By Adam Sussman, Global Head of Market Structure, Liquidnet.

Artificial Intelligence is not necessarily about predicting price, but predicting what kind of content, products, or services a user would find valuable.

According to a recent survey, 71% of US respondents believe that Artificial Intelligence (AI) will eliminate more jobs than it creates. Would the number be much different within the financial services industry? Almost everything I read or hear about on AI and automation is focused on the wrong issues. The discussion on automation versus augmentation is unhelpful; it minimizes the fear of job losses by downplaying the promise of massive efficiencies. Artificial Intelligence, like many buzzwords, is as popular as it is misunderstood. A recent Liquidnet-commissioned Greenwich Associates study indicates that only about 10% of Portfolio Managers and analysts use AI in the investment process. Yet, anecdotally, aren’t we hearing that EVERYONE has embraced AI? I bet a survey of those same firms’ marketing departments would show different results.

My point is that a lot of people who say they are using AI are not, and some people who are using AI don’t even know it. The latter is the more interesting case because when technology is put to its best use, we don’t know we are using it. I doubt that the folks that use 3rd party tools that leverage AI (6%), within the same Greenwich Associates study cited above, know exactly where and how AI is being deployed.

There are a few reasons why AI has not been more widely adopted. First, many alternative data providers tout their use of AI to generate a trading signal. They take unstructured content, such as written content and satellite imagery, and use various techniques to translate that raw content into structured data. AI can accelerate and improve the process because there are millions of data points (words and pixels) to train the model, and a robust training set with which to do it.

Even when the above is done well, the challenge is that the fundamental analyst doesn’t typically benefit from a data set that tries to predict price action in days or even weeks. They are called “long-term” investors for a reason. They care less about what the number of cars in the retail parking lot means for next quarter’s short-term revenue miss, and more about what the number of cars in the employee parking lot means for hiring trends.

Another shortfall in the use of AI is among investment research tools. According to the same Greenwich survey, alerting functionality is being used by just over half of the 56 respondents across US, Europe and APAC. The use of these alerts is for relatively simple events such as a new company filing or earnings announcement.

One use case that resonates with fundamental analysts is using Natural Language Processing (NLP) to help uncover when a company has made a notable change to some part of its filings. There is a substantial amount of academic literature in this space; the more interesting ones look at the words, phrases and changes that suggest future corporate events such M&A, litigation, or fraud. How that might translate into price movement is not necessarily a useful step.

In other words, one value proposition of Artificial Intelligence is not necessarily about predicting price, but predicting what kind of content, products, or services a user would find valuable.

Candle stick graph and bar chart of stock market investment trading. Analysis Forex price display on computer screen.

Could mega-retailer Walmart launch its own digital currency?

Give its resources and reach into the consumer sector, yes, and it might given Facebook’s own Libra stablecoin a rival of sorts.

While Facebook has formally announced its own stablecoin – Libra – Walmart has recently filed a patent with the government for a US dollar-pegged yet-to-be named stablecoin offering. The filing states that the potential coinage looks to serve underserved or low-income persons that find traditional banking alternatives too costly.

The filing, published in the U.S. Patent and Trademark Office (USPTO) recently, gives a detailed blueprint for “generating one digital currency unit by tying the one digital currency unit to a regular currency.” That would be a stablecoin.

Furthermore, this new blockchain-based digital currency “may be pegged to the US dollar,” the filing added, and could be used at “only at selected retailors or partners.”

“The digital currency can provide a fee-free, or fee-minimal place to store wealth that can be spent, for example, at retailers and, if needed, easily converted to cash. Such accounts could even earn interest,” the filing reads. “Digital currency may be tied to a national currency, such as the US dollar, so funds can be added or taken out easily. The digital currency value could, in some embodiment, be tied to other digital currencies.”

The patent was originally filed in January and is application #20190236564

Abstract business chart with uptrend line graph, bar chart and diagram in bull market on dark blue background.

The buy-sides’ largest brokers receive by far the largest percentage of flow, according to Tabb research.

Continuing its series of exclusive benchmark research information covering US Institutional Equity Trading for the past 15 years, TABB Group today published its third of six studies aggregating the collective intelligence drawn during the first and second quarters of 2019 from 92 heads of trading at institutional investors on the capabilities and services provided by 70 brokers.

“US Institutional Equity Trading 2019: Broker League Tables,” co-written by Larry Tabb, TABB Group founder and research chair, Campbell Peters, US equity market structure research analyst, and Elyse Gerard, director of market outreach, analyzes the 92 firms’ commission allocation and how each of the 70 brokers scored by major service categories, including commissions; trading algorithms; high-and low-touch coverage; electronic- and high-touch blocks; execution consulting; research; market structure insight; transaction analytics; central risk books; and capital. More specifically, the rankings include a breakdown of the Top 5 and Top 10 brokers by commissions and the Top 5 algo brokers for long-only and hedge funds, both weighted and by frequency of mention.

According to Tabb, there are key takeaways that both institutional investors and their brokers should understand as they begin to interpret TABB’s exclusive broker league tables. “It’s critical for brokers to understand where they sit in the eyes of their clients, that the buy-sides’ largest brokers receive by far the largest percentage of flow. The implications are far greater for hedge funds as their top broker tends to be their prime.” He goes on to explain that asset managers are more inclined to give their largest broker up to 18% of their order flow, with hedge funds giving their lead broker as much as 31%. “Hedge funds’ largest broker algo tends to be their largest prime broker.”

In the ranking by commissions, Morgan Stanley took top honors, followed by JPMorgan and Bank America Merrill Lynch, with Credit Suisse and Goldman Sachs rounding out the top five brokers. Peters points out that this ranking includes feedback on all 70 brokers. While Morgan Stanley led the league table, JP Morgan led the field in catering to most of the large buy-side firms with >$150b AuM. Here, JPMorgan was followed by Bank America and Goldman Sachs.

While commissions are critical, says Tabb, the buy-side firms ranked algorithms as the top reason why they allocated order flow to a specific broker. In this category, there was a significant change from 2018 when the buy side’s most critical service was high-touch coverage, followed closely by trading algorithms. He says the buy-side ranked the combined Virtu and ITG at the top the algo list. However, if taken separately, i.e., funds that mentioned Virtu or ITG separately, JPMorgan would have been the most extensively used algo provider, followed by UBS and Sanford Bernstein.

If the buy-side prioritized their order flow in the same manner as they ranked brokers’ services, their top brokers would be JPMorgan followed by Goldman Sachs.

Two other critical factors in today’s US equity market are liquidity and sourcing blocks, both highly prized by institutional investors. In this category, Jones Trading ranked the highest in providing agency block flow, while Goldman Sachs ranked second and Liquidnet ranked first for providing access to electronic block order flow.

Candle stick graph and bar chart of stock market investment trading. Analysis Forex price display on computer screen.

Re-imagining the Buy-side Dealing Desk

Over the last few months discussions around the benefits of outsourcing the dealing desks have intensified. As a result of asset managers facing a number of pressures, from regulation to fee compression and performance, the option of outsourced dealing is gaining momentum. In a recent report, Consultancy Opimas suggests that by 2022, approximately 20% of investment managers will outsource at least some of their trading desks. We talk to Dan Shepherd, CEO of BTON Financial, an outsourced dealing desk for medium-sized asset managers, to find out how the industry is changing.

Tell us about BTON Financial? What does it provide?

We are an outsourced dealing desk focussed on electronification to enhance asset manager performance. Specifically, we perform the role of a broker-neutral, smart broker router. We receive orders via FIX and then send them out to the most appropriate broker by instrument type and customer.

What makes BTON Financial different?

Our real differentiation is our focus on using a technology slant to help mid- and small-sized asset managers survive and thrive in the post-MiFID II trading environment. Automation and electronification of the trading desk is happening at a rapid pace across asset classes. For example, according to a Greenwich report, in the U.S. corporate bond market, roughly 70% of the trades executed are for 100 bonds or fewer (equivalent to $100,000 or less) and over 90% are now done on electronic trading platforms. So at BTON Financial, we have set out to automate the trading process as much as possible.

We are also different in that we have no ties to existing brokers, meaning we can access the best facilities at which to execute trades. We think this independence is key to our success as it helps firms comply with MiFID-mandated best execution policies, and automation lends itself perfectly to comprehensive audit trails.

In addition, because we charge a subscription fee through a SaaS model, rather than commission through a BPS model, we are much more aligned with our customer. The focus is not about the client trading more, but rather about trading in the right way.

What kind of interest is there from the buy-side in outsourcing their trading desk?

Our typical client is a traditional mid-sized asset manager with 150bn AUM and below. We help these firms achieve economies of scale though outsourcing. This helps the smaller asset managers keep up with the huge players who are in turn making significant moves on the technology-side of things.

We are also offering to augment existing trading desks for some larger asset managers who would like to better manage their large-in-scale and more esoteric trades. To achieve scale and cost reduction, these types of automatable trades can be filtered out to BTON Financial.

What do you think has prompted this interest?

Asset managers have been heavily affected by the MiFID II regulations. There has been a radical unbundling of services and clear lines are required for cost of research, trading, trade reporting and transaction reporting. In addition, heavily reduced margins are having an affect on large technology projects and overheads.

Mid- and small-sized asset managers need to change in order to survive in the new post-MiFID II environment. Larger firms on both the sell-side and buy-side have access to economies of scale which helps ensure their success. But the electronification brought about by MiFID II can also serve small and mid-sized firms as well, especially when accessed through a SaaS model. We can help smaller asset managers compete with the big players.

What do firms hope to achieve from outsourcing?

Outsourcing is a way for the smaller and mid-tier firms achieve economies of scale related to brokerage costs. In addition, by connecting to an outsourced trading desk functionality, traders can now have access to a greater set of data for trading decisions. Non-proprietary, consolidated data sets of executions conducted across the outsourced technology platform are anonymised and shared. Trading desks can then use this information to improve trading performance – something that would previously have been cost prohibitive for smaller firms to do on their own.

With the Federal Reserve delivering on its well-telegraphed rate cut, the risk-on rally continued in July as equity ETFs attracted over $20 billion of assets for the second consecutive month, according to the latest U.S. Listed Flash Flows report from State Street Global Advisors (SSGA). Despite the headlines and the fact Equity ETFs have accumulated over $40 billion over the past two months, they are still 30% off last year’s pace, through the first seven months of the year.

“Looking past July’s market tranquility, the equities rally is not global,” said Matthew Bartolini, head of SPDR Americas Research at SSGA. “Nor does it have deep market breadth in the US, evidenced by the sector performance as well as the ratio of the levels for the market-cap weighted S&P 500 relative to the equal weighted S&P 500 coming within a few points of hitting an all-time high. The latter indicates that large firms are at the helm of this rally ship, and rising tides are not lifting every boat (asset class).”

With such an environment, expect some volatility and that should affect future fund flows, Bartolini added.

“The slower pace of equity flows is another indication of a low participation rally, worth watching if markets turn volatile,” Bartolini said. “While equity ETFs are well off their pace from last year, the broader ETF market is not that far off (3% lower) as a result of the strength in fixed income flows. Bond ETF fund flows are running 42% higher than at this time last year. A lot of this strength is due to the record flows in June. For July, the flows were still strong, just more in line with the 36-month average of $9 billion a month.”

Commenting on equities on a global scale, SSGA noted the strength in equity flows was primarily driven by US- related exposures. US geographic-focused ETFs took in the most on both a notional dollar amount (+$21 billion) as well as on a percent of start-of-period assets for the month (+0.09%). With the US being the only major region to post positive returns in equities in July, as well as over the past three months, this is not surprise.

“Outside the US, there was little interest to express a risk-on view, with the exception of broad-based international developed exposures,” Bartolini said. “Single-country funds had outflows once again, and emerging markets had outflows for the second-straight month after being favored to start the year. As a result, EM’s three-month total has dipped negative.”

Away from equities, bond ETFs saw nearly $9 billion in fresh inflows during the month with investors favoring Aggregate, Mortgage-Backed and High Yield exposures. According to SSGA data, these segments attracted $2.8 billion, $1.7 billion and $1.4 billion, respectively.

“With flows (fixed income) 42% higher than last year’s pace, there is a strong chance of surpassing the $100 billion mark for the second time in history – 2017 was the first time,” Bartolini said. “But will 2019 break 2017’s record of $127 billion of inflows? Estimates are worth about as much as the paper they are written on, but using the trailing 12- and-36-month average fund flows for fixed income ETFs indicates that 2019 has a puncher’s chance.

One item of note, Bartolini said was the exodus from Healthcare ETFs.

“As a result of sizable geopolitical headline risk, given the amount of airtime this topic received during the Democratice debates, Health Care witnessed the greatest outflows of any sector in July, shedding $1.1 billion,” he said. “Conversely, Technology and Real Estate saw the most inflows during the month, attracting $779 million and $585 million, respectively.”

In the High-Yield sector, the last two months saw $4 billion in flows in June and $1.4 billion in July, marking the highest two-month total since 2012 and the third-highest ever.

Global trade and digital information technology using blockchain for

Managing workflows across multiple blockchains is approaching.

Although they do not carry the same cachet that they did a couple of years ago, distributed ledgers have established firm footholds in the financial services community. It is only a matter of time before buy-side and sell-side firms will need to integrate their workflows across multiple distributed ledgers that support different digital assets and front-, middle-, and back-office processes.

Markets Media caught up with Duncan Johnston-Watt, co-founder and CEO of DLT-management platform provider Blockchain Technology Partners (BTP), to discuss when and how these new challenges will wind up on the Wall Street CIO’s plate.

How close are asset managers and broker-dealers to needing to manage financial instruments and workflows across multiple distributed ledgers? Is it an actual thing yet?

The ability to manage financial instruments and workflows across multiple distributed ledgers is rapidly emerging as a challenge for asset managers and broker-dealers given the lack of standardization in the permissioned distributed ledger space.

Therefore this is definitely something that they need to be aware of and factor into their thinking in much the same way that they have had to learn to handle the plethora of market data platforms and liquidity pools in the past.

However, this is also an opportunity for fintech firms to develop tools to help asset managers and broker-dealers handle this complexity just as they have done so historically in, for example, the order management space.

Finally, while there is lack of standardization when it comes to distributed ledger technology, interoperability is possible with the right level of abstraction as exemplified by DAML, the smart contracts language, which Digital Asset open-sourced earlier this year. In the derivatives space, Digital Asset have teamed up with ISDA to create a reference implementation of the ISDA Common Domain Model (CDM). Written in DAML, this library will ensure that derivatives are traded and managed consistently across multiple distributed ledgers.

Would firms be more likely to roll their own management framework or rely on a hosted offering?

It is important to understand the difference between permissioned and public distributed ledgers. In the permissioned world, all the participants are known and there is a governance mechanism for admitting (or ejecting!) participants. Therefore permissioned distributed ledgers are the logical choice for most if not all consortia or multi-party use cases in a highly regulated industry such as financial services.

Against this backdrop, firms participating in a consortium underpinned by a distributed ledger actually have three alternatives when it comes to joining the network. They can rely on a service provider; roll their own nodes or use a blockchain management platform to facilitate this.

Although it may appear to be attractive for firms to use a service provider this only makes sense if its Blockchain-as-a-service (BaaS) offering supports the type of distributed ledger in question. Furthermore, it means putting their trust in a third party which arguably undermines one of the basic tenets of distributed ledgers, namely, that control is decentralized.

This leaves two alternatives for firms. Either they bite the bullet and each rolls their own management framework to contribute and maintain their nodes on the network or they adopt a blockchain management platform to facilitate this process. The first option imposes a huge overhead in terms of both deployment and ongoing management and maintenance whereas the second avoids this while ensuring that each firm still retains full control of its own nodes.

How would firms roll their own framework? Has the industry developed a set of best practices yet?

We would argue that the best way of participating in a distributed ledger is for a firm to use a blockchain management platform to facilitate this while retaining full control of its own nodes.

In terms of best practices such a blockchain management platform should be something that a firm can run itself; provide complete visibility into the stack being managed; automate standard operations and target Kubernetes as the runtime platform. Kubernetes is now the de facto standard for container management and can be deployed on-premises or in the cloud using a kubernetes-management platform such as Rancher.

What do you see as the next sea change in this space?

Financial services have a great track record of exploiting advances in middleware technologies by adopting the right level of abstraction.

In other words, to take full advantage of distributed ledger technology firms and fintechs need to focus on application development and avoid being tied to a specific implementation.

Once you get beyond the hype, distributed ledger technology is just another middleware play – this sea change in perception will unlock its true potential. We’ve been in this movie before with message-oriented middleware for example.

Where are the most advancements taking place in this space?

The two areas where we see the most innovation happening are in the smart contracts space and the underlying performance of distributed ledgers.

The first area – smart contracts – is exemplified by DAML which is built on a powerful functional programming language, Haskell, which, now it has been open-sourced, is being implemented on a wide variety of persistence layers ranging from distributed ledger technologies such as VMware Blockchain, Hyperledger Sawtooth and Corda to AWS Aurora and others.

The second area – performance – is crucial to the widespread adoption of permissioned distributed ledgers. This is closely related to research into both consensus algorithms and different privacy models that enable the immutable sharing of data while preserving Chinese walls where appropriate.

There is one thing still missing from the data debate — and that’s data.

The author of a recent op-ed in Canada made the comment that “rise in data fees has …a significant bearing on …net investment returns.”

That’s a big claim, sadly without any supporting calculations, which is symptomatic of much of the current data debate.

But let’s try to use the data that’s available to take a top-down look at investor costs and see how this claim stacks up.

How big are mutual funds?

Before we get into cost math, we need to understand how big mutual funds are, and how much they trade.

ICI data shows that equity mutual funds represent 52% of the $17 trillion in U.S. mutual fund assets, or $9.5 trillion. They also report that mutual fund turnover has fallen to just 32% (per side). That equates to trading of $5.9 trillion per year (buys and sells).

In contrast, the whole U.S. equity market trades $70 trillion per year. That’s $140 trillion(buys and sells).

Although it seems hard to believe, this puts mutual fund trading at less than 5% of market-wide activity. That’s in line with some estimates of retail trading.

What are the different costs to investors?

Let’s first be clear: The results below don’t suggest costs are “bad” for investors. Managing investments is not cost free; even those low priced index funds need a portfolio manager, custodian and accountants to calculate year-end distributions. For those investing with an advisor, it pays to ensure you save sensibly and have a secure retirement. And with a reported $27 trillion invested in U.S. equities directly and via mutual funds (see below), simple math means small charges can add to large notional values.

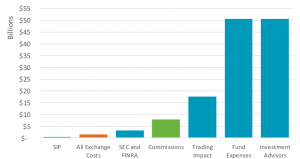

When thinking about costs, we look at five major types of costs: Investment Advisors, Mutual Fund Expenses (MER), Trading Impact, and Commissions and Regulatory (SEC and FINRA fees). To address the claim above, we also look at Exchange costs and costs for the Securities Information Processor, which we highlight are bundled into MER and Commissions.

Looking at all of these, it certainly puts exchange costs in context, and hopefully encourages a more data-driven debate. Even looking at grossed up costs (Chart 1), Exchange and SEC fees are a small part of the total equation. This is especially noteworthy considering the important role of exchanges in bringing companies to market, regulating the market and supervising trading, which provides the returns that help secure the retirement of U.S. workers.

When allocated based on turnover (below), the inherent cost or impact on investor’s returns is even smaller.

Chart 1: Estimated total revenues and investor costs across U.S. equities

Not all the data for this chart is freely available. Here is how we estimate it:

Management Expenses are probably the largest cost to investors. ICI reports average expense ratios have fallen to 0.55% in 2018. Based on other ICI data that suggest U.S. equity mutual funds are $9.2 trillion, which adds more than $50 billion in costs to investors.

Note that management expenses usually include things like SIP data costs, EMS and terminal costs, although soft-dollar agreements may pay these out of commissions. For completeness, industry-wide professional SIP user costs total around $0.2 billion per year.

Investment Advisor fees: Other data shows households hold more stock in their own account ($17 trillion) than mutual fund holdings. However, these investors often also pay an investment advisor to assist them manage their assets. Data on industry revenues from U.S. equities is hard to find, but typical fees are reportedly around 1% per-annum on assets, so revenues could easily be the around the same as the cost of managing mutual funds: $50 billion.

Market Impact costs: There is established literature about the fact that that trading causes market impact, with a Transaction Cost Analysis (TCA) industry that has developed to measure and manage it. It’s simple economics really. Buying (or selling) large quantities of a stock adds to demand (or supply) which moves prices up (or down), sometimes permanently. Interestingly, it’s generally reported that impact costs have been falling for decades. Recent ITG estimates imply average shortfall costs in the U.S. of 30 basis points (bps) per trade. We’d highlight that’s lower than any other country ITG measures, which speaks to how well the U.S. market works. But even then, on $5.9 trillion of trading, that adds up to almost $18 billion.

U.S. Equity Commissions were reported recently by Greenwich Associates at $7.4 billion. Equity commissions are “bundled,” and include a number of other expenses including net exchange fees, broker technology costs, settlement costs and even research.

SEC fees: SEC fees are reportedly around $2.3 billion and FINRA also charges brokers around $1 billion per year. Allocating these costs across the industry by value traded (see below) results in a cost to mutual funds of around $0.13 billion, which is also a rounding error on investor returns.

It is also possible to estimate some of the components that are included in the $7.4 billion of bundled U.S. Equity commissions.

The same Greenwich Associates study estimated around $4 billion of commissions was for research, or roughly around 50%.

Extrapolating our own study, all-in-exchange costs look to be around $1.5 billion. However based on trading levels below, the allocation to mutual funds would be less than $0.065 billion. The rest is incurred by other participants, from hedge funds to arbitrageurs and proprietary traders.

How much do those costs affect investor returns?

So, back to the original question: How much do these costs affect investor returns?

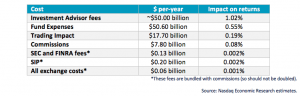

Remember that ICI data showed U.S. mutual fund assets are around $9.2 trillion. Also remember that for “industry-wide” costs, allocations to investors will be less than 5% based on their contribution to value traded (see * in table below). Doing some simple math, Table 1 shows the estimated impact on returns from each of the investor costs we’ve discussed.

Table 1: Estimated impact of costs on investors returns

Data analyzing in exchange stock market: the candle chars on display. Analytics price change cryptocurrency BTC to USD (Bitcoin / US Dollar), the most popular pair in the world. Big Bitcoin logo.

Industry leader Bitcoin.com has announced plans to launch a new cryptocurrency exchange on 2 September.

The exchange offers a place to trade with a clean, simple interface to promote easy navigation, along with high-liquidity and a powerful matching engine to support fast trading.

As a trading platform, The Bitcoin.com Exchange will complement the existing Bitcoin-focused products and services provided by the fintech company. Bitcoin.com Executive Chairman Roger Ver explains, “We’re always working to make Bitcoin Cash and other digital assets more accessible to everyone. Back in June, we released Local.Bitcoin.com where you can buy and sell Bitcoin Cash specifically. Now, with The Bitcoin.com Exchange, you can diversify your cryptocurrency portfolio, too.”

Traders will be able to trade against some of the most popular base currencies including Bitcoin Cash (BCH), Bitcoin Core (BTC), Ethereum (ETH), and Tether (USDT). These will give users the chance to exchange a broad array of digital assets through dozens of different trading pairs.

It’s also been announced that the exchange will soon support a new trading option: Simple Ledger Protocol (SLP) tokens. These tokens, which exist on the back of the Bitcoin Cash blockchain itself, can be created by anyone and will soon be tradable directly on The Bitcoin.com Exchange.

Ver highlights, “We’re on the cusp of something very exciting with SLP tokens. It’s the beginning of a world where we can tokenize anything and, as people realize the potential this holds, they’re going to start demanding a place to trade their tokens. That’s why we’ll be supporting SLP tokens on The Bitcoin.com Exchange.”

Additionally, Bitcoin.com’s exchange also seeks to reassure traders. Speaking about the upcoming exchange launch, Ver explains, “Bitcoin.com has been around the space for many years now and we hope that the quality products we’ve already built—our wallet, our merchant app, and so on—help to reassure users and remind them that we’re an established brand they can trust.”

In the run-up to the launch of The Bitcoin.com Exchange, users can pre-register and will be rewarded for doing so. Rewards include 25% discounted trading fees for the first three months and the chance to win prizes worth over $10,000 through a prize draw. To be eligible for this prize draw, users must pre-register and then make a trade within the first week of the exchange launching.

Bitcoin.com will be revealing which prizes can be won over the next few weeks on their Twitter channel. The first prize, which has been revealed on a company blog post announcing the exchange, totals $5,000 with five winners each winning $1,000 of BCH. All prizes are exclusive to users who register before the exchange launches at the beginning of September.

The buy-side want systems to track the value of research.

There is a slow evolution in the research market as the buy-side is working out how to measure quality according to Andrew Skala, head of research solutions at Bloomberg.

The European Union’s MiFID II regulation required the unbundling of research payments from trading commissions, and most asset managers have since chosen to pay for research out of their own revenues.

Skala told Markets Media that an increasing number of long-only funds are setting up internal research teams.

“Fund managers are raising money based on the depth of their research so need more structure in the process to determine which of their ideas are working well,” he added.

Bloomberg’s Research Management Solutions (RMS) allows the buy-side to structure the research process and integrate it with their portfolio managers. Skala said RMS is different from other research aggregation platforms because it integrates sell-side research into the buy-side workflow and also the fund manager’s internal research into the workflow of the firm’s portfolio managers. RMS is also integrated with Bloomberg’s data, news, analytics, communications and trading solutions on the terminal,

Skala continued: “There has been dramatic reduction in sales forces on the sell side which is boosting the transition to quality. Fund managers may be prepared to pay more for the research they want.”

For example, Deutsche Bank announced a restructuring this month with the firm exiting the vast majority of equities sales and trading business, while maintaining a focused equity capital markets presence and selected equity and macro research.

“As more providers focus on research as a core competency, research will become better and stronger over time,” Skala added.

Bloomberg said in August last year that BMO Global Asset Management and Union Investment had adopted RMS in response MiFID II.

With RMS fund managers can block receipt of certain content except from their preferred providers. Analytics and reporting tools allow firms to monitor and evaluate corporate access, research, and sales services based on their interactions from the terminal, Microsoft Outlook and bespoke broker files. Buy-side firms can use this data to manage research invoices and to connect to parties who will process payments. In addition, the platform has valuation scorecards to track research consumption and interactions to their budgets.

Holly Anderson, business manager, investment EMEA at BMO Global Asset Management, said in a statement at the time: “Bloomberg has been a very efficient interface between us and the sell-side as we all navigate this new regulatory landscape and the need to unbundle and value broker-provided services.”

Kevin Coleman, chief executive of expert network Coleman Research, agreed that there is now a bigger focus on price discovery and value. He told Markets Media: “Unbundling is hard to do and there is a journey for the buy side as they do not have the right systems in place to track the value delivered.”

Liquidnet survey

Liquidnet agreed that the mix of brokers being used by the buy side is changing. The institutional investor block trading network’s survey in April this year said 55% of respondents are taking research from more than fifty brokers globally, the same as last year, but the composition of the brokers is not the same.

The study, MiFID II Unbundling Research – Canary in the Coalmine II, found that 69% of buy-side firms chose bulge bracket brokers for research but they differentiate between those who provide basic waterfront coverage and those where they want to engage with an individual analyst.

Rebecca Healey, Liquidnet

Rebecca Healey, head of market structure and strategy, EMEA at Liquidnet, said in the report: “There is an increased interest in smaller brokers’ offerings or specialist research provision as a way to differentiate themselves and add value to their investment process.”

She also agreed that as the sell side develops a better understanding of where it can add value and what it can charge, there may eventually be an increase in some pricing models.

The survey found that since MiFID II came into force overall research spend remained constant for nearly half, 48%, of asset managers while 13% of asset managers are choosing to increase their research spend.

Healey said: “By honing in on quality and alternatives, the opportunity for growth in research provision could be an opportunity for providers globally, not just in Europe.”

For example, 80% of research providers are now increasing their coverage of small and mid-caps in a bid to diversify their product offering. Healey continued that new third-party providers offering differentiated research will continue to emerge.

Coleman agreed that the buy side is looking for alternative sources of data. He said: “Artificial intelligence and other technology is being further developed so institutions can look for additional forms of research when making investment decisions.”

Skala said Bloomberg is looking to increase use of machine learning to detect themes and uncover content in the natural workflow of fund managers. “We want to increase discoverability and surface the most relevant content,” he added.

Acquisitions

In May Liquidnet acquired RSRCHXchange, a marketplace and aggregator for institutional research which was launched in 2015 to distribute research from a variety of providers to asset managers through a centralized, cloud-based hub.

Brian Conroy, Liquidnet

Brian Conroy, president of Liquidnet, told Markets Media at the time that the addition of RSRCHXchange allows Liquidnet to provide a new level of research and analytics more efficiently so the buy side can capture more alpha.

Brian Kleinhanzl and Mike Brown, analysts at financial services boutique Keefe, Bruyette & Woods, said in a podcast this month that firms are looking to improve best execution and research capabilities to competitively position themselves under MIFID II.

“Some are investing to do so while others have acquired,” added the analysts. “For potential targets, the ability to be a part of a larger firm is attractive due to the stability provided from a more diverse business mix, plus larger firms can provide benefits such as broader distribution, access to a balance sheet, and of course cost synergies.”

The analysts highlighted three transformative deals this year – the acquisition of research boutique Autonomous by asset manager Alliance Bernstein; broker Janney Montgomery’s acquisition of FIG, a boutique investment bank and research provider; and broker Piper Jaffrey’s acquisition of boutique Sandler O’Neill.

“Year-to-date announced volumes for financials are 8.5% higher than the same time last year and last year was up 8% year over year,” said Brown. “In the bank space, high regulatory costs and the need to invest in digital capabilities continues to drive consolidation. “

Brown said he expects consolidation to continue due to fee compression and the continued need to invest in technology.

“In advisory for financials specifically, market share on the league table-based on deal value really drops off after the bulge bracket firms and a few top specialist firms, so I see a clear opportunity for those in the 5-15 position to consolidate and become larger contenders in the financials space,” he added.

We're Enhancing Your Experience with Smart Technology

We've updated our Terms & Conditions and Privacy Policy to introduce AI tools that will personalize your content, improve our market analysis, and deliver more relevant insights.These changes take effect on Aug 25, 2025. Your data remains protected—we're simply using smart technology to serve you better. [Review Full Terms] |[Review Privacy Policy] By continuing to use our services after Aug 25, 2025, you agree to these updates.

, the most popular pair in the world. Big Bitcoin logo.")