Tom Oxton has joined Bank of America as head of EU electronic execution services trading. He is based in Paris.

Bank of America reported US$4.3 billion in equities sales and trading revenue over the first half of 2025, an increase of 12% from H1 2023’s US$3.8 billion.

Oxton has over a decade of industry experience and joins BofA from Goldman Sachs, where he has been an executive director and equity trader since 2018. He specialised in the European tech, media and telecoms sector and block trading.

Prior to this, Oxton was a financials equity trader and vice president at Barclays Investment Bank.

Marex Group plc announced today it has agreed with Close Brothers to buy Winterflood Securities for £103.9 million in cash.

Founded in 1988, UK equity market maker Winterflood Securities services over 400 institutional clients. According to Marex, Winterflood represents 15% of the LSE traded volumes.

According to Close Brothers’ latest earnings reports, Winterflood has long held a top three rank among LSE counterparties, driven by high-frequency liquidity provision and execution services. Despite this position, it reported a £800k operating loss for the first half of 2025 which closed 31 January, following a £2.6 million loss in H1 2024.

Announcing the acquisition, Marex CEO Ian Lowitt said: “This acquisition gives us an opportunity to transform our existing equity market making business into a leading franchise”

He expects synergies via scale, technology integration, and access to new institutional clients.

The deal follows Marex’s strong start to 2025. For Q1, the firm reported revenues increased by 28% year-on-year? to US$467 million.

The transaction is subject to regulatory approval and expected to close in early 2026.

Alex Ham, global head of investment banking, Barclays

Alex Ham has been named global chairman of investment banking at Barclays, effective early 2026.

In the London-based role, Ham is responsible for furthering Barclays’ UK and European investment banking franchises.

According to Dealogic data, Barclays generated US$1.3 billion in global investment banking revenue over H1 2025, holding its sixth-place standing in the rankings.

In equity capital markets, US$151 million in revenue and a 2.6% market share saw the bank fall from seventh to eighth position globally. In debt capital markets, it fell from fifth to sixth globally with US$560 million and a 4% market share.

Earlier this month, Barclays made a slew of appointments within its investment banking business across APAC.

Ham has more than two decades of experience, spent at Deutsche Bank. He has been co-CEO of UK investment banking business Deutsche Numis since 2016, and co-head of corporate broking since 2012.

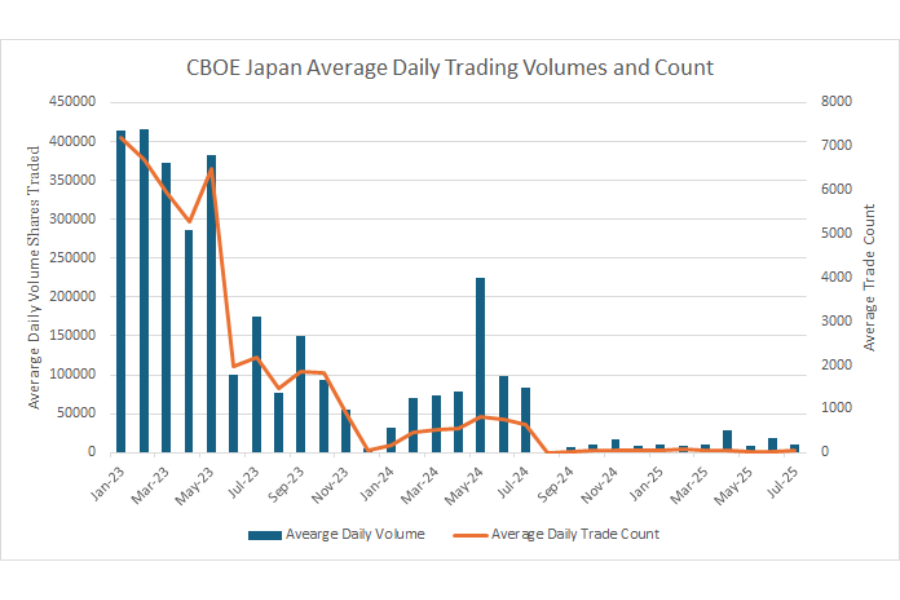

Cboe is shuttering its Japan equities business, including its proprietary trading system and block trading system Cboe BIDS Japan.

Volumes at Cboe BIDS Japan collapsed in 2024, hitting zero between 26 July and 2 September 2024. Average monthly shares traded dropped by 90% between January 2023 and January 2025, falling from 414300.5 to 9878.

On a yearly basis, the average trade count in 2023 was 3476, with volumes of 214,000. In 2024, these figures were 349 and 58,000 respectively.

CBOE Volumes Trade Count Graphic

Cboe BIDS Japan was created after Cboe acquired Chi-X Asia Pacific in July 2021.

Operations are planned to be suspended on 29 August, with the businesses formally closed after consultation with regulators.

Cboe stated that its closure of the businesses is strategic, adding, “The decision to close this business reflects Cboe’s disciplined strategy to steward resources towards opportunities that deliver the best potential returns for shareholders and was taken in the context of evolving business conditions, which challenged the financial sustainability of maintaining operations of Cboe’s equities business in the country.”

The details of these “evolving business decisions” were not shared.

A source familiar with the market told Global Trading, “[Cboe Japan] dropped from 200-300b to 40b daily as the Japan Alternative Market (JAX) accelerated. Seems JAX best execution policy may have changed as of mid-June and [is] no longer interacting with CBOE.”

“[Cboe] anticipates that the wind down of the Cboe Japan equities operations will have an immaterial impact on Cboe’s organic total net revenue growth and adjusted operating expense guidance in 2025,” it added.

The venue will continue to operate its global derivatives and Data Vantage businesses in the region.

Last year, Cboe took a 14.8% share in proprietary trading venue Japannext in an effort to expand its presence in the country beyond Cboe Japan. It stated that the two venues would be run independently.

Established by brokerage firms SBI Securities, Rakuten Securities, Orix Securities, and Click Securities in 2006, Japannext now holds 5% market share in the country. Goldman Sachs Japan is also a stakeholder.

Cboe did not respond to requests for comment on the matter.

UBS is looking to rationalise further its market data spending. On 22 July, the bank said a long-term partnership deal with London Stock Exchange Group would allow it to adopt LSEG’s revamped offering, particularly Eikon successor Workspace, across all asset classes and business lines. It aims to consolidate data infrastructure, enhance data cataloguing, and streamline data governance and access across the bank.

UBS CEO, Sergio Ermotti, described the contract as one further lever of the Credit Suisse integration program. He emphasised the potential to unlock further “cost synergies and operational efficiencies” as legacy systems are retired.

The bank’s 2024 annual report shows that ‘market data services’ costs reached US$749 million, up from US$419 million in 2022 as duplicate feeds and associated fees inherited from Credit Suisse hit their P&L.

By the end of Q1 2025, UBS had already booked US$8.4 billion of gross cost savings ,or 65% of its Credit Suisse merger related US$13 billion 2026 target. In its latest earnings call presentation, the bank said: “We expect that most of the remaining US$4.5 billion in gross saves required to achieve our US$13 billion target will come from reductions in technology, staffing and vendor costs.”

According to LSEG, Workspace supplies real-time, multi-asset prices, Reuters news and low-latency data feeds, together with a full programmatic access. Its partnership with Microsoft means those data streams and analytics can be embedded directly in Teams and other 365 applications, with the aim of allowing a single, cloud-based desktop to replace separate market terminals and chat systems across UBS’s worldwide operations.

Industry sources quote a headline cost of about US$22,000 a year for a full Workspace license and US$3,600 for a pared back tier, whereas Bloomberg has notified clients that a single seat Terminal will rise to US$31,980 in 2025, with multi-seat contracts at US$28,320. On list prices alone, UBS therefore would stand to cut 25% to 30% from each screen it replaces before factoring in exchange fees or Bloomberg’s dedicated hardware.

At LSEG, the data and analytics division generated £4.01 billion in 2024 and £1.04 billion in the first quarter of 2025, representing 46% of group income. Organic growth in the segment accelerated to 5.1 % in Q1 and management guided for 6.5% to 7.5% for the full year, or £4.3 billion.

With Eikon’s sunset already passed on 30 June, Workspace is LSEG’s sole flagship desktop.

Munish Gautam, global head of trading platforms product management, Broadridge Trading & Connectivity Solutions

Munish Gautam has joined Broadridge’s Trading & Connectivity Solutions (BTCS) business as global head of trading platforms product management.

Based in London, Gautam reports to BTCS chief product officer Brian Pomraning. He is responsible for Broadridge’s multi-asset order management system (OMS), which connects to more than 200 trading venues. A major competitor in this space is BlackRock’s Aladdin.

He will also work to strengthen Broadridge’s overall front-office technology services for global capital markets clients.

Broadridge has made a number of changes to its front office trading solutions team over recent months, including naming Ken MacHarg global head of futures and options trading in June and appointing Ian Williams and Anand Chintala as product management leads in April.

“Clients today need trading platforms that not only deliver low-latency cross-channel execution and adaptability but also respond to ongoing regulatory and structural changes,” Gautam noted.

“I look forward to building on Broadridge’s culture to deliver an agile, resilient and data-powered trading ecosystem that keeps our clients ahead of the curve.”

Gautam joins the company from JP Morgan, where he has been an executive director and cash equities product management lead since 2010, focused on the firm’s global equities trading platforms. Prior to this, he spent almost four years at Credit Suisse as a senior business analyst for equities.

The SEC is exploring whether to tweak its trade-through prohibition amid criticism that the current rule forces some market participants to worse-than NBBO pricing after fees and rebates are considered.

The SEC aims to reassess the “trade‑through” prohibition enacted by Rule 611 in 2005; the rule forces trading venues to execute at, or route orders to, the national best bid or offeror better. Announcing the event, chair Paul S. Atkins said: “Reg NMS and its Rule 611 have not served investors or broker‑dealers well, given the market distortion and resulting gamesmanship by those that seek to take advantage of the Reg NMS structure.”

Joe Saluzzi, partner and co-founder at Themis Trading told Global Trading that: ”Atkins is correct and Rule 611 should be reviewed. Reg NMS shattered the equity market causing liquidity to disperse amongst dozens of exchanges and off-exchange venues. Displayed liquidity shrunk and the average trade size plummeted. HFTs were quick to jump in to take advantage of latencies between these market centers and the stock exchanges were more than happy to arm them with the tools that were necessary. The SEC needs to figure out a way to put the pieces back together and a review of Rule 611 is a good start.

Several research papers have been presenting evidence supporting this affirmation. Sida Li, Mao Ye and Miles Zheng in their paper from 2021 titled “Refusing the Best Price?” say “As the NBBO ignores exchange fees, 62 % of routings lead to worse net prices.” Their study finds that brokers often bypass the apparent best quote when fee differentials make another venue cheaper once costs are netted out.

In the paper “Does maker-taker limit order subsidy improve market outcomes?”, Yiping Lin, Peter L. Swan and Frederick H. de B. Harris go further: “The regulatory requirement that trading and order flow depend only on raw (nominal) spreads and prices underpins the multi‑billion‑dollar subsidy to limit orders

Our own Global trading study of lit continuous trading finds that 2% of trades happen at worse prices than the NBBO.

Rule 611 was introduced in 2005 to prevent one marketplace from selling stock at a price inferior to a protected quotation displayed elsewhere. Critics argue that the rule looks only at the nominal price and ignores the exchange access fees and rebates that determine an investor’s net execution cost.

The roundtable planned for 18 September gives market participants the opportunity to express their view on the need for it to still exist.

Sandro Oswald, quantitative trader for the central risk book, Susquehanna

Sandro Oswald has joined Susquehanna as a quantitative trader for the central risk book. He is based in London.

Susquehanna executed 7.7 billion shares in May 2025, according to Global Trading analysis, with price improvements of US$55.7 million provided to retail traders down more than 20% on April figures. Execution quality also declined.

Oswald joins the company after almost a decade at Morgan Stanley, where he was most recently co-head of the centralised risk book and systematic market making for the EMEA region, covering cash equities and Delta 1. Prior to this, he was a quant trader for ETFs and equities.

Earlier in his career, Oswald was an ETF quant trader at KCG Holdings and Bank of America Merrill Lynch’s quantitative statistical arbitrage group. He also spent five years at Interactive Brokers, leading ETFs and structured products for the Swiss Timber Hill business.

UBS AM: Markets brace for the tariff volatility, and concerns develop over “irrational optimism”

While markets have been trading at all-time highs, Stuart Lawrence, head of equities at UBS Asset Management, warns of a potential market pullback in September as tariffs take effect and looks at whether the market’s “irrational optimism” could collide with the hard economic data.

BofA_900x600")