F/m Investments CIO urges diversification amid US political gridlock and AI boom

New Trader TV This Week – Political dysfunction in Washington and the ongoing US government shutdown will be major forces unsettling markets this week, says F/m Investments’s Alexander Morris. Speaking to Trader TV, the chief investment officer discusses what’s driving market sentiment, whether the AI boom is sustainable, and the likelihood of a broader market correction. He also discusses ways to approach the upcoming week and other market events to pay close attention to.

Abdoulaye Ba, head of multi-asset trading, Banque de Luxembourg

Abdoulaye Ba has been promoted to head of multi-asset trading at Banque de Luxembourg.

He replaces Quentin Gaget, who has held the role since 2023.

Banque de Luxembourg reported net profits of €79.4 million in 2024, up 5% year-on-year.

Ba has close to 20 years of industry experience and has been a multi-asset trader at the bank since January. Prior to this, he was a fixed income trader at service provider Natixis TradEx Solutions and a senior business analyst at Ostrum Asset Management.

Valdene Reddy has been named CEO of the Johannesburg Stock Exchange (JSE), effective 1 April 2026.

She replaces Leila Fourie, who has held the role since 2019.

The JSE has a US$1.23 trillion market cap, as of July 2025. A total of 435 companies are listed on the exchange.

Under Fourie’s leadership, the JSE partnered with a range of exchanges and data vendors as it sought to increase its global presence.

A 2023 partnership with Big Xyt to develop a data analytics solution distribution service was followed up by an agreement with DataBP in 2024, intended to improve data management services.

Also in 2024, Euronext joined the JSE’s fast-track listing route as part of the exchange’s push for dual- and multi-listing – an initiative already supported by exchanges including the LSE, ASX and NYSE.

Reddy has 25 years of experience and has been director of capital markets at the JSE since 2020. Prior to this, she was head of equities and equity derivatives at the exchange.

Her career began in equity derivatives sales and trading at Bank of America Merrill Lynch, after which she worked in equity derivative sales at Renaissance Capital.

Hudson River Trading (HRT) and Susquehanna (SIG) won the August price improvement race. This may be the symptom of the securities, order type, and order size they choose to favourably market for retail brokers, Global Trading analysis reveals.

US equity retail volumes cooled by 11.6% month-on-month in August according to our data from BMLL Data Lab, and aggregate price improvement (PI) delivered by market makers fell to US$382m from US$447m in July (-14.5%), a touch below this year’s monthly average of US$388m (-1.6%).

On execution quality (E/Q), Hudson River Trading (HRT) posted the lowest share-weighted median E/Q at 0.315, with Susquehanna (SIG) next at 0.335, both clear of their competitive field despite broad, visible shifts in the shape of every market maker’s E/Q distribution.

Substantial price improvement versus the national best bid-offer (NBBO) are disclosed in 605 forms: Citadel Securities delivered US$130.9m on 25.15bn shares (-10% MoM) , Virtu US$86.2m on 16.2 bn shares (-8% MoM), SIG US$65.4m (-15% MoM), Hudson River Trading US$57.5m (-10%), with Jane Street US$26.3m (-32%) and Two Sigma US$11.3m (-13% MoM).

In August, volumes for our lit proxy printed 123bn shares versus 139bn shares (-11.6% MoM). Trades’ E/Q aggregate for our market proxy delivered US$632m versus US$707m improvement in July equally, down 10% MoM.

Looking at our 0 to 2 E/Q (the realised spread versus prevailing spread ratio) distributions of price improvements or volume traded, which we build for each market maker, and comparing the shape of E/Q density distributions, it is apparent why SIG and HRT achieve best execution for retail traders on aggregate: Most of their volume sits in very tight bins with E/Q below 0.4 and the their median E/Q is also the lowest.

HRT improved at the margin in August and became the best market maker to trade against with on average for retail; Its median E/Q edged down from 0.344 to 0.315 and the share of ticker / order size / order type E/Q prints with execution quality better than 0.4, where retail trades at better than 40% of the distance between the NBBO and the mid price, rose to 66.6% (from 64.0% in August).

The mode, which is the value that appears the most in the distribution stayed low with a peak around 0.275. This signals consistency rather than just statistical mix artefact, where one type of trade or securities filles would skew the whole E/Q distribution, for market orders, which are most orders that they fill. HRT’s PI of US$57.5m fell in line with volumes (-16.6% MoM, not because execution quality slipped.

SIG became a close second on median quality but saw its distribution shift right: its median E/Q went from 0.295 to 0.335 and the sub-0.40 E/Q share fell to 52.4% from 61.9%. The peak migrated from 0.285 to 0.365 pointing to slightly wider realized spreads for retail trading against it. PI landed at US$65.4m (-14.9% MoM), roughly in line with the market-wide volume pullback.

Citadel Securities provided retail traders with the month’s largest volume of PI, as the biggest market maker, at US$130.9m (-13.9% MoM) but showed the most pronounced execution quality deterioration, as shown by the right shift in its E/Q distribution; Its median E/Q went from 0.405 to 0.515. The better than 0.4 E/Q-share of execution also fell from 47.6% to 27.5%. The distribution’s peak moved from 0.285 to 0.485, indicating, maybe, a heavier mix in names/contexts where the realised spread is inherently larger.

Median E/Q Spread Ratio Over Time

Virtu median E/Q also degraded in August to 0.515 from 0.444 in July. PI delivered to retail were US$86.2m (-14.0% MoM).

In very liquid, directional exchange traded funds (ETFs), market makers’ E/Q tends to converge. For example, July’s triple levered Nasdaq ETFs (TQQQ) and its reverse triple short (SQQQ) were traded by most market makers with low E/Q dispersion (standard deviation of E/Q at 0.11), and large-cap stocks like Apple or Tesla also showed tight clustering. Most market makers have the same colours in these securities on our heat map reflecting similar execution quality.

In more idiosyncratic or leveraged exposure securities, E/Q diverges. July’s silver trust (PSLV) and single-name outliers like Lucid group (LCID) showed much wider E/Q dispersion across makers (standard deviation of E/Q up to 0.25–0.39). That’s probably where skill, inventory, and microstructure tactics bite and where mix changes can move a firm’s aggregate E/Q even when its process quality is steady.

In August’s, the top 10 retail traded ETFs were dominated by levered ETFs such as the triple semiconductor ETF and inverse, the triple Nasdaq and inverse ETFs, the double and inverse Tesla ETFs, or more esoteric ones like the ultra income ETF ULTY that sells weekly covered call. For these, order-type filled by market makers diverged in ways that line up with the E/Q differences per market maker. SIG received and executed the highest share as market orders (65% on ETFs), with Citadel Securities and HRT in the mid-50s and Two Sigma a touch lower; Jane Street stood out for the largest marketable-limit share filled (≈50%) and the highest inside-quote filled among peers.

Where the ETFs are most liquid and directional, like the triple Nasdaqs, or semiconductor ETFS, E/Qs are fairly clustered, but Jane Street’s more limit/inside mix seem to correlate with its median E/Q to keep its execution quality looking worse while market-heavy routing shows up as greener, that is a better E/Q. HRT’s best in class median-level E/Q is consistent with this profile—even though its top10 ETFs set is smaller in our per-ticker files, its book keeps a larger share of executions in sub-0.40 E/Q.

The top 10 retail traded stocks (Opendoor, Nvidia, Tesla, Intel, Palantir, as well as penny stocks like Tilray, Denison Mines et al.) tell a similar August story. In the deepest names (INTC, AAL, NVDA), makers’ E/Q is tightly grouped, and differences are small; in idiosyncratic names (OPEN, PLTR, TLRY) dispersion widens and order-type mix seem to qualify execution quality.

Susquehanna again shows the highest of at market routed executed stocks (≈80% on stocks), Hudson River is next, while Jane Street carries a higher marketable-limit and inside-quote proportion which seems to lead to worse E/Q in these names. *

In short, execution quality rankings seem at least driven, in part, by which names each market makers leaned into and even more how much of that flow they executed as market vs. marketable-limit orders or outside the quote orders. Jane Street the largest ETF market maker worldwide is unlikely to be offering the worst execution quality for them, rather retail broker route to them specific orders (marketable limit, outside of quote) that skew the execution quality average picture.

This article has been amended to correct a factor mulitplication in volume of shares traded (ratioed by 10)

In all our execution quality reports, we discuss E/Q, the standard measure of wholesalers’ / retail market makers’ execution quality. The measure is calculated as the spread realised by market makers versus the national best bid offer (NBBO) mid-point divided by the prevailing NBBO spread. This means a ‘0’ E/Q is a trade at mid price, 0.5 is a trade at half the spread between mid and NBBO, and ‘1’ is trading at NBBO, while ‘2’ would be trading at twice the spread.

605 disclosures contain these aggregate measures per order type and order size, as well as tickers and volume. For price we use our monthly calculated volume weighted average price (VWAP) per ticker from the ‘all trades’ proxy sourced and constructed on BMML Data Lab.

Our lit market proxy looks at all the securities information processor’s trades within the month, as long as the bid and offer have been updated within 10 seconds of a trade, and the quotes are not locked or crossed.

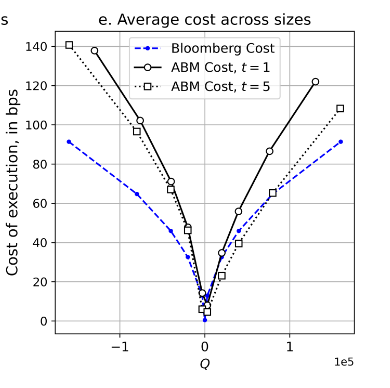

A David-and-Goliath battle has broken out in the world of pre trade transaction cost analysis (TCA). In one corner, upstart vendor Simudyne unveiled an agent-based TCA model that it claims outperforms Bloomberg. Now the data and analytics behemoth has hit back, accusing the upstart of mischaracterising its research.

In its research paper ‘Agent-based liquidity risk modelling for financial markets’, Simudyne presents a simulator of a continuous double auction in which fundamental investors, momentum traders and noise agents interact so that short-lived and permanent price impacts emerge from the simulation rather than being imposed ex-ante from empirical formulas. The authors calibrate to Hang Seng index futures and run Monte Carlo paths to generate liquidity-risk surfaces across order sizes and horizons; to demonstrate the strength of the endeavour they compare reinforcement-learning execution schedules with time weighted average price (TWAP) and volume weighted average price (VWAP), two common strategies to minimise market slippage.

Simudyne frames the work as both research and live tooling.

“This liquidity risk calculation, this liquidity risk manager, is currently in use in production in Hong Kong stock exchange,” said Justin Lyon, founder of Simudyne, describing scenarios run daily by venue risk managers.

He also told Global Trading that the simulator could have a large impact improving the execution of meta-orders: “We are showing, with evidence, that we can deliver at least a 10-basis-point improvement in execution. Instead of relying on bog-standard liquidity-seeking algos, the portfolio manager simply says, ‘spin up the AI-powered simulator’. It is calibrated and run overnight, and by the next morning it is executing a completely bespoke algorithm – specific to that flow, specific to that venue.”

Hong Kong Exchanges and Clearing (HKEX) declined to comment on the paper and the use in production of the model for liquidity risk prevention at its central counterparty (CCP). But Richard Wise, head of risk for HKEX group, co-authored both the aforementioned paper and others with Simudyne, including one presenting how the simulator is used to estimate potential liquidation costs in real-time with HKEX.

Not everyone is convinced by the substantial improvement promised on large order executions. A head trader at a large European institution told Global Trading: “Ten basis points against arrival price seems a massive improvement to achieve.”

When we contacted Bloomberg, whose pre-trade transaction cost analytics (TCA) tool is widely used by buy- and sell-side desks, the firm was sanguine about how its approach is presented in Simudyne’s paper.

Vlad Rashkovich, global head of trading research and analytics at Bloomberg, said: “The part that is a bit surprising to me is that the formula that they are quoting is not the one used in Bloomberg’s TCA equity model. Their research references many documents, but they have no reference to the paper, which we published in the Journal of Trading, (Autumn 2012), where we introduced our approach and share our results.”

He also stressed the scale and breadth of the firm’s calibration set: “Bloomberg’s pre-trade TCA model is based on millions of parent orders from some 500 buy-side firms across 89 countries.”

Bloomberg told us that its model fit (r²) varies by region and microstructure, and is typically around 10% in the US 8-9% in Western Europe, and 7-8% in developed Asia. Their model coefficients evolve slowly as market structure changes. Their refresh cadence depends on asset class: some fixed income models are recalibrated daily, others are reviewed quarterly.

The firm also emphasised that execution horizon has been central to its framework since 2012, rather than relying on a simple ‘block’ formulation, and that its models are trained on contributed parent-order data large enough to link fills into meta-orders across brokers and regions.

Simudyne argues that a venue-calibrated, agent-based exchange can do three things empirical pre-trade models cannot provide directly.

First, it can run fully specified counterfactuals: by simulating many price paths for a given order and horizon, the desk can separate market-risk variance from market-impact cost rather than inferring that split from past orders.

Second, it can let microstructure effects emerge: By allowing agents to update beliefs and interact through the order book, both short-term and permanent impacts arise without pre-imposing a functional form.

Third, it can produce learning-based schedules: reinforcement learning strategies trained inside the simulator can output execution trajectories that adapt to the calibrated venue state, which the firm says underpins the “10 bps” claim when compared with standard participation templates.

Some market participants we talked to criticise the published calibration as limited to a single venue/day and that independent validation across regimes remains the key test.

Other independents are innovating and adapting existing models to specific microstructures.

BestEx Research has launched Pulse, a futures-specific pre-trade estimator delivered by API within its algo management system that seems to compete with Simudyne ABM simulator, while Bloomberg does not offer futures pre trade TCA at the moment. BestEx says Pulse is symbol/future-specific, accounts for “shadow liquidity” and explicitly splits total slippage into market-impact and order-placement components.

As Hitesh Mittal, founder and chief executive, says: “From a Pulse perspective, the benchmark is arrival, arrival price… It breaks it down into two components… Market impact cost and order placement cost. it is not an optimiser; it is really an estimator;” BestEx argues that in many futures, reported contract volume is a poor proxy for executable capacity across related markets and along the curve, and that liquidity is better proxied via spread, depth, and resilience.

Northern Trust Asset Management (NTAM) is launching long/short equities portfolios for institutional investors and financial advisors, effective early 2026.

NTAM holds US$1.3 trillion in assets under management.

Tax-managed strategies of this kind are increasingly popular, NTAM says, allowing clients to access diversified concentrated positions, use losses to offset gains from business sales and private equity distributions, improve short-term loss harvesting for cash-driven portfolios and revive inactive portfolios.

Slava Malkin has been appointed as a senior portfolio manager for the offering. Based in New York, he reports to global co-chief investment officer Anwiti Bahuguna – promoted to the role last month.

Malkin has close to 25 years of industry experience and joins NTAM from BlackRock, where he has been director of Aperio quantitative strategies since 2021. Prior to this, he was a portfolio manager and quant researcher at NorthCoast Asset Management.

In a blow to the Australian Stock Exchange (ASX), Cboe has received regulatory approval from the Australian Securities and Investments Commission (ASIC) to operate a listing market in the country.

ASX Group was put under investigation by ASIC in June, after concerns were raised about whether it was fit for purpose.

Cboe’s approval will increase listing optionality in Australia, putting Cboe in direct competition with market operators including ASX, the National Stock Exchange of Australia (NSX) and the Sydney Stock Exchange (SSX).

Cboe Australia holds a 20% share of total equity market turnover in the country – close to AUD 2 billion in trades. It has been active since 2011, under the name Chi-X, before being acquired by Cboe Global Markets in 2021. The group also offers a listing market in the US.

Joe Longo, ASIC chair, commented, “This move will provide more choice for companies to list in Australia, build more links to offshore markets and create more options for investors, which is good news for the Australian economy.”

ASIC’s attempts to boost IPO activity in the country have included a ‘fast-track’ procedure, which the commission says can down the IPO timetable by up to a week, and allowing firms to accept retail investor applications during the public exposure period for new listings.

AUD-denominated IPOs have been minimal over the past 12 months, with US$3 billion representing just 1.6% of global issuances. The largest IPO, by data centre investment, operation and development company DigiCo Infrastructure REIT, constituted over a third of this – a US$1.3 billion offering announced in November 2024.

David Myers has joined ClearBridge Investments as a senior trader on the global trading team.

Based in Edinburgh, he reports to head of trading Patrick Collier. He will lead the firm’s global emerging markets portfolios and cover European trading in partnership with fellow trader Anthony Lucas.

ClearBridge, a Franklin Templeton-owned global equity manager, holds US$195.5 billion in assets under management as of end-June.

The appointment is part of ClearBridge’s alignment with active equity specialist Martin Currie, the firm said. Myers has been head of trading at the firm for more than 15 of his 30 years in the industry.

Prior to this, he was a trader at single-manager hedge fund O’Connor – sold to Cantor Fitzgerald by UBS earlier this year.

Euronext has launched its voluntary exchange offer for the acquisition of all common registered ATHEX shares.

ATHEX shareholders have until 17 November to accept the tender offer, which will exchange every 20 ATHEX ordinary shares for one new Euronext ordinary share. Euronext must gain 67% of ATHEX’s voting rights by this time – represented by 38,759,500 shares – to give it a total 90% of voting rights.

An announcement of the offer’s results is expected on 19 November. If conditions are fulfilled, Euronext will take control of ATHEX on 24 November.

ATHEX reported increased revenues year-on-year for H1 2024, with the listings division popping 27% to €2.5 million, and trading up 37% to €6.5 million.

The deal, which was first announced in July, has received positive market feedback.

Euronext states that the integration of ATHEX into its European network would improve liquidity for the Greek market, through the adoption of its Optiq trading platform, and support a single post-trade infrastructure across the continent. Euronext Clearing will be expanded to cover Greek securities.

The group also plans to make ATHEX its Southeast Europe hub for listings in the region.

CEO and managing board chairman Stéphane Boujnah commented, “Europe is entering a new strategic phase in building more integrated European capital markets that serve local economies within the framework of a Savings and Investments Union.

“Greece’s robust economic growth, supported by rising investment, growing international confidence, and solid fundamentals, makes this the right moment to strengthen its market. Through the integration of ATHEX into Euronext’s ecosystem, Greece will play a key role in this European project. This move will enhance the visibility and international appeal of the Greek market, supporting the shared European goal of stronger, integrated and more efficient capital markets.”

The ATHEX board of directors has given the initiative its full support.

Third Avenue Management: US Government shutdown fuels market uncertainty, while buy-side overhauls core tech systems.

As markets enter the fourth quarter of 2025, the US Government shutdown kicks off a fresh bout of uncertainty and potential for market volatility. Michael Warlan, global head of trading and operations at Third Avenue Management, speaks to Trader TV about unease in the market if the government disruption continues past this week.

Despite the unsettled market backdrop, Warlan also discusses the details of how his buy-side firm is rolling out a new execution and order management system (EMS and OMS), detailing implementation challenges, its importance in today’s trading environment, and the future role of auto-execution across its multi-asset desk.