Martin Pluves, CEO of FMSB, said, “Data drives today’s FICC markets. Ensuring confidence in data is vital to stability and resilience of the financial system. With exponential growth in the volume and sophistication of data, there are opportunities for increased transparency and improved overall efficiency of FICC markets. There are also great challenges and significant risks, explored in this paper. Given the growing importance of data there is an increasing interest in developing standards in this area and on strengthening data governance, areas FMSB and its diverse members are well placed to address.”

Gareth Ramsay, Executive Director of Data at the Bank of England, added, “The rapid pace of systems development and the increasing dependence of the financial system on data is a key strategic focus for the Bank. The key themes in the review, particularly the importance of data governance and standardisation, complement the Bank’s ongoing data collection review, which aims to make data collection more efficient for the Bank and for firms, and to improve our ability to use that data effectively.”

TransFICC, which speeds connectivity to fixed income and derivatives venues, plans to double in size following its latest fundraising as workflows became increasingly automated.

The London-based fintech allows firms to easily connect to trading venues using open source technology through its ‘One API for eTrading’ platform, streamlining technology requirements and reducing operational costs.

Steve Toland, TransFICC

Steve Toland, founder of TransFICC, told Markets Market: “We enable firms to stream prices on venues such as Tradeweb and Bloomberg in minutes. In a greenfield situation we can build a production environment to go live on these venues in a week.”

Toland continued that TransFICC currently builds connections to a core of between 35 to 50 venues, which typically provide 90% of a bank’s needs.

“But there is a long tail,” he added. “For example, a client has asked us to connect to Peruvian and Chilean government bond venues.”

Another client has asked TransFICC to connect to some credit trading venues, which is a very fragmented market. In March this year TransFICC partnered with SoftSolutions to provide connectivity and workflow solutions for interest rate swaps.

Banks are still operating and trading despite the current Covid-19 pandemic lockdown.

“Their thinking on how they run their systems has changed and the use of the cloud has been forced upon them,” said Toland. “That will not be going away in the long-term.”

Funding round

Last month TransFICC closed its £5.75m ($7.2m) funding round. ING Ventures and HSBC joined existing shareholders, Citi, Illuminate Financial, Main Incubator – the R&D unit of Commerzbank Group, and The FinLab.

Toland said the fundraising will be used to double the size of the team this year, to build connections to more venues and enable this to be done faster.

“The roadmap of new venues to connect with is not going to end any time soon,” Toland added. “This time next year we would expect to have double the number of clients, including clients from the buy side.”

Mark Whitcroft, Illuminate Financial

Mark Whitcroft, founding partner at Illuminate Financial, said in a statement: “With the backing of now six global financial institutions, as clients or investors, the team is successfully executing their vision to become the API layer in electronic trading. As an investor in enterprise technology for financial markets, the proposition aligned with our key theses on electronification of markets and cloud adoption.”

Before the latest fundraising TransFICC was part of the Citi Innovation Lab with Toland described as “transformational.”

“Having Citi involved in the design and testing of the product was a real benefit,” said Toland. “The feedback cycle was very fast, as we provided code on a daily basis and Citi had automated testing.”

Stuart Riley, global head of operations and technology for markets and securities services at Citi, said in a statement: “Providing the company with office space in our lab allowed Citi and TransFICC development teams to work side-by-side and co-create very rapidly, integrating development and testing processes to deliver and release value-add functionality on a daily basis. Our experience with TransFICC has paved the way for a new operating model for Citi with start-ups.”

Toland continued that TransFICC has an advantage with a different business model of providing the connectivity toolkit for clients to build trading components to their own requirements on an open basis. “It is a plug and play model,” he said.

Increased use of trading venues

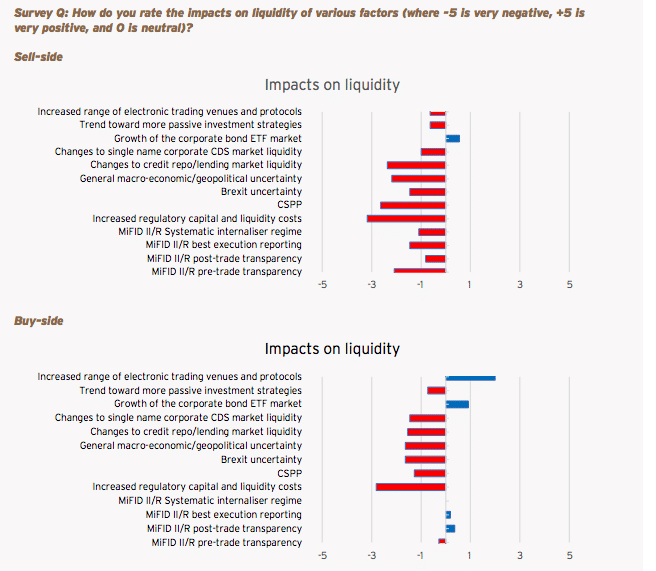

Market, and even security, selection by dealers is becoming more prominent, particularly among firms outside the global bulge bracket, according to the latest survey of Europe’s investment grade corporate bond market by the International Capital Market Association.

The survey found that the use of trading venues and e-trading protocols to execute trades has continued to increase over the past years.

Selective or multiple request for quote continue to dominate although there appears to be more interest in, and uptake of, alternative protocols to source liquidity according to the report.

Impact on liquidity. Source: ICMA.

“Direct connectivity (or “direct access trading”), whereby dealer banks stream axes or prices directly to their clients, appears to be gaining more interest among participants, which also supports more automated bilateral order execution, such as “click-to trade,” added ICMA.

When it comes to market data provision, there appears to be no better way to deliver the lifeblood of the markets than the Cloud. The Cloud is fundamentally reshaping the distribution, consumption, management and analysis of market data, which has become a bigger part of serving the markets than trading services. The convergence of big data, cloud capabilities and rise of mobile platforms has created the opportunity to meet investors or firms where they are. This means that all manner of financial firms, from small fintech firms and entrepreneurs to the larger, more traditional players, can be served seamlessly. This has pushed Cloud adoption to advance at a rapid pace.

According to recent data from Greenwich Associates, 93 percent of market data professionals plan to use the Cloud to manage their data needs. Of that 93 percent, more than half said there was a “very high” probability of usage while only one percent reported a “very low” chance.

Usage of the Cloud has obvious benefits. First, data is much more accessible wherever one is located. Secondly, the Cloud does not have the size limitation that a physical server or computer memory bank does – it is theoretically boundless – hence offering virtually unlimited capacity at a fraction of the cost. And as the demand for new and more esoteric information grows, a place to store it that is easily accessible becomes essential.

The Cloud fits the bill. Greenwich noted that one-third of buy-side trading desks’ technology budgets are spent on market data desktop application, compared to only 12% on direct data feeds. This is in part because the firms often have a heavy burden in setting up the hardware needed to take these feeds. The cloud does away with a lot of that baked-in spending.

In this vein, Nasdaq just announced the launch of its Nasdaq Cloud Data Service (NCDS), which provides clients access to real-time equity, index, and fund data through cloud-based technology. Nasdaq, a data and technology partner to a multitude of companies, sees moving to the cloud as a logical next step in evolving to meet client needs.

Lauren Dillard, Nasdaq

NCDS is accessible through a suite of highly scalable, cloud-based Application Programming Interfaces (APIs). These APIs utilize open-source delivery standards and a software development kit (SDK) to fast track engineering efforts. This eliminates the need for hardware procurement, proprietary protocols, file formats, and leased lines, and allows for effortless integration of data from disparate sources. This equates to a big reduction in time to market for customers. NCDS currently runs on the Amazon Web Services (AWS) Cloud but is cloud agnostic, capable of being used with any cloud provider.

“Taking market data from the cloud makes our customers faster and more agile. This increases the options we can offer clients, and we can get them online in hours or days instead of weeks or months,” explained Lauren Dillard, EVP and Head of Global Information Services, Nasdaq.

The NCDS offering was created to deliver lower latency and higher performance for entrepreneurs, fintech firms and traditional financial services applications. NCDS allows users to connect to a variety of data products in real time.

And just recently, MT Newswires announced its global, real-time multi-asset class capital market and economic news services are now available to clients via the Nasdaq Cloud Data Service API.

The last several years have seen a tremendous shift away from building new trading technology and systems in-house to outsourcing via specialty vendors. For example, Greenwich research shows that over 90% of buy side firms now look to a third party for their execution management system.

Spencer Mindlin, Aite Group

Fintech providers have spent over two decades simplifying customization, removing the burden of maintenance from their users and, more recently, deploying applications via the cloud eliminating the need for local installations and on-premises hardware. Movement away from in-house to outsourced cloud deployed applications further makes the Cloud-based market data an even better value proposition.

Spencer Mindlin, capital markets analyst at Aite Group, said data and technology services is an important part of Nasdaq’s business and their customers are increasingly moving to the cloud. So, it’s smart that Nasdaq is making its data as easily available as possible.

“The amount of data that financial services firms will need to collect, produce, analyze, and store will undoubtedly continue to increase exponentially. And the value propositions of the cloud are driving any almost all new applications, migrations, and deployments to it,” Mindlin said. “So, it only makes sense that the data will need to be available in the cloud as well.”

David Howson, president of Cboe Europe, said Periodic Auctions and Large In Scale volumes will continue to grow and the exchange is exploring offering new order types to further enhance liquidity.

Howson took on his current role at the start of this year from Mark Hemsley, who retired from the company. He had previously been chief operating officer of Cboe Europe since 2013.

David Howson, Cboe Europe

He told Markets Media that Cboe Europe expects continued growth in Periodic Auctions and LIS as existing clients are looking for ways to extend their interactions with these platforms and there is a healthy pipeline of new clients onboarding to use these services.

“We are exploring offering new order types to further enhance the liquidity on our market,” Howson added. “For block trades we are enhancing the workflow to increase matching.”

In addition Cboe Europe launched a closing cross mechanism, 3C, last year which he said is being used more actively. “We have seen good flow in Europe and there is a decent pipeline so we expect volume will continue to grow over the coming months,” he said.

3C is a post-close trading service for customers looking to execute across the 18 European markets that the exchange serves as increased volumes are being executed in the closing auction and post-close trading session in Europe. In addition, many exchanges charge higher fees during this period.

The mechanism is independent from the listing exchange and does not depend on their closing auction price. It uses an “at limit” order type, so orders can only be entered and matched at the participant’s specified price. Market participants are able to see the price and size/quantity for all levels predicted to execute in the cross in real-time.

The increase volatility as a result of the Covid-19 pandemic led to a rise in across all exchanges. Howson noted there have been no problems in trading or clearing despite all staff working from home on some of the exchange’s heaviest volume days.

“On February 28, overall market volumes reached over €100bn ($108bn), the largest volume day since the referendum on the UK leaving the European Union,” he added. “We have also seen volume records in our Periodic Auctions Book and Cboe LIS.”

Cboe reported in its results for the first quarter of this year that net revenue for European equities increased by 15% from a year ago to $26.2m.

The exchange said Cboe European equities had 17.7% market share in the first quarter of this year, down from 22.1% in the first quarter of 2019, which was primarily as a result of significant market profile shifts. Highly volatile market conditions during the quarter saw some participants recalibrate their models or retrench from the market.

“In the first half of March some funds managers were looking for actionable liquidity and recalibrating their models and volumes rose on the lit central limit order book,” said Howson. “Spreads widened about five to six times the average, but fell back to between two to three times average in early April.”

Launch of European equity derivatives exchange

Howson confirmed that the exchange is still planning to launch Cboe Europe Derivatives, a new exchange, in the first half of next year. “The Covid-19 pandemic may lead to some short-term bumps in the road, but it does not alter our long-term plan or strategy,” he added.

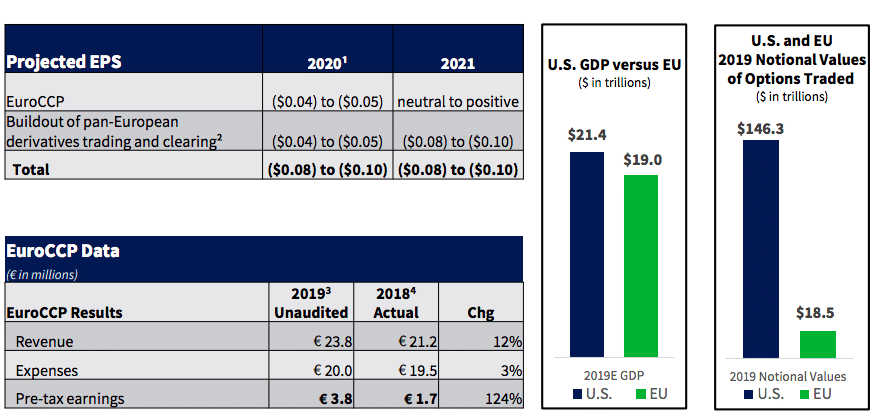

Pending acquisition of EuroCCP. Source: Cboe.

In order to launch the new exchange, Cboe announced the acquisition of EuroCCP, the pan-European equities clearing house in December last year. EuroCCP clears trades for 39 trading venues, which represent close to 95% of Europe’s equity landscape.

Ed Tilly, Cboe Global Markets

Ed Tilly, president and chief executive of Cboe Global Markets, said on the first quarter results call that the exchange will look to provide an alternative market model and introduce efficiencies available in the US market .

He continued that Cboe expects to offer exposure that represents multiple European markets through index futures and options, single-name futures and options and other products.

MiFID II review

Last month the European Securities and Markets Authority published responses on its review of certain aspects of MiFID II as the regulator had wanted to the EU regulation to increase trading on lit venues in the region, which has not happened.

📢ESMA has published responses to the consultation on MiFID II MiFIR review – equity transparency, DVC and trading obligation.

— ESMA – EU Securities Markets Regulator 🇪🇺 (@ESMAComms) April 23, 2020

Howson said: “Buy-side participants find utility in access to a range of execution mechanisms so they can optimise performance for their strategies. If the number of execution mechanisms is constrained through an artificial quota they cannot meet their best execution requirements.”

In their responses fund managers also argued that systematic internalisers, dark venues and periodic auctions have saved money for end-investors and there are other ways to increase transparency, such as introducing a consolidated tape. The sell side responses also said that forcing trades onto lit venues will harm best execution and want the share trading obligation and double volume caps removed from MiFID II.

Howson wrote a letter to clients on the consultation and the exchange’s response. He said: “Many of the areas consulted on need careful consideration in order to avoid causing damage to European equity market structure and we have provided a robust response.”

The response said there is no fundamental issue with the balance of trading between available trading mechanisms.

“This becomes apparent when activity that is technical in nature and therefore not appropriate for execution on a multilateral venue is removed from the picture,” wrote Howson. “The Esma consultation is unhelpful in the way that it presents non pre-trade transparent trading as including all systematic internaliser and over-the-counter activity, as well as all activity undertaken under a waiver.”

Cboe Europe President David Howson shares his thoughts on recent market performance, Cboe’s response to ESMA on its MiFID II/MiFIR report, and more. Visit the Cboe blog for details – https://t.co/ml70qVwFJQpic.twitter.com/iRnYCT8fIC

Howson also stated that the double volume cap regime should be completely removed, rather than arbitrary alterations made to the current thresholds. MiFID II introduced caps on trading in dark pools with the aim of shifting volumes onto lit markets

“The DVCs have introduced cost and complexity and delivered no clear benefit to execution performance and end investors,” he added.

He continued that there is also no evidence of investor detriment from periodic auctions. “The platforms, including the enhancements Esma proposed last year, have proven themselves as low impact, price-forming mechanisms that deliver beneficial execution outcomes,” said Howson.

However Cboe did express concern that the significant increase in closing auction volume poses a systemic risk to the efficient and orderly running of markets and should be closely monitored by regulators.

“This trend would be further exacerbated if the choice of low impact trading mechanisms, such as those utilising the reference price waiver and negotiated trade waiver is forcefully reduced,” said the letter.

The U.S. Securities and Exchange Commission’s move to modernize market data infrastructure is an opportunity to improve the system at the margin, but it also presents risks that going too far will be counterproductive.

That was the general consensus of a May 8 Nasdaq-hosted webinar that convened market-structure experts to discuss ‘Reg NMS II: The Impact of Redesigning Equity Market Structure’.

Justin Schack, Rosenblatt Securities

Justin Schack, Managing Director and Partner at Rosenblatt Securities, noted that people complain about the complexity of equity market structure, but ultimately equity markets produce good outcomes for the two most important stakeholders: end-user investors and corporate issuers.

“Let’s not mess with something that is not fundamentally broken,” Schack said. “There are things you can do around the edges and tweaks you can make,” but an overhaul is not indicated, he said.

The SEC in February proposed to update and expand the content of national market system (NMS) data, which has not been done in a significant way since the 1970s. The regulator seeks to open up data provisioning to competition for the first time, with the goal of enabling all market participants to access and benefit from the expanded content.

Tal Cohen, Nasdaq

Nasdaq “favors an incremental and exacting approach to change,” said Tal Cohen, EVP and Head of North American Markets at the exchange operator. The SEC’s Equity Market Structure Advisory Committee favors a similar way forward, Cohen noted.

“That doesn’t mean there aren’t opportunities to modernize our regulatory framework or adjust ‘one size fits all’ rules,” Cohen said. “It’s just a matter of what we focus on and how we approach it.”

Regulatory goals should include improving the resiliency of infrastructure, eliminating single points of failure, and introducing ‘guardrails’ where it makes sense. More broadly, “any comprehensive revision to the rules that govern our maret should consider whether you introduce new levels of complexity or expose us to new risk,” Cohen said.

Aside from opening up the provisioning of NMS data to competition, other specific areas the SEC seeks to address include best bids and best offers for round-lot sized orders; redefining the order-size threshold for protected quotations; and new rules around ‘depth of book’ data.

It’s an open question how the SEC initiative will play out over time, but there is some optimism that the end result will be a net benefit. About half of respondents to a poll conducted during the Nasdaq webinar said they support the SEC initiative.

“Changes are a long time coming. Some of this has been discussed over many years,” said Bojan Petrovich, Executive Director and Head of Trading at JP Morgan Asset Management.

“This is an opportunity to challenge ourselves to improve markets and set a higher bar. There are no easy answers but I don’t think anything is insurmountable.”

The comment period for the SEC’s data-infrastructure modernization initiative ends May 26.

Axoni’s equity swap platform based on its AxCore distributed ledger software is now live following the landmark equity swap transaction earlier in the year between Citi and Goldman Sachs.

The initiative, which has been backed by a working group of fifteen leading sell- and buyside firms in the equity swaps market, is a peer-to-peer electronic confirmation, cash flow matching, and event reconciliation platform. The aim was to find an alternative to the cumbersome legacy processes and infrastructure unable to handle the growing demand for equity swaps and the subsequent increase in data.

Carl Forsberg, Axoni

Some derivatives, such as interest rate swaps, are now fairly standardised due to widespread adoption of post-trade processing platforms such as MarkitSERV. However, most equity swaps such as portfolio swaps, baskets and contract for difference (CFDs), have their own operational processes around lifecycle events. They are executed directly between counterparties, with each maintaining their own books and records to represent the initial trade terms and track any changes through the lifecycle of the trade. Data breaks between counterparties are frequent, leading to substantial operational costs from manually reconciling records against one another.

Axoni’s platform enables post-trade processing between counterparties, without the need for an intermediary or for human intervention. This is achieved via a shared infrastructure that ensures both sides of an equity swap are always synchronised during the entire transaction lifecycle, communicating changes between counterparties in real time.

A key prerequisite for building common, shared infrastructure for derivatives is the recognition and adoption of a standardised data model by market participants. Axoni leveraged the work undertaken by the International Swaps and Derivatives Association (ISDA) in developing standards such as the Common Domain Model (CDM).

Automation of derivatives processing via use of smart contracts is an important area for the trade group who is working on the standardisation and digitisation of legal documentation. This groundwork will facilitate more accurate capture and analysis of complex derivatives contract data, allowing for greater automation of post-execution obligations and events.

Ciarán McGonagle, ISDA

Ciarán McGonagle, Assistant General Counsel at ISDA, says “The key question is: how much of a derivatives contract can we realistically automate? ISDA has developed a series of principles that can help to inform this decision. Certain types of operational provisions lend themselves better to automation than provisions that require subjective judgement. Automation must also be efficient. There must be sufficient benefit to justify implementation.

He adds, that “given ISDA’s traditional role in the market, our focus has been on developing common legal, process and data standards upon which these new technologies could be developed and implemented, such as the ISDA Common Domain Model and ISDA Clause Library. We believe that there are likely to be significant efficiency and cost-saving benefits associated with automation. We are working with our members to consider the implications of increased automation of existing business and operational processes from a legal, regulatory and operational perspective.”

Carl Forsberg, Senior Director of Enterprise Solutions at Axoni, says “Our equity swaps platform is the first step towards a future with substantially more efficient post-trade processes across all OTC derivatives, not just equity swaps, enabled by the use of DLT. The opportunities within capital markets are enormous and we are just getting started. Expanding what we have built into other asset classes is already underway. Axoni is active in five additional areas of capital markets that require multiple parties to share and reconcile data.”

Founded in 2013, Axoni has developed a range of integration mechanisms to foster more widespread adoption of distributed ledger technology (DLT) in front-to-back operational infrastructure within financial institutions. These range from application including Application Programming Interface (APIs) to event publishers, user interfaces and plug-ins to traditional databases, allowing enterprises to seamlessly integrate the platform into their existing technology stacks, without requiring DLT-specific knowledge.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.